“Everyone wants to win, but not everyone is willing to prepare to win.”

-Bobby Knight

While Knight had his issues (don’t we all?), he didn’t have as many as most do in implementing a winning #process. At Indiana, Bobby Knight won 902 NCAA games, 11 Big Ten Championships, and 2 National Championships.

The New York Rangers have that same quote on the wall of their dressing room at their training facility in Tarrytown, NY. After routing Tampa Bay last night, the Rangers won their 9th out of their last 10 games when facing Stanley Cup elimination.

Preparing to win starts with reducing mistakes. If you don’t make a habit of making big ones, you’ll take up the probability of your success. Whether you’re on the court, the ice, or in the market – winning happens when preparation meets opportunity.

Back to the Global Macro Grind…

Were you prepared for US #GrowthSlowing? How about another sharp reversal (to the downside) in rates? Yesterday’s US Durable Goods report slowed to -2.3% year-over-year. Bond Yields fell, hard. At 2.14% the 10yr US Treasury Yield is down YTD.

Getting up early and grinding through the #process isn’t a given but, for me at least, that’s the easy part. The hardest part is contextualizing the short-term within longer-term durations. That’s where my team and I spend the most time preparing.

While that ramp to 2.36% in the UST 10yr Bond Yield got my attention, it also prompted me to take a step back and remind myself of our most differentiated research views. To remind Longer-term Risk Managers on those, they are as follows:

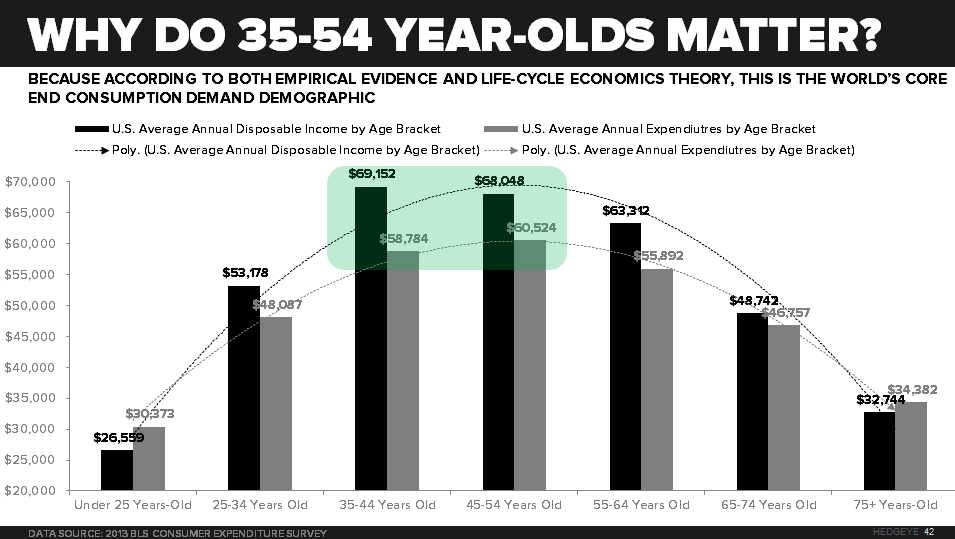

- #DemographicYields – with the USA, Europe, Japan, and China all seeing their core consumption cohorts ((35-54 year-old populations decline on an annual basis - see Chart of The Day for the USA one – yes, it’s secular)

- #LateCycle – not to be mistaken with something early-to-mid cycle like #Housing, classic late cycle sectors of the US economy are in month 73 of an expansion but now slowing in rate of change terms (wages, labor, capex, earnings)

- Long-term Global Growth Expectations have been, and remain, too high – so central planners around the world are going to have to react to #GrowthSlowing with more cowbell which will, in due course, perpetuate volatility

That last part (volatility) is what crushes the un-prepared. As in the permas – the complacent. Those who bought both the 2000 and 2007 highs in the US Equity market thinking there was a “new normal” in volatility – or something like that.

It’s The Cycle stupid.

And remember, stupid is as stupid does (I am a knucklehead hockey player don’t forget) when it comes to believing that the Fed, ECB, BOJ, PBOC, etc. can “smooth” both cycles and the market volatilities they breed.

But, but, “Keith, housing is strengthening.” #Agreed. So why don’t you strap on your active manager pants and buy early-to-mid cycle recovery exposure to US #HousingAccelerating (our Q1 2015 Macro Theme) instead of freaking out when rates rise?

Of course consensus doesn’t want to buy Long-Bonds or Housing or REITS A) after it missed them into their 2015 highs and B) when everyone and their Bond Bear brother is still underwater betting on “rate liftoff.”

So don’t be consensus.

Do you think that Ranger Coach, Alain Vigneault, was consensus when he took former NHL MVP, Martin St. Louis, off the Rangers 1st line in an elimination game last night and replaced him with a rookie?

In my proprietary Money Puck model (I.e. in rate of change terms) J.T. Miller has been the best Ranger (relative to ice-time) in the playoffs. He had his opportunity to play on the big line last night and had 4 points. Huge game! #Timestamped

Back to the Fed, rates, and Housing… do you really think that Coach Yellen is going to thwart the only major component of the US economy that has bullish rate-of-change momentum with a pre-emptive rate hike?

C’mon.

Even the Fed isn’t that pro-cyclical when it comes to their job protection. I actually think they are going to celebrate the success of Devaluing The Dollar and keeping rates low (forever?) because, alongside the stock market, that’s all they have.

Back to beating the US stock market in 2015, if you really are paid to win (both relative and absolute) in this game I think you’ll continue to avoid making big mistakes by being either underweight or net short:

- The Financials (XLF) which are still -0.6% YTD

- Industrials (XLI) which are now chasing them as relative losers, -0.5% YTD

If you’re long both of those, you’re A) losing and B) betting on:

A) US and Global Growth Accelerating (at the end of a cycle)

B) The Fed raising rates in September

You don’t have to “bet” on random mean reversions like those if you have a repeatable #process that probability-weighs the accelerations and decelerations in both growth and inflation, across durations.

Everyone in this game wants to make money, but not everyone can win when consensus doesn’t.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.97-2.21%

SPX 2098-2121

VIX 12.95-14.37

EUR/USD 1.08-1.15

Oil (WTI) 57.36-61.34

Gold 1185-1212

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer