KEY TAKEAWAY

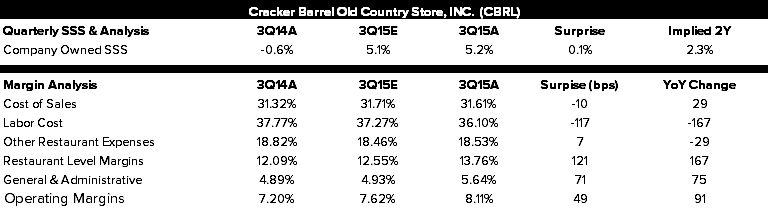

CBRL delivered a top and bottom line beat in 3Q15, reporting $683.7 million in revenue vs consensus $679.8 million, and net income of $35.3 million vs consensus $32.9 million. Comparable SSS of 5.2% also slightly exceeded expectations. Management effectively controlled costs while improving operating margins by 49 basis points (bps) versus 3Q14, and expanding restaurant level margins by 121 bps for the same period. The company has done a nice job spending their money wisely to grow sales and traffic. The concept has also benefited from lower gas prices.

We will be watching closely in the coming quarters to see if this positive momentum continues or begins to slow. We remain cautious that CBRL can continue the momentum.

Composition of the comp. This was an impressive quarter overall, the fourteenth consecutive quarter of outperformance of the Knapp-Track casual dining index. Although a bulk of the growth in same-store sales came from a +3.4% increase in average check, traffic growth was still greater than average in the industry, which is a positive sign.

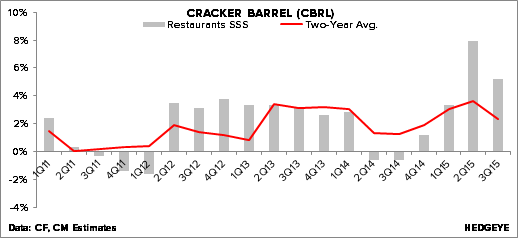

Same-Store Sales Trends are on their way up. For the last three quarters CBRL has its 2-year same-store sales trends accelerating. This past quarter, the 2-years trends slowed slightly, although the overall number remains healthy.

With great performance, comes great expectations. Going into Q4 and then into FY16 they have tough comps to beat, and although the street isn’t expected knock out quarters like the Q2/Q3 of this year they still want to see low-to-mid single digit same-store sales growth. Although CBRL is not in our starting lineup right now, we will continue to monitor it on the bench and modify our thinking if necessary.

VALUATION

CBRL is currently trading at the higher-end of its historical EV/ NTM EBITDA valuation range. I believe over time this number will normalize back to a lower more reasonable range.