“It's tough to make predictions, especially about the future.”

-Yogi Berra

Yogi turned 90 last week. Hedgeye will turn 7 in June. From the mound to markets, deep simplicities and pithy aphorisms are still ageless.

When Berra donned post-war pinstripes en route to 3 AL MVP’s, 18 All-Star appearances and 13 World Series championships, the U.S. was enjoying a productivity boon, the demographic tide was just beginning to come in, the middle class was ascendant, Buffett was still small enough to perform and the prospects of rising household leverage and modern central banking carried an air of secular opportunity.

“The Future Ain’t What It Used to Be”

Back to the Global Macro Grind...

Hedgeye’s formal coverage of the Housing sector turned 1 last week and I’ve chronicled our evolving investment view of the sector recurrently in the Early Look over the last year.

Our 2Q15 Housing Themes call, which we presented back on April 2nd, was titled “If it Ain’t Broke” … the allusion being that our reversal from bear to bull in late 2014 was working with Housing outperforming every other sector through 1Q15 and the fundamental strength looked set to continue.

The core of the 2Q call could be sufficiently captured in the context of the following four factors:

- The Data: The cocktail of easy comps, improving fundamentals, credit box expansion and rebound demand (i.e. deferred housing consumption due to weather) should conspire to drive accelerating rates of change in reported housing data in 2Q.

- The Dilemma: Housing equity performance shows pronounced seasonality with 4Q/1Q being periods of marked outperformance and 2Q/3Q generally being periods of relative softness. At the same time, the implementation of new TRID regulations on August 1st could emerge as a mild-to-large speedbump to reported activity.

- The Distillation: The convergence of performance seasonality and new regulation (TRID) – along with emergent issues such as the California drought and step function back-up in global bond yields - pose a collective risk to housing activity into the end of 2Q. While we remain mindful of those quasi-latent risks, it’s likely accelerating rates of change in both demand and price dominate investor mindshare in the more immediate-term.

- The (tactical) Decision: Let’s stay long accelerating improvement in the immediate-term and then look to lower exposure into the collective crescendo of concern as it builds into mid-late summer

To frame it another way: If I told you housing would put up the best rate of change numbers in all of domestic macro – and, arguably, in all of global macro – would you want to be long or short that?

So, how has the data come in thus far in 2Q?

- Housing Starts: New 7-year high in the latest month

- Purchase Applications (existing market): 2Q15 Tracking +14% QoQ and +13% YoY, on pace for best quarter in two years.

- Pending Home Sales (existing market): PHS are up an average of +11.8% year-over-year the last two months

- New Home Sales (new market): NHS are up an average of +22.5% year-over-year the last two months

- HPI: After a year of discrete deceleration in home price growth in 2014, 2nd derivative HPI has seen 3 consecutive months of acceleration through the latest March data.

How have the stocks performed?

- April (Rate Rise + Builder Margin Concerns): Of the four categories we profiled in our 2Q themes call as being beneficiaries of Housing's ongoing improvement, only one, the Mortgage Insurers, beat the market in April. The builders underperformed significantly and the Title Insurers and Home Improvement chains underperformed moderately.

- May: Housing got its mojo back in May, rebounding strongly over the last couples weeks alongside the moderation in rates and ongoing strength in reported price/volume data.

The somewhat confounding part is that even if I knew then, what I know now in terms of how the fundamental housing data would come in in 2Q, I would have made the same decision to lean long in April.

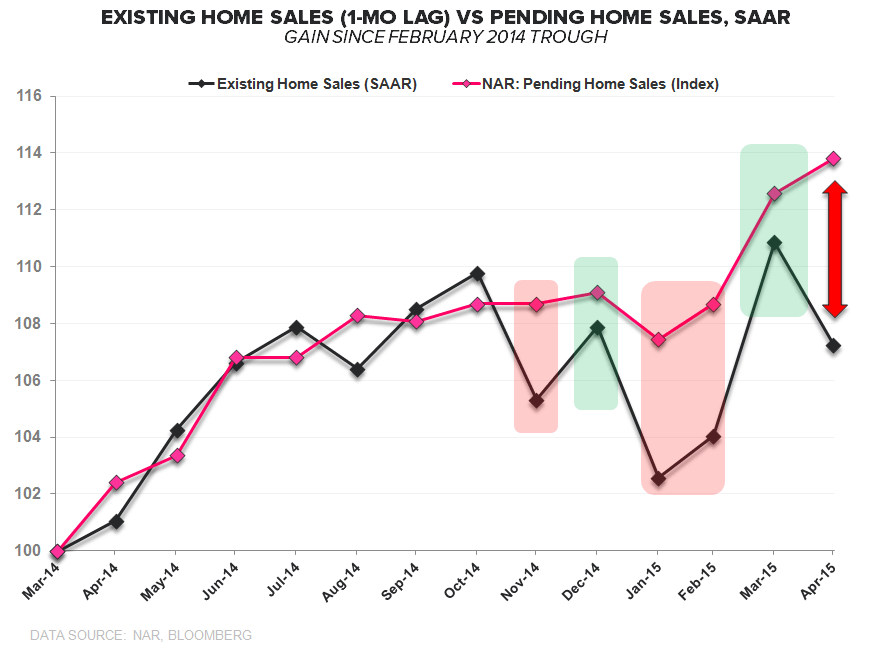

What about Existing Home Sales yesterday, that missed right?

EHS in April were certainly underwhelming, missing estimates and declining -3.3% sequentially (although they were still +6.1% YoY). Below is how we contextualized the data in our institutional note yesterday:

Here’s the primary issue at play: Pending Home Sales and Existing Home Sales have shown recurrent bouts of divergence and re-convergence in recent quarters. Definitionally, Pending Home Sales (PHS) represent signed contract activity while Existing Home Sales (EHS) represent actual closings. The two measures are invariably tethered and, given the mechanical nature of the relationship, PHS serve as a strong leading indicator for EHS with the relationship strongest on ~1mo lag.

There is some chop in the data from month-to-month but, absent some acute shock to the qualifying ratio, the two only diverge for so long and so much in magnitude before re-convergence between the two series occurs. Practically, this can only occur in a few ways – one series can fully re-couple with the other on a lag, both see subsequent revisions in opposite directions and/or both series (for whatever reason) move in opposite directions with spread compression from both directions.

As can be seen in the Chart of the Day below, the recent tendency has been for EHS to re-converge with PHS. Given the prevailing pattern, unless PHS in April (released 5/28, next Thursday) are very soft and/or March sees a significant negative revision, the path of least resistance is for upside in Existing Sales over the next couple months. Further, the trend in the high frequency mortgage purchase application data, which is currently running +14% QoQ and +13.3% YoY, argues in favor of that expectation more so than not.

Universality is the hallmark of acute observation. Clever linguistics provide the effervescence and perdurability. Ahead of the holiday weekend – and just because they’re good – I’ll leave you with a few of Berra’s best (annotated with associated investment applicability):

“It gets late early out there” (counter-cyclical investing… remember, the data always looks best before the crest)

“Nobody goes there anymore because it’s too crowded” (consensus’s thinking about consensus’s positioning)

“You can observe a lot just by watching” (no annotation needed)

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.97-2.24%

SPX 2110-2144

RUT 1

USD 92.92-96.17

EUR/USD 1.10-1.15

Oil (WTI) 56.98-61.64

Have a great weekend!

***Click here to watch The Macro Show live at 8:30am.