Below is the breakdown of this morning's initial claims data from Joshua Steiner and the Hedgeye Financials team. If you would like to setup a call with Josh or Jonathan or trial their research, please contact

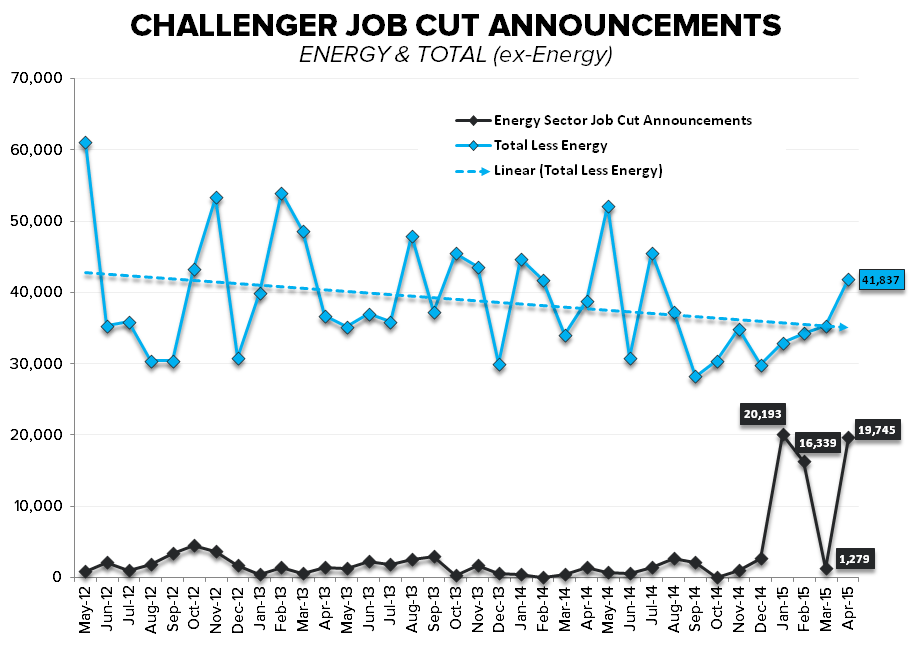

JOB SEPARATIONS: AGGREGATE vs ENERGY

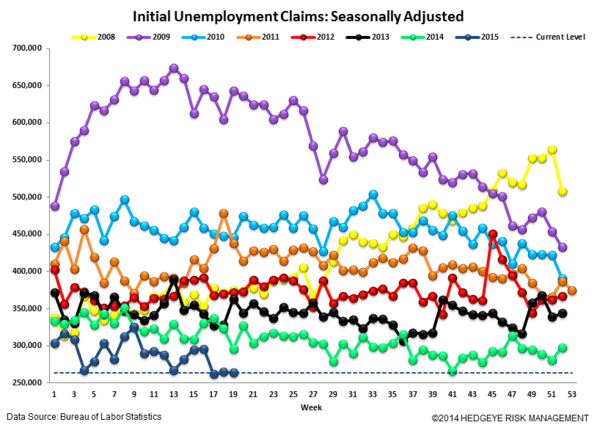

Claims improved once again last week, falling to a seasonally adjusted 264k, continuing an impressive push below the frictional floor of 300k.

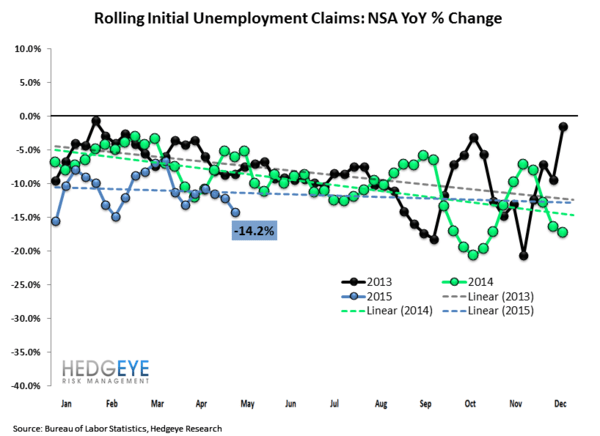

In the first chart below, we show that the spread between our indexed basket of energy state claims and the U.S. as a whole has tightened for the last few weeks, moving from 31.8 on April 11 to 24.8 on May 2.

However, the second chart below shows that the labor market in the energy sector worsened again in April. Job cut announcements in the energy sector had been running at 16-20k/month in January and February, but then appeared to show some glimmer of improvement when they fell to 1k in March. That didn't last long, as the latest data shows 20k more energy workers let go in April.

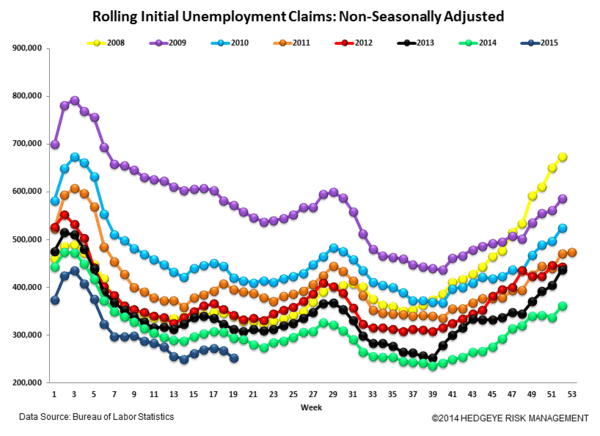

The Data

Initial jobless claims fell 1k to 264k from 265k WoW, as the prior week's number was unrevised. Meanwhile, the 4-week rolling average of seasonally-adjusted claims fell by -8k WoW to 272k.

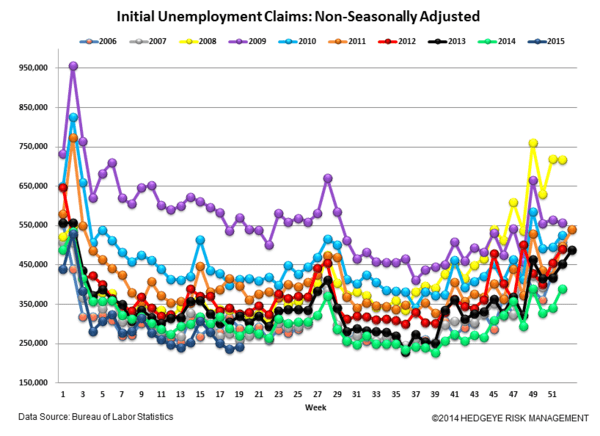

The 4-week rolling average of NSA claims, another way of evaluating the data, was -14.2% lower YoY, which is a sequential improvement versus the previous week's YoY change of -12.2%

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT