“The men who have changed the world never succeeded by winning over the powerful, but by stirring the masses.”

-Napoleon Bonaparte

Like all of us, Napoleon obviously had his issues. Unlike most of us, he changed part of the world at a time when it needed changing.

In 1799, France was littered with a political elite (The “Directory”) that plundered its People with a Policy To Inflate. Most British historians of the Napoleonic era missed that part. That’s because they were writing from their own aristocratic perspective.

Ah, the historical perspective. If you want to stir the masses in America like JFK or Reagan did (or like Thatcher did in the UK), promote the truth about a #StrongCurrency. It ensures the purchasing power of the many, at the expense of the political few.

Back to the Global Macro Grind…

If only because the Eurocrats were Burning Euros yesterday, it was a great day for Americans who don’t get paid by the edifice of asset price inflation. On a US Dollar +1.1% day (EUR/USD was -1.5% at one point):

- The CRB Commodities Index (19 commodities) deflated -1.9%

- Oil (WTI) got tagged for a -3.7% loss on the day

- Coffee and Corn dropped -2.3% and -1.6% in price, respectively

I’m not sure what part of the world you grew up in, but I can tell you that crushing a long-term inflation expectations bubble in food and gas prices would go over quite well in my Canadian stomping grounds.

It wouldn’t go over particularly well in parts of Texas or Alberta, however:

- Oil & Gas Stocks (XOP) led losers at -2.9% on the day

- Energy Stocks at large (XLE) weren’t far behind at -1.4% (in a flat US equity market)

- Oh, and Russian stocks (RSX) dropped -2.3% too

Futhermore, I can’t for the life of me find the part in the Federal Reserve Act of 1913 that states that un-elected-US-linear-economists shall be tasked with upholding levered Energy Junk Bonds and/or “international earnings” from SP500 cohort companies…

In other words, never did so many do so well yesterday, at the expense of the few.

Sadly, this too shall probably pass as the Federal Reserve boxes itself in a corner at this stage of what we have been calling #LateCycle in the US economy – and that’s devalue the Dollar as both US consumption and labor cycles slow.

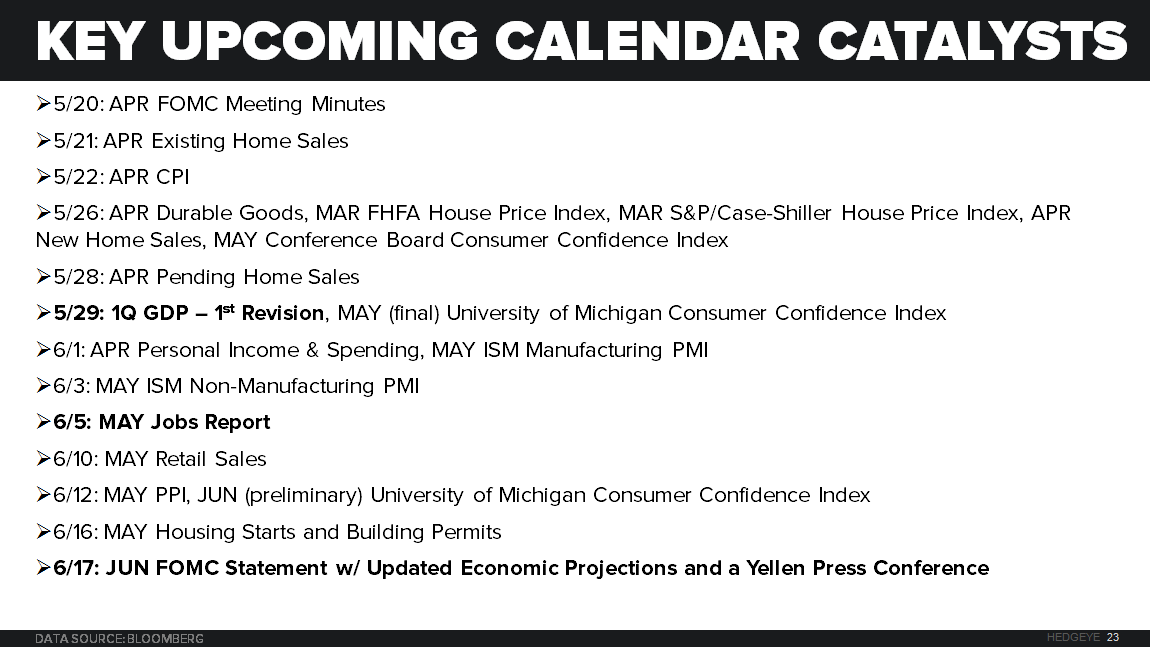

As a reminder, here are your immediate-term Macro Calendar Catalysts for a resumed Down Dollar correction:

- May 29th – ugly headline Q1 2015 GDP report will keep political pressure on the Fed to push out the dots

- June 5th – watch out for the cycle on the labor front; especially if we get the 2nd bad jobs report in the last 3

- June 17th – Fed Day in America (FOMC meeting); sleep in until 9AM and just buy everything

If the European, Japanese, and Chinese central planners don’t come out and devalue, daily, that is…

Looking for immediate-term risk management levels on that?

- US Dollar Index immediate-term TRADE overbought at 96.02 with no support to 92.82

- EUR/USD immediate-term TRADE oversold at $1.10 with no resistance to $1.14

- CRB Index immediate-term TRADE oversold at 224 with no resistance to 234

- Oil (WTI) immediate-term TRADE oversold at $56.14 with no resistance to $61.37

- Gold immediate-term TRADE oversold at $1200 with no resistance to $1239

That’s just the immediate-term though – and if you’re paid to not risk manage that duration (or take advantage of the opportunities it presents), no worries – you probably aren’t reading this anyway.

From a long-term TAIL risk perspective, the onus is definitely on the Europeans (and Japanese) to prove that they aren’t who we think they are – some version of what Napoleon crushed over 200 years ago.

But, other than Warren, who in this business is really allowed to stir the masses with long-term leadership views and skip over everything that could happen until June 17th? I’m not. So, for now, I’ll take our asset allocation to Commodities to its YTD high of 10%.

Our immediate-term Global Macro Risk Ranges (with intermediate-term TREND views in brackets) are as follows:

UST 10yr Yield 1.97-2.32% (bearish)

SPX 2105-2140 (bullish)

RUT 1 (bullish)

DAX 118 (bullish)

VIX 11.91-14.98 (bullish)

USD 92.82-95.92 (neutral)

EUR/USD 1.10-1.14 (neutral)

YEN 118.91-120.99 (bearish)

Oil (WTI) 56.14-61.37 (bullish)

Natural Gas 2.79-3.11 (bullish)

Gold 1 (bullish)

Copper 2.78-2.91 (neutral)

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer