“In order to lead an army, you have to ceaselessly attend to it.”

-Napoleon Bonaparte

The way my typical day goes is as follows: ceaseless attention to Global Macro market moves, news, and analysis in the morning – meetings in the afternoon – and, family, hockey, and #history (in that order) in the eve.

The compare and contrast of the macro morning to a history book at night couldn’t be more drastic. Before bed last night I was enthralled in early 19th century European history (Napoleon, A Life). This morning I feel like I’m watching a version of it 200 years later.

I don’t do it because it’s cool. I do it because I love it. I do this because I’ve realized that every book I read reminds me how much I don’t know. And since I’m leading an independent army against an Old Wall guard that seems to know everything, there’s work to do.

Back to the Global Macro Grind…

Can you contextualize immediate-term market moves within the intermediate-term? How about the long-term? What is the long-term? Is it 3 years or 200? If you could know everything about everything, across durations, I’m betting you would.

Since I write every day, I spend a lot of time trying to contextualize the TRADE (3 weeks or less) within the TREND (3 months or more). But especially during times like these, it’s critical to attempt to have a view of what TRENDs are doing within long-term TAILs.

We define longer-term TAILs as having a duration of 3 years or less. I use that time horizon because A) I really suck at calling things 3 years out and B) unless they have permanent Buffett-like capital, mostly everyone else does too.

So today, to keep it simple, I just wanted to give you my TREND vs. TAIL views, across Global Macro:

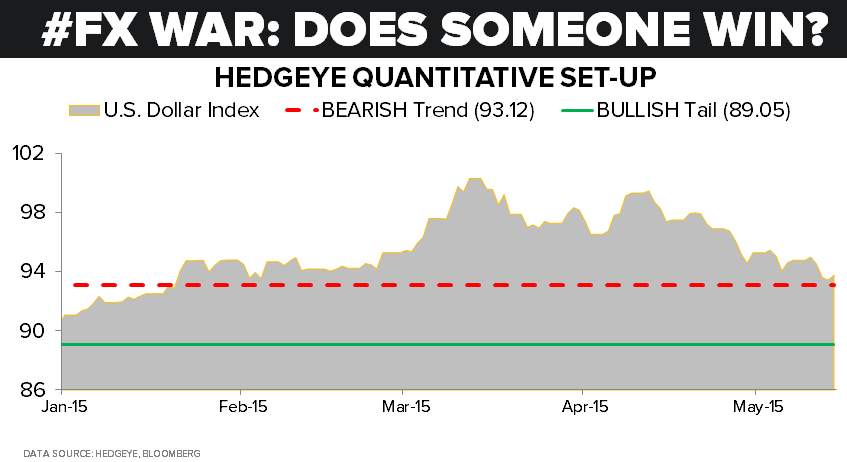

- US Dollar = bearish TREND; bullish TAIL

- The Euro = bullish TREND; bearish TAIL

- Japanese Yen = bearish TREND and TAIL

- US 10yr Treasury = bullish TREND and TAIL

- US 30yr Treasury = bullish TREND and TAIL

- Japanese Government Bond (10 yr) = bullish TREND and TAIL

- SP500 = bullish TREND and TAIL

- Russell 2000 = bearish TREND; bullish TAIL

- US Equity Volatility (VIX) = bullish TREND and TAIL

- Nikkei = bullish TREND and TAIL

- German DAX = bullish TREND and TAIL

- BSE Sensex = bearish TREND; bullish TAIL

- CRB Commodities Index = bullish TREND; bearish TAIL

- Oil (WTI) = bullish TREND; bearish TAIL

- Gold = bullish TREND; bearish TAIL

I better stop there, or I am going to confuse you. I used to get confused by intermediate-term TREND views disagreeing with longer-term TAIL ones. But after building, breaking, and re-building my #process, I don’t dwell on the non-linearity of it all as much.

Most of our confusions have to deal with our own emotional baggage. We are humans, after all. And when something goes one way for a period of time that we think we understand – then it goes the other (that we don’t understand), we get frustrated.

That makes our collective challenge to see the macro market for what it is, as opposed to what we’d like it to be. This is not easy. And it gets a heck of a lot harder if we don’t do the longest of long-term #cycle work to contextualize the “de-couplings.”

I wrote about why I think USD continues lower from an intermediate-term TREND perspective yesterday (Commodities, Oil, Euro, etc. higher), but I didn’t spend any time on why it could strengthen after easier Fed policy and slower growth is baked into consensus.

The longer-term case for:

A) US Dollar Index to put in a long-term-higher-low at around 89-90 on the USD Index (EUR/USD 1.19-1.20)

B) Commodities (CRB) Index to put in a long-term-lower-high in the 248-253 range

C) Oil (WTI) to start to fade and fail at lower-long-term-highs of $69-71

Is as follows:

- Currency War (centrally planned FX devaluations to create growth and inflation) will see Japan, Europe, and the USA fail

- As each of the 3 majors sees growth and/or inflation slowing, they’ll take their turn with more of what has not worked

- In the end, the US has the best demographics of the 3, so they’ll have the best real growth of the 3 (and strongest currency)

The most important words in those 3 points are “they’ll take their turn.” In almost every macro strategist/economist piece there is either a complete disregard for that and/or a blind faith that real economic growth will be born out of these policies to begin with…

Look up the Wall Street Journal article this morning on US “Economist’s Expecting Recovery”:

- US economic growth to magically re-accelerate to +3.0% year-over-year in 2nd half of 2015

- US non-farm payrolls (NFP) to average 223,000 for the rest of 2015

- A “Strong Dollar” to weaken, which was the “headwind” to the US economy in Q1 2015

Meanwhile, the Hedgeye Predictive Tracking Algorithm has US GDP growth at +1.8% year-over-year growth in 2H 2015 and we could easily see non-farm payrolls at half of that expectation, in our most bullish case.

If I rattled off the Japanese and European “economist” expectations, the only ones that are in the area code of close are Japan’s. But that’s only because they have been forced to predict that none of this “growth” policy has worked for 20 years!

I realize this is the longest Early Look of the year. My apologies for that. If you’d like to ceaselessly stare at the S&P Futures, please refer to our risk ranges. Buy at the low-end (sell at the high-end) of the range, but please pay attention to TRENDs and TAILs too.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.95-2.31%

SPX 2098-2129

RUT 1

Nikkei 19199-20024

VIX 12.11-15.67

EUR/USD 1.10-1.14

YEN 118.77-120.58

Oil (WTI) 55.67-61.60

Best of luck out there today and enjoy your weekend,

KM

Keith R. McCullough

Chief Executive Officer