This note was originally published May 14, 2015 at 07:28 in Healthcare

SUMMARY

We have had numerous discussions about ATHN over the last several weeks with some of the top shareholders and most prominent bears. What is clear from these discussions is that there is a large duration mismatch between the timing and expectations of how the bull and bear thesis play out. Many of the metrics the bears are looking to as catalysts in the short-term are known to long-term shareholders, but largely dismissed due to greater emphasis on the TAM. This lack of consensus among investor types appears to be the reason why the forward 12-mo excess return of the stock is positively correlated with short-interest. It seems that absent a complete derailment of the growth story, the probability of mass capitulation on the long side is low.

POINT COUNTER POINT

We have summarized the bear and bull arguments from our discussions below. Please let us know if you would like to dig deeper on any of these points.

- Rising % of capitalized R&D to ~18% in 1Q15 <- 1Q15 elevated due to recent acquisitions. Investing in the business to drive growth. Company guided ~16% cash R&D expense (~6% capitalized) as they develop their inpatient offering.

- Slowing physician growth <- Not focused on quarter-to-quarter doc adds... more concerned about long-term adoption and strategic direction of the company.

- Company is going to miss consensus estimates for doc adds because they are unreasonably high <- Probably right... but that doesn't mean they will miss revenue guidance for the year or next. It is a shame that the Sell Side hasn't figured out how to accurately model the company given the transparency and metrics they provide.

- Not a SAAS company, does not deserve SAAS multiple <- Company's offering is the definition of SAAS, subscription based software service with a single instance, multi-tenant delivery platform. Outsourcing component provides competitive advantage and high multiple deserved given growth and margin opportunity.

- Increased competition from CERN, MDRX and EPIC <- Competition is always a risk, but precedent exists where SAAS companies take significant share quickly away from legacy providers in market's outside of healthcare that are even more penetrated and competitive. Additionally, ATHN's market reputation is high in RCM outsourcing, other companies have tried and failed. Enough share exists outside of EPIC where ATHN can continue to grow and become a dominant player.

- Increased reliance on new products and inpatient opportunity to drive growth <- Ambulatory opportunity remains significant, continued cross selling, while the company is taking the right approach in tackling the inpatient opportunity. Under 100 bed hospital market is large and underserved, EPIC not a major player, and ATHN can take share by altering the cost curve and value proposition.

- West Penn Allegheny ~600 athenaCollector customer disconnecting <- Not concerned with variability in doc adds in the short-term.

- Jonathan Bush commentary on 1Q15 earnings call related to lack of urgency due to no government mandates causing drop in close rates <- Largely expected given lack of federal mandate. Core business is Revenue Cycle Management and is much less dependent on EHR incentives. ICD-10 is likely to be a short-term catalyst.

- Jonathan Bush commentary around variability in Enterprise bookings <- Enterprise bookings are lumpy, this is a known fact, and something the company has been very straight forward about over the years.

- Epocrates has been a disappointment with sales declines in excess of -20% in 2014 <- Epocrates is doing what it was meant to do... That is, provide the company with access to a network of over 300k physicians, spread awareness and drive lead generation for core, athenahealth branded products. Epcorates sales actually grew 2% YoY in 1Q15 and positive bookings commentary is encouraging. Much of the sales decline was due to management deciding to walk away from certain parts of the business.

- Not getting any traction with Enterprise Coordinator <- Still early days with population health and they have a really good product. Change in go-to-market strategy makes sense and should lead to shorter sales cycles by splitting the referral management and population health components.

- They are a phone bank with little operating leverage <- athenaCollector gross margin is running in the mid-70s. If you look at the company's P&L on a unit cost basis (e.g., # physicians per direct employee) you can see similar leverage to other SAAS companies. Long-term profitability targets established by the company are attainable.

- Change in revenue recognition timing on Imp & Other boosted sales growth <- Better matches revenue with implementation expense, rather than amortize over the estimated life of the customer.

- Significant cash burn in 1Q15 <- Excluding acquisitions, in-line with seasonal trends due to timing of cash bonuses... cash balance builds through Q4.

- Low KLAS rating for athenaClinicals <- athenaCollector is their core product and is ranked Best in KLAS. 43% of athenaCollector physicians are using athenaClinicals and management is addressing the issue with the roll out of a new interface sometime this year.

- They are giving it away for free <- Industry standard to provide Enterprise clients with discounts... Take rate has increased from 3.7% in 1Q09 to 4.5% in 1Q15.

ownership analysis

We believe it is important to consider ownership before taking a long or short position. Our hopeful thinking is that we better our chances of being right by understanding what drives the buy and sell decisions of those responsible for the stock's fate, and based on the results of our own due-diligence process, align ourselves accordingly.

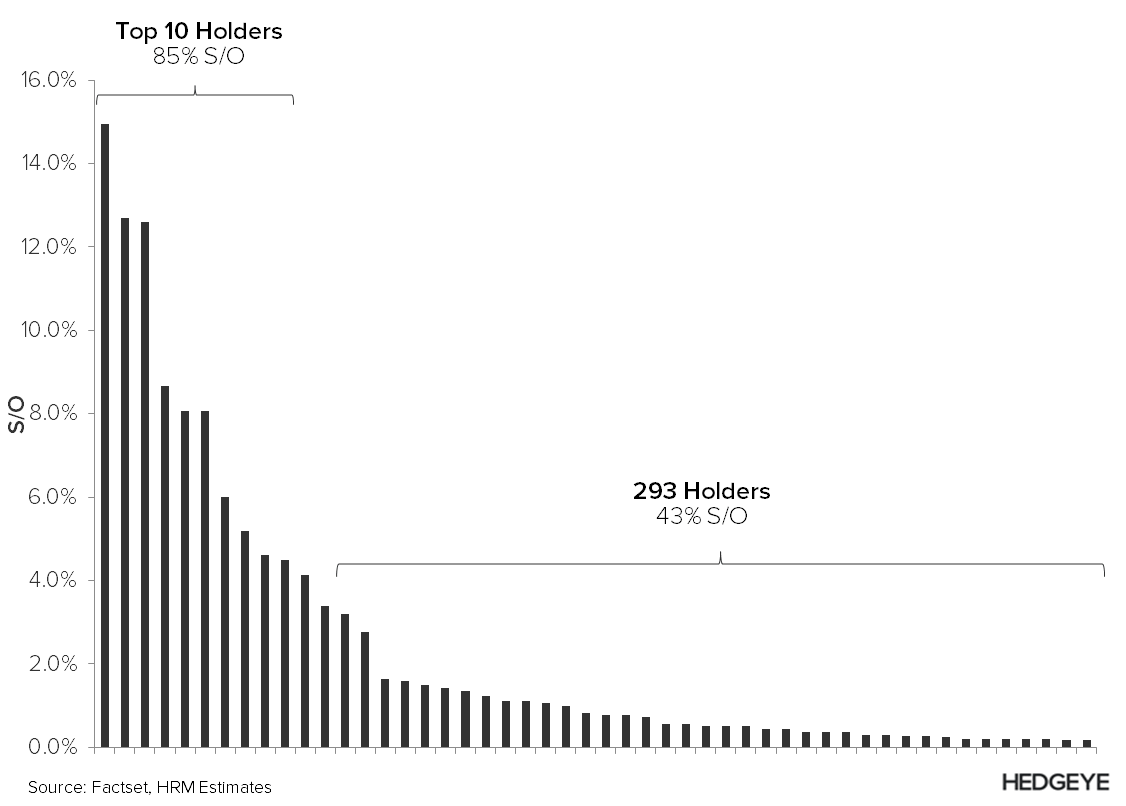

In the case of ATHN, 85% of shares outstanding are owned by the top 10 institutional shareholders with the majority being large mutual funds with long investment horizons. More specific, 60% of shares are owned by funds with a holding period between 2-4 years and 35% have a holding period greater than 4+ years. We compared ATHN to VRX in the chart below to provide context.

conclusion

It seems that absent a complete derailment of the growth story, the probability of mass capitulation on the long side is low. Meanwhile, the positive correlation between short interest and forward excess return suggests that while the bears may control the narrative in the short-term, over the long-run, bulls are often right.

Please call or e-mail with any questions.

Andrew Freedman

Analyst

203-562-6500

@HedgeyeHIT

Thomas Tobin

Managing Director

203-562-6500

@HedgeyeHC