At face value, a company putting up 9% revenue growth and de-levering to 4% EBIT growth and 7% EPS growth is nothing to write home about. But in this tape, where we’re seeing retailers across the board show weakness on the top line, lower margins, higher inventories, and in many cases, earnings below last year, we think the DKS 1Q15 print was actually not half bad. Something that is ‘not half bad’ is hardly our benchmark for an investable idea. But for the most part, the print was in-line with what the company outlined at its analyst event just one month ago.

Taking a step back, we’d been perennial bears on DKS, but after digesting the content from the investor day we turned much more constructive on the DKS story. It’s not one of our top ideas (at this price), but this is perhaps the first time in many years that DKS set the bar for long-term growth and margin expansion at a level that is beatable. There was absolutely nothing that came from the print today that changes this view.

Clearly, people were not happy with the fact that the comp came in below the top end of the guided range (a whopping +1%), as well as the company’s posturing that it will be tough to recapture the margin lost when the golf/hunt categories collapsed last year. We’re less concerned than DKS is leading the investment community to be on the Gross Margin issue.

Specifically, Golf and Hunt combined accounted for about 30% of total sales, which were collectively down last year by 10-15%. The company suggested that this cost about 40-50bp in margin, but we disagree. The incremental margin on this lost business won’t be a simple 10-15%, but rather something closer to 30-40%. That suggests to us that the margin hit was anywhere between 140-180bps. That’s definitely something to keep in mind in the context of a 3-year 110bp margin improvement target. DKS could potentially get there in half that time.

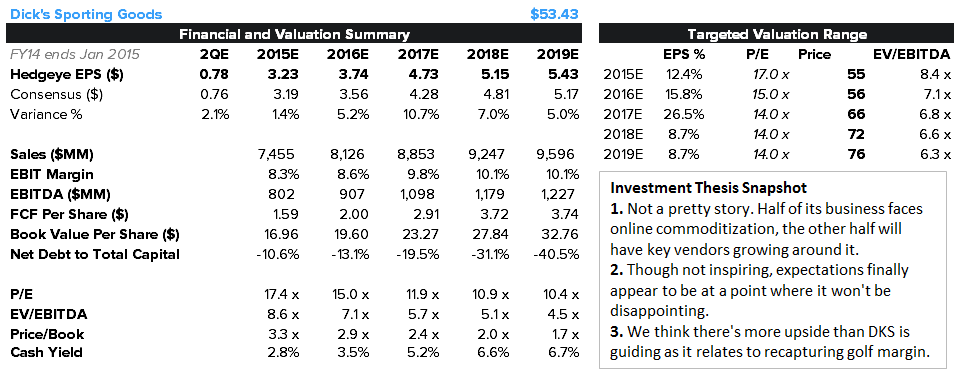

As for the model, we have the company at $4.73 in 2017, which compares to the consensus at $4.28. If we had to pick either $4.50 or $5.00, we’d take the Over. With the stock at 15x next year’s EPS and 7.1x EBITDA, we actually think that this name is bordering on cheap given the likely earnings upside.

To get bigger here, we need more confidence in the top line trajectory – not necessarily that the company will beat, but that it won’t miss in 2Q when compares get very tough. It’s probably not a rush to get into the name – so we’ll dig deeper where we need to. But it definitely gets interesting on sell-offs like today.

Here Are Some Puts/Takes for This Quarter

1) Dick’s Inventory Looks very clean. The sales to inventory spread for the consolidated company was the best number we’ve seen since 1Q12. And management noted that Dick’s sales growth was ahead of inventory growth during the quarter. That’s a bullish gross margin set-up coming out of a quarter where merch margins cost the company 56 bps of gross margin. Now the company is lapping the elevated promotions in the golf department (which account for a large part of the 112bps of merch margin dilution in 2Q14) with a clean balance sheet.

2) Hunting done? Field and Stream will account for about 20% of the unit growth over the next 3 years. We’ve heard a lot during the Analyst Day and on the call about the long term opportunity for this and side-by-side Dick’s/F&S concepts, but to us it sounds like Field and Stream is the dumping ground for lower margin, slow turning categories that no longer fits in the core Dick’s concept. We’re trying to keep an open mind as it relates to Field and Stream until we hear more quantified stats, but the initial management commentary on store placement, cannibalization, etc. aren’t exactly bullish. Add to that the fact that management is having internal conversations about what to do with Hunt/Fishing in markets where DKS has no plans to open a Field and Stream and it seems like a category not worth driving capital into. This is all accounted for in our model. But we wish management had better control over where this business is headed.

3) Golf better on the margin. When a CEO stands up in front of Wall-Street and says that a business, which at one point accounted for 20% of consolidated sales, doesn’t have much left to contribute to the portfolio, you’d expect a hugely negative response. But the fact is, we’re talking about Golf at DKS – which most people have written off. On the margin, sales trends QTD are relatively flat and margins are up 100bps 17 days into 2Q. It’s not time to declare victory, but if DKS can continue to push AUR higher in the face of the huge promotional calendar in 2014 it will be a positive margin event. As noted, our math suggests that the combination of Hunting and Golf ate away about 1.5pts of margin during 2014. We have no reason to think that DKS doesn’t recapture 100% of that within 12 months, unless the company has understated the e-commerce investment needed to bring the three urls in house.

4) World Cup? The company will face the World Cup comp in 2Q where sales essentially doubled on a per store basis from the event in 2010. That will be a big headwind to lap if the company can’t manage to keep golf flat for the quarter.

5) E-comm carrying the load. Since the company started reporting a blended ‘omni-channel’ comp in 1Q13, the company has comped positive in its stores just twice. This marks the 7th quarter of negative store comps in the past 9 and 3rd consecutive at the same time sq. ft. continues to grow in the HSD. Over the long term we have a very hard time seeing how online margins are higher online vs. in-store. Yes the GSIC agreement shaves a few hundred bps off of current DTC margins, but when you consider the shipping cost and minimal fixed cost rationalization potential on a consolidated basis as DTC continues to cannibalize in store sales, e-comm = margin dilutive. Our sense is that this will be muddied by the margin DKS will recapture from golf. On a net basis, it should be fine although some of the components are ugly.

6) Occupancy pressure. DKS needs 10% revenue growth to leverage store occupancy, which is a very tough hurdle. Managements 2017 sales targets suggest an 8.5-9.5% CAGR, or a 2-3% comp. We feel good about our assumption for margin upside from golf/hunt. But the comp trajectory is a different story. We’re ok with 2-3%, but it is admittedly a dangerous place to be with DKS. This is probably the biggest risk to our above-consensus estimate. If we see a continuation of what we saw in 1Q (1%), then our numbers are likely too high.