HAIN in on the HEDGEYE Best Ideas as a SHORT!

Being short HAIN has been the pain trade for me.

That being said, the FY15 financial performance (negative earnings revisions and declining margins) over the past 12 months does not warrant a multiple expansion. Unfortunately, over the past 12-months the NTM EV/EBITDA multiple expanded from 13.6x to 16.8x today. At the time of our SHORT call we argued the company was overvalued because the international business (UK) was a slow growing, low margin food business that did not deserve to trade at a U.S. Organic food company multiple.

The exact opposite happened!

To that end, our thesis has not changed but has strengthened over the past six months. The company continues to provide little evidence that they have a sustainable business model, additionally management does not disclose the basic information analysts need to understand what the real organic growth rate is. We believe that there are structural impediments to future margin improvement, making the bull case even more suspect. The biggest impediments to margin expansion are:

- Global geographic diversification put pressure on margins

- The two most recent acquisitions are low margin protein businesses

- The limited supply of global Organic ingredients is hurting gross margins

- Increased trade spending will lower gross margins

According to the current sell-side models the HAIN business model will look very different in FY16 versus the past four years. Frankly, I have no explanation for the change in the sell-side logic other than they need to be bullish on the stock due to its Natural & Organic attributes.

The key components to the changes are:

- Gross margins will expand in FY16 after declining for the past four years

- The company will not be cutting SG&A any more

- Operating margins will expand in FY16 after declining in FY15

The following is a look at why the current models are too aggressive in FY16:

GLOBAL DIVERSIFICATION LEADS TO LOWER MARGINS

Over the course of six quarters (to establish its international business), HAIN bought four international businesses for a total of $600 million.

- October 29, 2012 (2Q FY13) HAIN acquired Premier Food and Jams for $315.8 million.

- On April 27, 2012 (4Q FY12) HAIN acquired Cully & Sully Ltd. for $19.8 million.

- On October 25, 2011 (2Q FY12) HAIN acquired Singapore Food Industries Ltd. from SATS Ltd., for $254.5 million.

- On October 5, 2011 (2Q FY12) HAIN acquired Europe's Best, Inc. from The J. M. Smucker Co.

Importantly, none of these businesses are organic or all-natural. This is in direct conflict to the U.S. business which is primarily Organic and the reason why the UK business should trade at a lower multiple.

Collectively HAIN’s new international businesses are producing low single digit operating margins, while the U.S. is running at 17%. Going forward, with the company now seeing 20% of its revenues coming from international with 1/3 of the margins and another ~12.3% from its latest protein acquisitions with mid-single digit margins it will be hard to grow overall margins. To summarize, HAIN can’t cut G&A to offset the gravitational pull of lower margins or it will sacrifice performance in other areas of the company.

GROSS MARGIN PRESSURE

For the past three years HAIN gross margins have been declining at a fairly steady rate. Since 2Q FY11 the company’s adjusted gross margins have declined from 29.3% to 26.6%, or 270bps. Gross margins are under significant pressure from commodity headwinds, mix shift and increased trade spending. We don’t see these issues abating in FY16. The current consensus sees a dramatic shift in HAIN’s gross margins in 1Q FY16. What has changed in order for management to guide to better gross margins in FY16?

MASSIVE CUTS IN G&A ARE CRITICAL AND UNSUSTAINABLE

Can any company cut G&A at the rate HAIN has and sustain critical mass? Does outsourcing G&A functions create sustainable long term advantage? I feel this is a big risk to the HAIN business model!

Prior to making the series of international acquisition in FY12 HAIN had not relied on G&A cuts to drive margin expansion. Obviously, when they acquired lower margin business they need to cut significant amounts of G&A to prevent the overall margin structure of the company from collapsing. Until FY15 they have achieved the intended goal.

Prior to 2QFY12, over the previous five quarters HAIN had only cut G&A by 9bps. Since 2QFY12 the need to cut significant amounts of G&A has become critical to the overall story. From 2QFY12 to 3QFY15 the company has experienced on average 132bps reduction in G&A. Over that same time G&A has gone from 18.7% to 13.45%, or 496bps.

Over the past 12 months HAIN’s G&A has run has 13.75% of sales, as compared to 20% for most of HAIN non-organic companies and 23% for the biggest organic companies. Either HAIN has figured out a better mouse trap or this company is structurally set up to fail.

Now the company is in a very difficult position, the margins internationally have stopped improving and there is incremental pressure on the margins in the U.S. business. HAIN can’t cut G&A and be a company that is built to last.

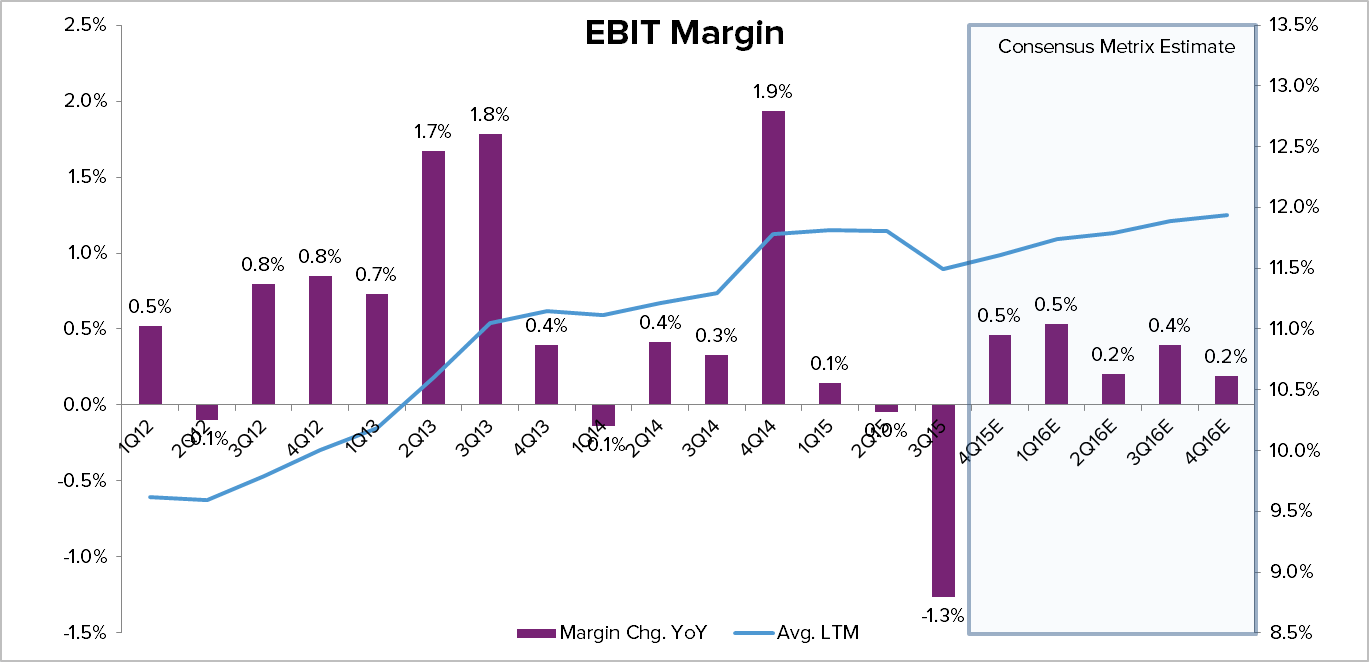

OPERATING MARGINS HAVE PEAKED

Looking forward into FY16 the street consensus has HAIN returning to growth in operating margins. The improvement is entirely coming from improved gross margins, which seem counter intuitive to what is happening in the market place.

HAINS LTM EBIT margins have gone from 9.5% in 4QFY11 to 11.6% in FY4Q15. In FY15 LTM EBIT margins have gone from 11.8% to 11.6%. FY15 will represent the first time in 4 years that the company has not shown margin improvement. Why will the trajectory change in FY16?

Our bottom line for HAIN is that the margin story is over!

When the music stops it's going to be real ugly!

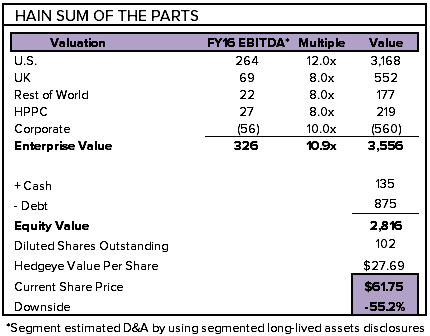

SUM OF THE PARTS

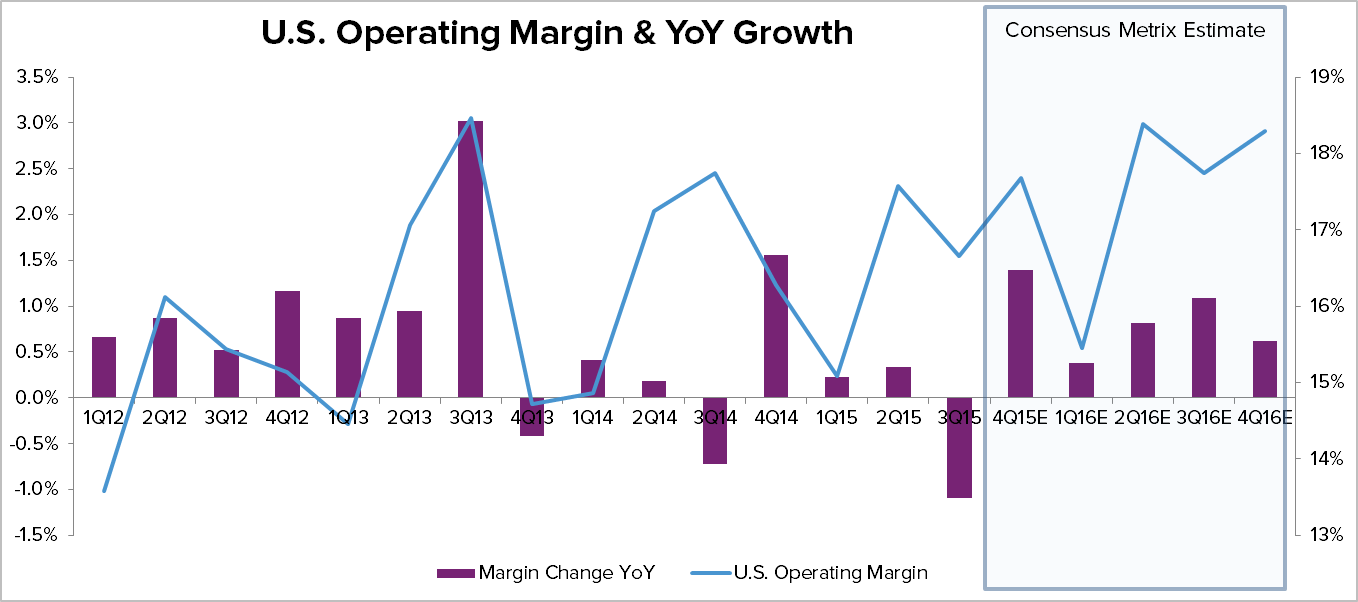

The following charts are a look at the top line growth rate for the HAIN’s important regions. As you can see the two most important markets U.S. and UK are showing a significant slowdown in revenue growth. Importantly, the UK business revenue growth is estimated to slow 1% over the balance of FY16. What is the organic growth rate of a company with 1% revenue growth? And why should it trade at a premium multiple? Even the U.S. business is slowing to the mid-single digits. Again, the company organic growth will not be in the high-single digits in FY16.

What do you pay for a company that is seeing a significant slowdown in revenues and can only grow margins by cutting massive amounts of G&A?

I understand that my bearishness on HAIN ignores the roll-up story and all the hype surrounding the growth taking place in the organic market. At best the UK business is seeing low single digit organic growth of 1-2 and high single digit operating margins. We believe the UK business should trade at a significantly lower multiple than the U.S. business.

Our sum of the parts table is below: