This note was originally published at 8am on May 19, 2015 for Hedgeye subscribers.

“Trouble springs from idleness, and grievous toil from needless ease.”

-Benjamin Franklin

Not to be confused with Eurocrats who have recently returned from their monthly vaca, I’m pretty sure Ben Franklin was talking about lazy Americans who spend their time doing nothing.

They’re back! This morning’s macro market moves have nothing to do with central planners standing idle. Needless easing, you say? Who cares what we say? They say they need moarrr cowbell!

With both the European and Chinese economies now slowing, at the same time, there is only one play in their gravity-smoothing playbook for that. Must ease, faster.

Back to the Global Macro Grind…

On The Macro Show yesterday (new daily video product we’re launching on Thursday) I kept asking my man Darius Dale, “where’s Draghi?” With both European stock and bond markets under pressure, I figured he’d re-appear…

I figured wrong…

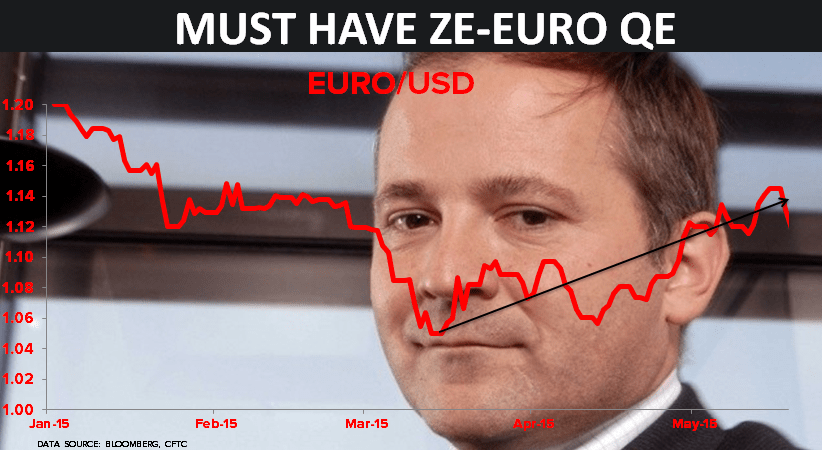

Instead of Draghi coming back from the beaches with a bazooka, he sent in the Frenchman. Who’s the French guy? As in The Lefty Economist, Benoit Coeure. This guy hails from L’Ecole Polytechnique and the Paris Club de creditors. He’s big time.

And a big time headline he provided, indeed!

“Ze ECB is going to front-load ze QE” -Coeure

That’s code for we’re going to get back to Burning Euros and buying bonds, so you, little yield chasing man, better get out of your idle bed and start buying stocks, fast! Here’s what Global Macro markets did on that:

- Euro -1.1% (vs. USD) to $1.11 after tapping the top-end of our $1.10-1.14 risk range last week

- EuroStoxx50 +2.1% in a straight line off last week’s oversold lows

- German Stock market (DAX) +2%, leading gainers, after a -2.2% drop on Up Euro last week

- US Dollar up +1% (from 1-month lows)

- Commodities mostly down on the inverse correlation move to USD

Oh, and not to be confused with centrally planned markets, there was the actual European economic news:

- German ZEW sentiment for April fell to YTD lows of 41.9 vs. 53.3 last

- Eurozone inflation for April clocked in at 0.0% y/y; wow was that Policy To Inflate successful!

- UK CPI -0.1% year-over-year in April (PPI -1.7%) was the 1st deflationary report since 1960

That would be the year 1960, not some moving monkey level in the SP500.

Ah, wasn’t local life in America grand back then. That’s when the front-page of the NY Times would trumpet a young President by the name of John F. Kennedy and his #StrongDollar, Strong America message…

Newsflash: this is not the 1960s

This is a worldwide growth slow-down. It’s getting more volatile by the day, week, and month as central planners struggle with realizing the output of their currency devaluation policies to inflate – economic stagnation.

In other gravity-bending news, China’s slowdown continues and so does the “policy response” to “stimulate. The Shanghai Comp Casino ripped another +3.1% overnight to +36.7% YTD on “easing requirements for corporate bond issuance.”

You don’t have your 401k or clients in “China” as Chinese growth slows at a faster rate than its population is aging? What is wrong with you? Don’t stand idle. Get a Chinese broker and a margin account already. This is easy. Grievous toil be damned.

Our immediate-term Global Macro Risk Ranges (with intermediate term TREND views in brackets) are now:

UST 10yr Yield 1.96-2.32% (bearish)

SPX 2107-2139 (bullish)

RUT 1236-1259 (bullish)

Nikkei 19589-20056 (bullish)

VIX 11.97-15.44 (bullish)

USD 92.99-95.61 (neutral)

EUR/USD 1.10-1.15 (neutral)

YEN 118.81-120.78 (bearish)

Oil (WTI) 55.99-61.39 (bullish)

Natural Gas 2.78-3.10 (bullish)

Gold 1203-1238 (bullish)

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer