Listening to most recent mainstream media reports, you get the sense that former Secretary of State Hilary Clinton is not only a shoe in to win the Democratic nomination for President, she’s also very likely to win the general election. While most people on the right may view this with varying degrees of trepidation and disbelief, the view is actually well founded in current polls.

As it relates to her party’s nomination, the top six polling candidates based on poll aggregates are as follows:

- Clinton – 64.2%;

- Warren – 12.5%;

- Biden - 9.8%;

- Sanders – 7.4%; and

- Webb – 2.6%.

You get the point. The current “race” for the Democratic nomination isn’t really a race. Her current spread over Elizabeth Warren is a staggering +51.7 points. Fast forward to the general election match up, Clinton holds a sizable lead against various potential Republican nominees. Her most significant competitors— the GOP triumvirate of Jeb Bush, Rand Paul, and Marco Rubio—all trail over 7 points behind her in the poll aggregates.

The bottom line is that if the election was held today, there’s little doubt Hilary Clinton would be elected President. The election of course is not today and between now and November 8th, 2016 a lot can, and will, happen. Without further ado, here are five key factors that could put what currently looks like an inevitable Clinton Presidency at risk.

1. The Clinton Foundation - This risk is the most topical right now given the current scrutiny the Foundation is receiving thanks to Peter Schweitzer’s book, “Clinton Cash: The Untold Story of How and why Foreign Governments and Businesses Helped Make Bill and Hillary Rich.” It is also very likely an issue that will not go away. On some level, whether the Clintons acted ethically as it relates to the Foundation is irrelevant because there is enough fodder that it will allow Republicans to continue to keep the heat on the Foundation. To the extent the scrutiny accelerates, the Foundation has the potential to become Clinton’s “Swift Boat” moment.

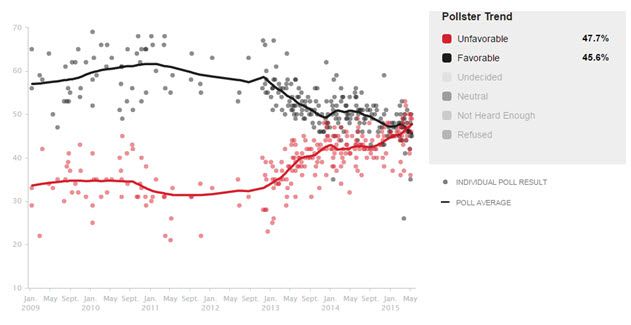

2. Likeability (and accessibility) – Since announcing her candidacy more than 35 days ago, Hillary has answered a grand total of 8 questions from the press. Whether this lack of accessibility is ultimately perceived as a lack of a common touch (think Hillary going into Chipotle wearing sunglasses and not leaving a tip) remains to be seen. However, as the chart below shows, her favorability has taken a steady decline since she left office as Secretary of State in February 2013. Most interesting, since actually announcing her intention to run for President, her “Unfavorable” rating has exceeded her “Favorable” rating.

3. Rubio Emergence – Ultimately for Hillary to not win the Presidency, a front running Republican candidate will have to emerge. The current GOP crop of contenders is broad, some would even argue deep, but there’s really no one is standing out or breaking out from the crowd. In the Real Clear Politics chart below, we show the top 14 candidates for the Republican nomination. (Yes, 14!) As the RCP chart shows, there is no clear front runner. In fact, Bush, Walker and Rubio are all basically in a statistical dead heat.

From our perch, it feels like the Republicans need a candidate that is not white, middle-aged and male. In the front runner category, Rubio clearly fits that bill. Latinos’ lack of support in 2012 (only 3 out of 10 votes) was noted as a key reason for Romney’s inability to win the election, so clearly this demographic will be key for the Republicans. Rubio (and to some extent Bush, given his Mexican born wife and bilingualism) has the best chance of increasing the Latino votes based on their backgrounds and policies.

4. Bill’s Gaffes – While there is no question that Bill Clinton is one of the most talented politicians of his generation, there is also no question he is (and maybe increasingly so) prone to putting his foot in his mouth. In today’s hyper-plugged in digital world, where no one is safe from a rogue iPhone recording a candidate’s every word, this may pose a delicate challenge for the former commander in chief. Don’t forget that the key negative turning point for Romney in 2012 was his 47% quote:

“There are 47 percent of the people who will vote for the president no matter what … who are dependent upon government, who believe that they are victims. … These are people who pay no income tax. … and so my job is not to worry about those people. I’ll never convince them that they should take personal responsibility and care for their lives.”

Remember, Romney said this in the friendly confines of a Republican fundraiser. The lesson? No environment in the day of iPhones and social media is off limits in terms of quotable material. Bill Clinton may have the political acumen to not have a major gaffe, but his historical penchant for the spotlight makes it difficult for him to stay out of the media.

The most recent gaffe was his response to NBC’s Cynthia McFadden after she inquired about his enormous speaking fees ($500,000 and above). Clinton responded, “I gotta pay our bills.” That’ll play well in Peoria. While this quote won’t sink Hilary’s campaign, it does offer a taste of what may come from his mouth in the months ahead. It will certainly be used over and over by the Republicans to portray the Clintons as rich and out of touch.

5. Benghazi (and general track record) – In aggregate, Hillary Clinton’s role as Secretary of State is regarded favorably and without much controversy with one big elephant-in-the-room exception – Benghazi. This was of course the unfortunate turn of events that led to the deaths of U.S. Ambassador J. Christopher Stevens and three other Americans when the U.S. diplomatic mission in Benghazi, Libya was attacked. We are going to reserve analysis of the events, but believe this will become a major thorn in her side, especially as it gets into the nitty-gritty of the campaign post the nominating conventions. The downside of having a track record is that in can and will be scrutinized under a microscope and Benghazi remains a major issue.

Despite these five key challenges to Clinton’s candidacy, make no mistake about it: this remains her race to lose.

Daryl Jones is the Director of Research at Hedgeye Risk Management.