“You are, in a word, constructively-dissatisfied.”

-Jim Casey

After editing the founder of UPS’s famous business-building quote I am, in two words, constructively dissatisfied this morning. It’s the last citation I wanted to highlight for you from one of the better books I’ve read this year, Learn or Die, by Edward Hess.

Per Casey via Hess, here’s the UPS DNA: “Learn, Improve and Adapt” and there are “four primary strands: 1. Mutual Accountability 2. Constructive Dissatisfaction 3. Process Improvement and 4. Employee Centric Culture.” (pg 180)

Casey’s people-model isn’t perfect. No one’s is. But it certainly worked for him and his team. For me, it’s transparency, accountability, and trust. And I can’t give lip-service to that. My teammates and I need to live that out loud, every day.

Back to the Global Macro Grind…

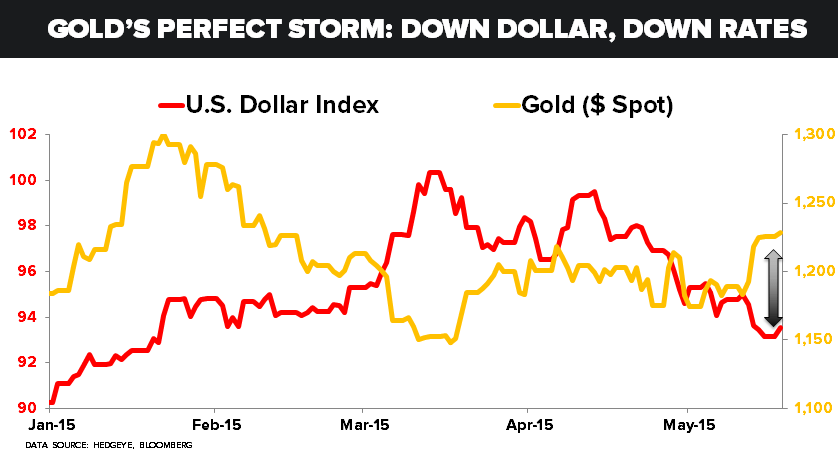

Let’s say I was constructively dissatisfied with how last week went for Global Macro markets. Constructive because I think we made the right research pivot on Dollar Down, Commodities Up. Dissatisfied because devaluing the Dollar isn’t the answer for America’s stagnating economy.

On the heels of an ugly Retail Sales slow-down to 0.9% year-over-year growth (and the worst US Consumer Confidence report of the year via the University of Michigan), this is what the big macro stuff did last week:

- US Dollar Index -1.8% on the week (and now -5.3% in the last month)

- Euro (vs. USD) +2.3% on the week (and now +7.2% in the last month)

- Commodities (CRB Index) +1.0% on the week (+6.9% in the last month)

- Oil (WTI) +0.5% on the week to $59.69 (+15% in the last month)

- Gold +3.1% on the week to $1225

That last one (Gold) was the best performing of the Dollar Down inverse-correlation-love lot … primarily because there was this extra-cherry on top that Gold loves more than anything else. It’s called Down Rates.

Down Rates finally did what they usually do and correlated positively with Down Dollar on slowing US economic data, with the 10yr US Treasury Yield dropping from an intra-week-freak-out-high of 2.36% to 2.14% as economic gravity won, again.

On Friday, the Down Dollar, Down Rates move looked a lot like 2011 all over again. Remember that? Markets did. Financials (XLF) -0.4% on the day vs. Utilities (XLU) +1.3%. It’s the Fed is going to stay Lower-For-Longer move that Hilsenrath confirmed in the WSJ this morning.

Back to the week-over-week moves and how those synched in the land of Global Equities:

- US Financials (XLF) were down in an up tape, -0.2% on the week, staying in the red for the YTD at -0.1%

- US Healthcare (XLV) continued to outperform beta, +1.1% on the week to +8.6% YTD

- European Stocks (EuroStoxx600) flashed another bearish divergence vs Global Equities -0.9% wk-over-wk

- Germany’s DAX lagged its European continent bogey, falling -2.2% on the week

- Emerging Market Stocks (MSCI Index) flagged another bullish divergence vs Global Equities +0.8% on the week

Yep, Down Dollar = Up Euro à Emerging Market Equities beat European Equities.

If you didn’t pick-up on the year I called out, let me hammer the num-lock pad on that one more time: 2011. That was a big year for both Gold and Emerging Markets. It was also a very bad year for Europe and US Financials.

2011 was the year of stagflation being priced into US Federal Reserve Policy. It was the year where the initial Quantitative Easings didn’t provide the centrally planned elixir of a real US growth “recovery” … and The Bernank had to deliver more QE Cowbell.

As markets front-ran the next QE, the US Dollar burnt to a crisp (not mentioned once by big Ben in any of his statements, but it was a 40 year low) and Gold hit its all-time highs. US interest rates hit all-time lows and the Financials posted their widest losses vs. Utilities, ever.

Constructively dissatisfied with that?

If you’re a money manager, maybe not. “Fighting” an easier Fed (read: pushing out the dots, from here, would be an easing, on the margin) has proven to be elusive for most who have expressed their bearishness in 2009-2015 Zero Hedge Bear terms.

But if you’re looking for mutual accountability between policy makers and economic outcomes, you can UPS that request in the mail and kiss it goodbye. Until we have real leadership in this country that gets the difference, in real Dollars, it’s The People’s purchasing power that loses.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.95-2.22%

SPX 2100-2131

RUT 1211-1251

USD 92.84-94.44

EUR/USD 1.10-1.14

Oil (WTI) 55.97-61.57

Gold 1198-1231

Best of luck out there this week,

KM

Keith R. McCullough

Chief Executive Officer