“We live in time, and through it.”

-Wallace Stegner

That’s another great quote about life from a book I’m quite liking right now, Angle of Repose. For the record, there is no repose for me this morning. And I like it. There will be plenty of time to sleep, when I retire.

In the meantime, I’m getting on a plane to the heartland of America for a day of investor meetings. I’ll be outlining what I think is becoming more likely by both the day and economic data point – Slower-For-Longer, on both US and Global growth, that is…

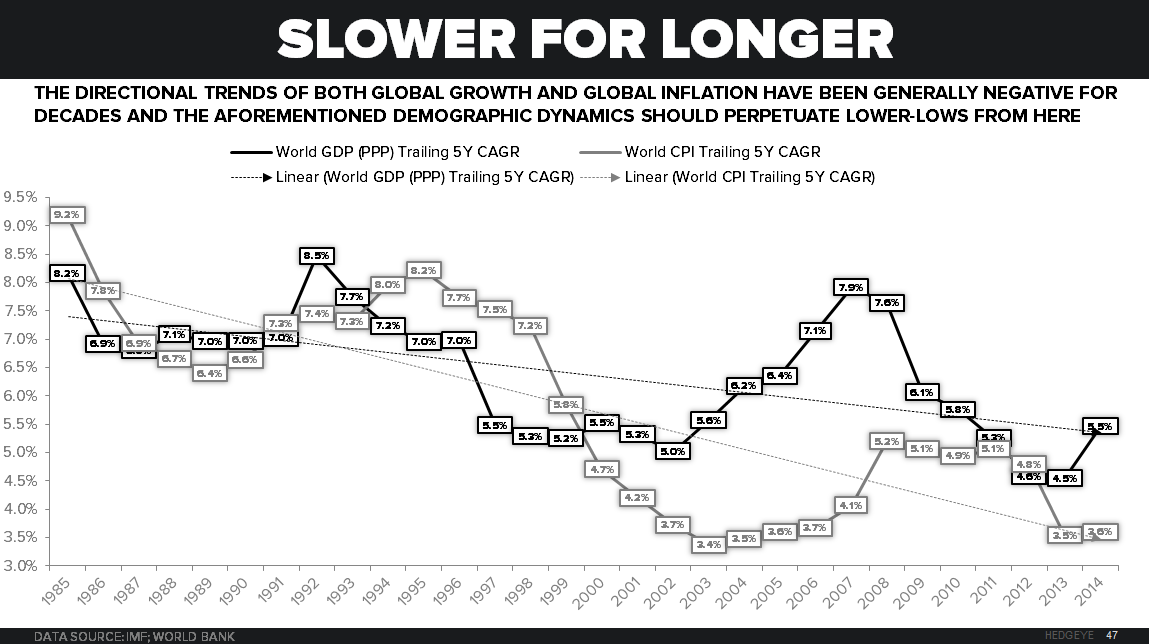

The two core components of our Global Macro slide deck remain A) the cyclical call (USA in a #LateCycle slowdown) and B) the secular call (#Demographic slowing of core baby boomer consumption cohorts, in the US, Europe, Japan, and China).

Back to the Global Macro Grind…

Dollar Up, Rates Down? Yep. We lived through that yesterday. In terms of our positioning, some of that was good – some of it bad. It was a very immediate-term move, but here’s what it looked like:

- Dollar Down -1.5% on the day (biggest down day in a month)

- Euro (vs. USD) +2.1% to the top-end of my current $1.08-1.12 risk range

- Commodities (CRB) Index +1.1% on the “reflation” trade to 226

- Oil (and Oil & Gas stocks) up with XOP leading US equity sub-sector performers +1.8%

- German 10yr Yield ramped from 0.49% to 0.71%, in a day

- US 10yr Yield chased that and went from 2.12% to 2.28%, in a day

This, mostly on consensus headline chasing of “inflation is back”, after the Eurozone posted a mind-altering 0.3% year-over-year “inflation” report for the month of May.

In other news, European producer prices (PPI) deflated -2.2% year-over-year. But don’t tell Bond Bears that.

What did my day look like?

- FX: I came into the day short the USD in Real-time Alerts and signaled buy/cover #Oversold

- Commodities: with our asset allocation at a 1yr high, I was satisfied and stayed put

- Bonds: didn’t do much of anything as we already trimmed our allocation to FI on last week’s rally

- *Stocks: opted to buy US stocks that look most like bonds in Utilities (XLU) and short more Retail (XRT)

- Hockey: coached practice until 7PM and felt normal for about an hour

- Family: kissed my kids on the forehead before bed

We either let these macro moves raise our anxieties to un-healthy levels or we live through them with a work/family life balance. I’m much more prepared on that front today than I was for the last US #LateCycle slow-down. That’s a #process too.

Back to the positioning (I think of asset allocation on a NET exposure basis, just because I love shorting/selling things when they are at the top-end of my risk range, so that I can hopefully cover/buy things back at the low-end of the range):

- US Equity Allocation = UP from 2% at the all-time SPX high of 2130 to 6% as of yesterday’s close

- International Equity Allocation = FLAT at 10% with most of that leaning long Japanese Equities

- Commodity Allocation = DOWN 1% from 13% to 12%

- Fixed Income Allocation = UP from 23% to 24%

- FX = DOWN from 3% to 2%

I realize how I communicate allocating capital to assets on down moves and taking some off on up moves isn’t for everyone. But it’s dynamic and daily. I do it every day in this transparent format so you can hold me to account.

On the Fixed Income vs. Equities debate I don’t really think that’s what matters most right now. I think the Sector Style and asset allocations you make to either the growth #accelerating or #decelerating exposures does.

In other words, if you think that:

A) US growth is going to accelerate in 2H 2015, you buy inflation/growth stocks and short Treasury Bonds

B) US growth is going to continue to decelerate in 2H 2015, you buy #YieldChasing stocks and bonds

Sure, you’ll have to live through volatility along the way. But, if the best longer-term risk management call you could have made 1-year ago was preparing for Global #Deflation, from here until 2016 it’s setting up for Global #GrowthSlowing (again).

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.01-2.29%

SPX 2098-2118

Nikkei 20103-20709

VIX 13.03-14.94

USD 94.83-98.33

EUR/USD 1.08-1.12

Oil (WTI) 58.68-61.90

Gold 1178-1203

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer