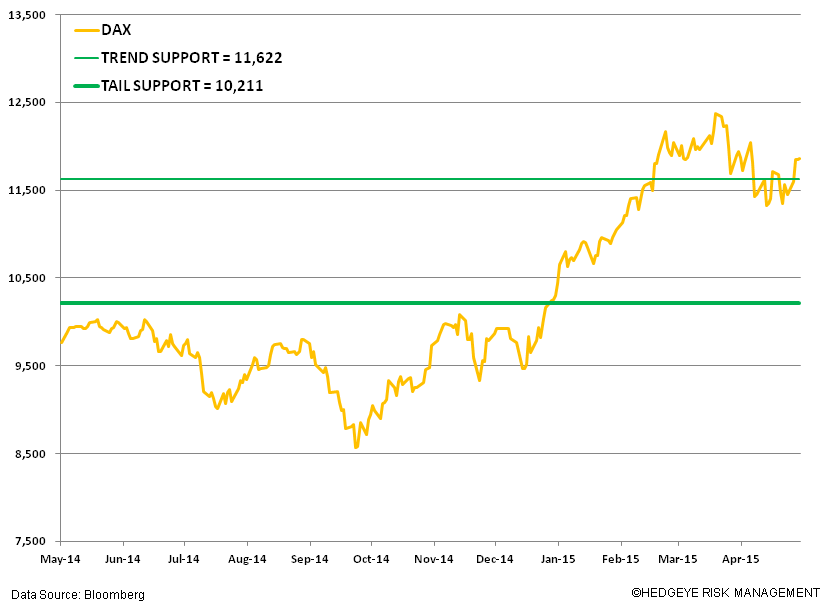

- German Equities = Bearish TRADE (3 weeks or less); Bullish TREND (3 months or more).

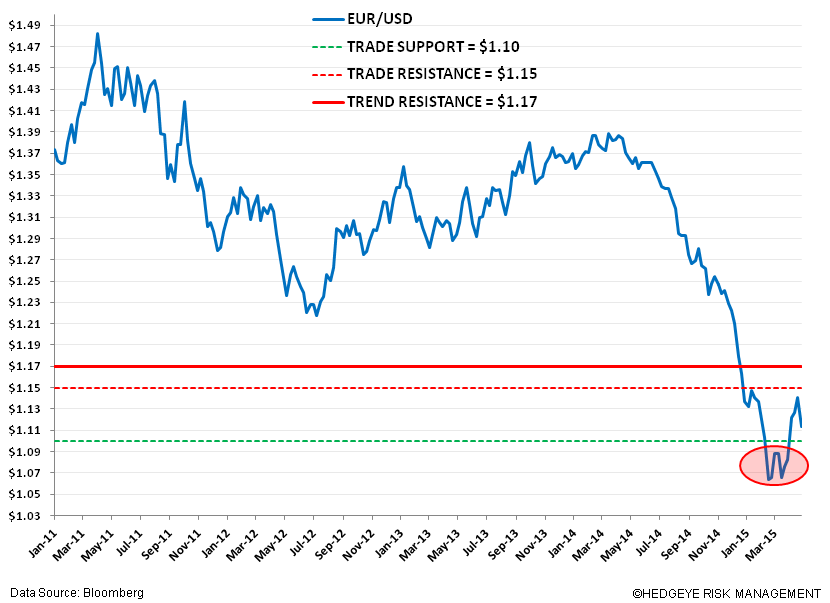

- TRADE: German fundamental data underperforming, EUR/USD strengthening, and Greek uncertainty. (Bearish)

- TREND: ECB head Mario Draghi will continue to ramp the QE machine, muting EUR/USD appreciation. Expect concessions made to Greece to advert default and Grexit. The macro team forecasts weakness in U.S. data that should perpetuate positive European equity flows, in particular to Germany. Bullish quantitative TREND & TAIL

On 4/14 we presented a 40 page slide deck titled Germany: Still Bullish (CLICK HERE for a video replay). Given the weakness in recent German data and the DAX (down -3% since our call), we believe it’s worthwhile to revisit and update our outlook.

Clearly the data over the TRADE has taken a leg lower. Below we show some key German and Eurozone fundamental data points that have recently missed estimates:

- Germany Manufacturing PMI 51.4 MAY Prelim (vs exp. 52 and 52.1 APR)

- Germany Services PMI 52.9 MAY Prelim (vs exp. 53.9 and 54 APR)

- Germany Retail PMI 52.6 APR vs 53 MAR

- Germany Construction PMI 51 APR vs 53.3 MAR

- German ZEW Sentiment 41.9 APR (YTD low) vs 53.3 MAR

- Germany PPI -1.5% APR Y/Y vs expectations -1.4%

- Germany Q1 GDP 0.30% (vs exp. 0.50% and 0.70% prior)

- Eurozone Inflation (CPI) 0.0% APR Y/Y

- Eurozone MAY Flash Consumer Confidence -5.5 vs consensus -4.8 and prior -4.6

Recent economic data points to weakness, but our bullish call on Germany was not predicated on the data (as the economics YTD have been weak at worse or grinding slightly higher at best). Rather focused on Draghi’s QE program and the benefit that the German economy would reap from a weak EUR/USD.

We believe the recent data misses in concert with the Greek consternation (everything from Grexit to Greek bankruptcy) has roiled European markets (especially the DAX) over recent weeks.

In addition, we’ve seen strengthening in the EUR/USD over the near-term TRADE duration (~ +4.5% since our Germany: Still Bullish call) which has further pressured the DAX lower. And as we move forward over this TRADE duration, here are the key macro calendar catalysts that we think will take the USD lower, and therefore the EUR likely higher:

- May 29th – ugly headline Q1 2015 GDP report will keep political pressure on the Fed to push out the dots

- June 5th – watch out for the cycle on the labor front; especially if we get the 2nd bad jobs report in the last 3

- June 17th – Fed Day in America (FOMC meeting); sleep in until 9AM and just buy everything

All that said, our TREND view on the DAX remains intact. While it’s tenuous ground, we have eyes wide open of the centrally planned world we live in. We expect Draghi to continue to have his foot squarely on the QE gas pedal, especially as fundamental data underperforms. In this light, we see Draghi poised to win the currency debasement war versus Janet Yellen’s Fed, if conditions warrant.

Here’s why we think German equities get a lift over the TREND:

- History has shown that the Eurocrats cave against any and every pressure of a member state to default or threaten to break-up the Eurozone. Therefore, once again, we expect the current Greek debt issues to “settle” (some sort of concessions will be made to kick the can down the road). This should boost most European equities that have been held down in recent weeks by (more) great uncertainty over the Greek state

- All-In QE. We expect the QE machine to ramp higher over the coming months (see recent buying in the chart below). We got a preview of this on Tuesday in remarks from the ECB board member Benoit Coeure who said the Bank will frontload QE purchases in May and June and will backload in September if needed. Expect such commentary from Bank members to chase the EUR/USD lowe.

- ECB Minutes confirm united board. Minutes released today show unity on policy measures (QE and no change in rates). We expect Draghi’s firm hand of “whatever it takes” to prevail –he’ll will Eurozone equities higher even if he struggles to inflect growth and inflation.

- US data weaker. Hedgeye’s macro team forecasts weaker data ahead, which should help fuel the Eurozone equity trade.