TICKERS: MGM

EVENTS

- June 4: CCL special press announcement in NYC

COMPANY NEWS

MGM - MGM's Clark Dumont confirmed that preliminary votes showed all of the casino-hotel company's 11 incumbent directors were re-elected.

Takeaway: No surprise here

INDUSTRY NEWS

Package tours - visitors on package tours totaled 806,000 in April 2015, down by 6.8% YoY. Package tour visitors from Mainland China (648,000) and Taiwan (45,000) dropped by 6.6% and 19.6% YoY, respectively.

There were 99 hotels and guesthouses operating at the end of April 2015, providing 28,000 guest rooms, up by 1.7% year-on-year; 5-star hotels accounted for 64.8% of the total supply, with 18,000 rooms.

A total of 827,000 guests checked into hotels and guesthouses in April 2015, down by 7.1% YoY. Guests from Mainland China (521,000) decreased by 12.0%, while those from Hong Kong (125,000) and Taiwan (29,000) increased by 10.9% and 8.6% respectively.

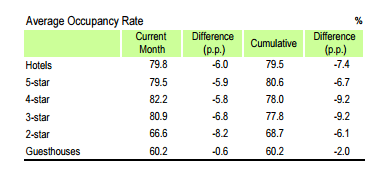

The average length of stay of guests held stable as April 2014, at 1.4 nights. The average occupancy rate of hotels and guesthouses was 79.4%, a rebound from March (77.2%) yet still down by 5.9% YoY; the rate of 4-star hotels and 5-star hotels was 82.2% and 79.5% respectively.

Takeaway: More bad news for Macau. Package tour visitors fell for the 1st time since Feb 2014. Hotel occupancy declined again in April (-6% YoY).

MACRO

Hedgeye Macro Team remains negative on Europe, their bottom-up, qualitative analysis (Growth/Inflation/Policy framework) indicates that the Eurozone is setting up to enter the ugly Quad4 in Q4 (equating to growth decelerates and inflation decelerates) = Europe Slowing.

Takeaway: European pricing has been a tailwind for CCL and RCL but a negative pivot here looks increasingly likely in 2015.