This note was originally published at 8am on May 08, 2015 for Hedgeye subscribers.

"It is better to be a lion for a day than a sheep all your life."

- Elizabeth Kenny

Is it? In financial market terms that is.

While Nurse Kenny’s boldness served her well in her treatment of polio among other musculoskeletal illnesses (her controversial methods are credited with being the foundation for modern physical therapy), I’m not so sure she would’ve been able to manage global macro risks during confusing times like these with that attitude.

For example, what if you took on orange jumpsuit risk and got the look-see on today’s jobs numbers? Would you know how to appropriately position for it? Would you be a lion and bet big on red or black or would you be a sheep?

To be crystal clear, we don’t have any edge in accurately forecasting the rate of change in nonfarm payrolls. Between the seven analysts on our macro and financials teams, we have just shy of a cumulative 100 years of experience analyzing markets and economies in both buy-side and sell-side roles and not one of us has been able to build a model that consistently and accurately forecasts said number – or the rate of change in wages for that matter. The standard error on every model we’ve built is too high to rely on such estimates so we don’t bother to incorporate them into our views.

I guess we are the sheep.

Back to the Global Macro Grind…

There is a reason our cash position in our model asset allocation is as high as it’s been since mid-December; we are dazed and confused and require the shepherding of Mr. Market. Like God, he doesn’t speak to you directly – or out loud for that matter. Fortuitously, we employ a number of rigorous quantitative methods to extract such guidance from the marketplace (like TACRM for example).

Our intermediate-term views of lower-for-longer and deflation has been wrong for several weeks now and we have no problem jettisoning such views if Mr. Market tells us to. In this regard, he hasn’t given us the signal(s) just yet, but he’s definitely thinking out loud enough for us to lack a high degree of conviction in those views.

One thing we do have a high degree of conviction on is our ability to forecast the rate of change in both growth and inflation. We are also pretty good at figuring out how trends in these omnipotent macro factors front-run changes in monetary policy.

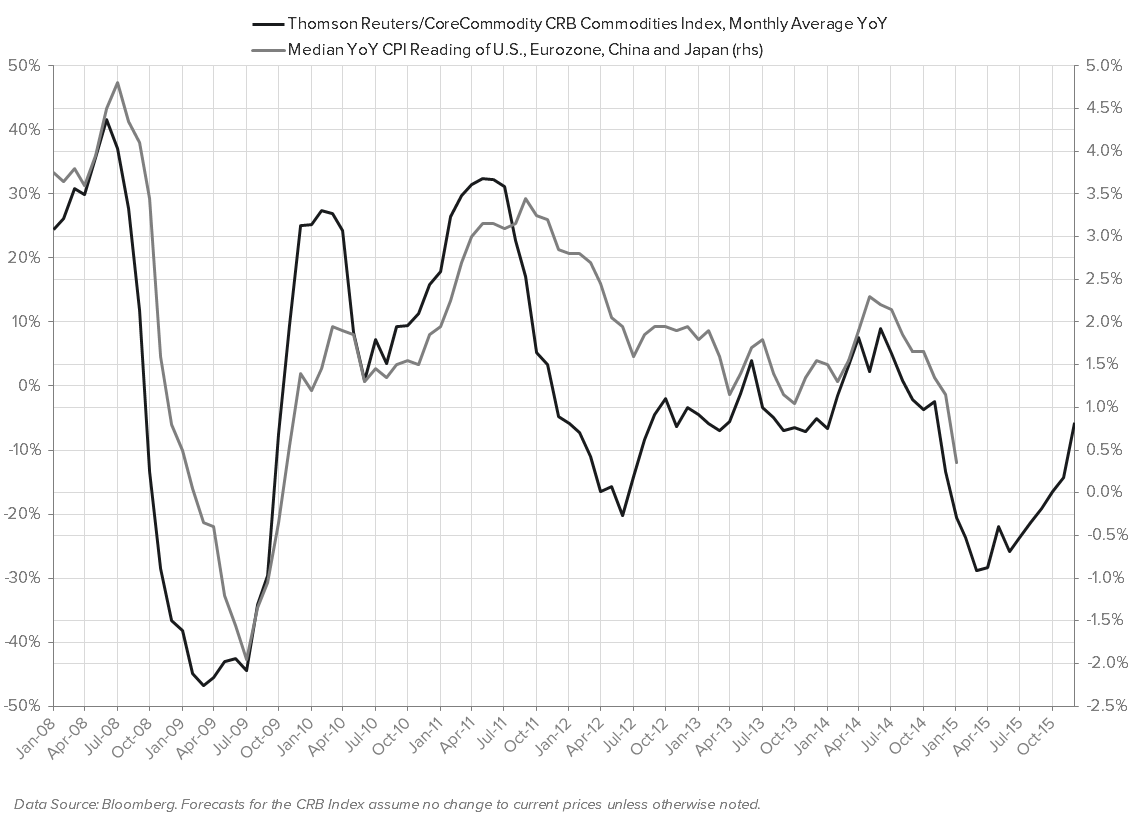

On that front, inflation is likely to accelerate in 2H15 and the risk to that forecast is actually to the upside as far as timing is concerned. Our inflation tracker had forecasted a bottom in YoY CPI in June as of ~6 weeks ago, but we now have the disinflationary impact peaking in April (chart #1 and chart #2). You’ll note on our GIP model (chart) that the 2nd derivative delta on inflation (x-axis) is very small in 2Q. We’re still disinflating, but not by much from here.

As previously mentioned, the base effects for CPI get really easy in the 2nd half of the year (chart). Will the Fed use this as justification for “having confidence that inflation will return to their target over a reasonable timeframe” and set the stage for hikes in 1H16? Maybe. By then, however, real GDP growth will have likely slowed dramatically (chart).

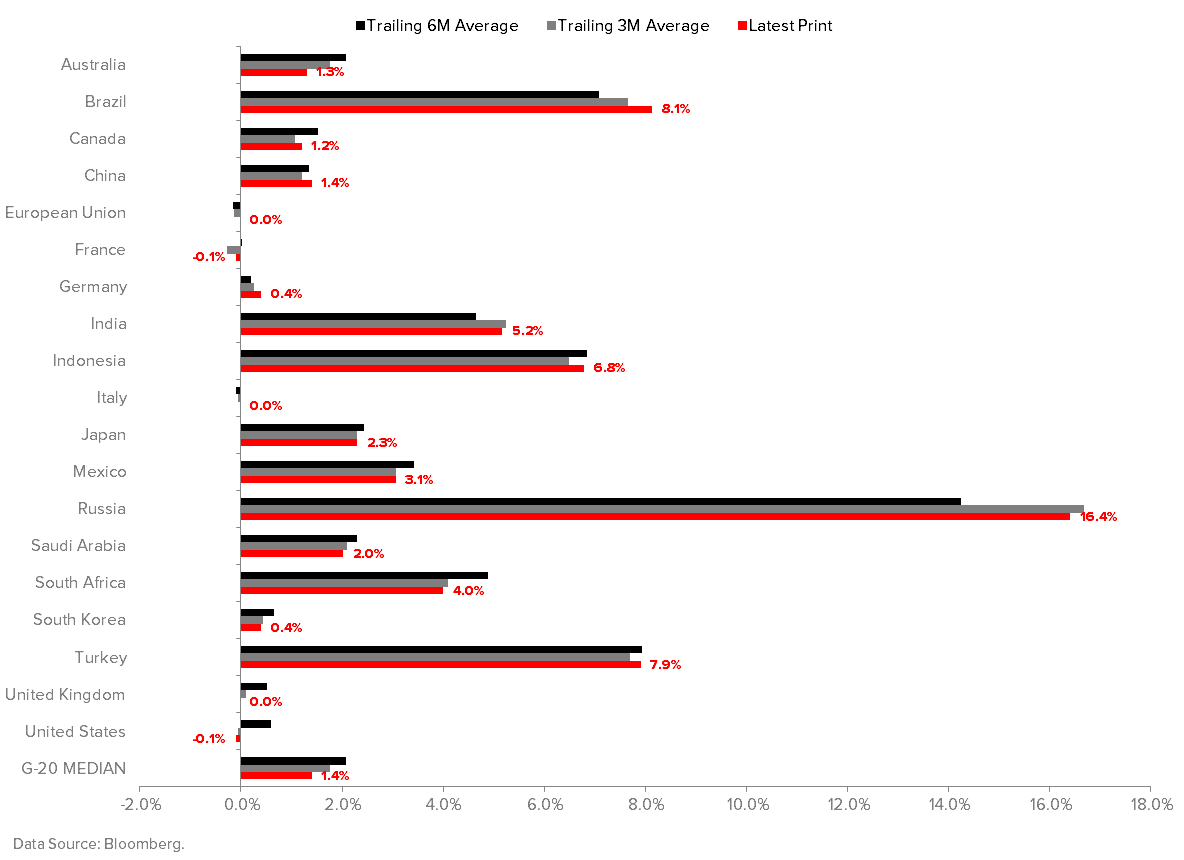

Broadening our horizon, inflation is still slowing on a trending basis across the world’s key developed economies. Across many of the EM economies, however, it is accelerating due to annualized currency debasement (chart). From a forecast perspective, global inflation is in the same boat as the U.S. (chart).

The strong inflows into TIPs of late appear somewhat prescient in the context of those forecasts. Specifically, investors have piled into TIPS at the fastest pace in three years, with $3.6B of inflows into mutual funds and ETFs that track this market. This follows two consecutive years of outflows.

Can rates work when inflation is accelerating? Our backtest data shows that the long bond usually works in #Quad3, but certainly not as much as it does in #Quad4 and arguably not when the Fed is setting the table for rate hikes (chart #1 and chart #2). We are simply making the bet that those rate hikes are not coming; in fact, the narrative could be one of preparing markets for QE4 by the time we get the 4Q15 GDP report at the end of January 2016. We believe spread compression to be a high probability outcome from here (chart).

Since this is probably the only strategy note you’ll read this morning that doesn’t focus on the jobs report, we’ll leave you with another piece of seemingly-random-but-useful analysis. The key takeaway from the Chart of the Day below is that over the next 2-3 months, the preponderance of high-frequency growth data is likely to look optically better relative to consensus expectations from here. It literally can’t get much worse as far as the surprise factor is concerned and we’re quite sure expectations for a broad swath of indictors were lowered after that soft 1Q GDP print. Also, 2Q GDP will accelerate on a headline (i.e. QoQ SAAR) basis.

We believe rates have likely priced in these dynamics and see no reason for bond yields to chase them any higher.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.87-2.29%

SPX 2071-2099

VIX 13.63-15.84

USD 93.61-96.53

Oil (WTI) 54.22-61.93

Gold 1170-1214

Best of luck out there,

DD

Darius Dale

Senior Macro Analyst

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}