A lot of people have asked me recently about insider selling at Nike. Here’s some history as to the one-two punch of insider selling vs. company stock repo. There are some key considerations this time around.

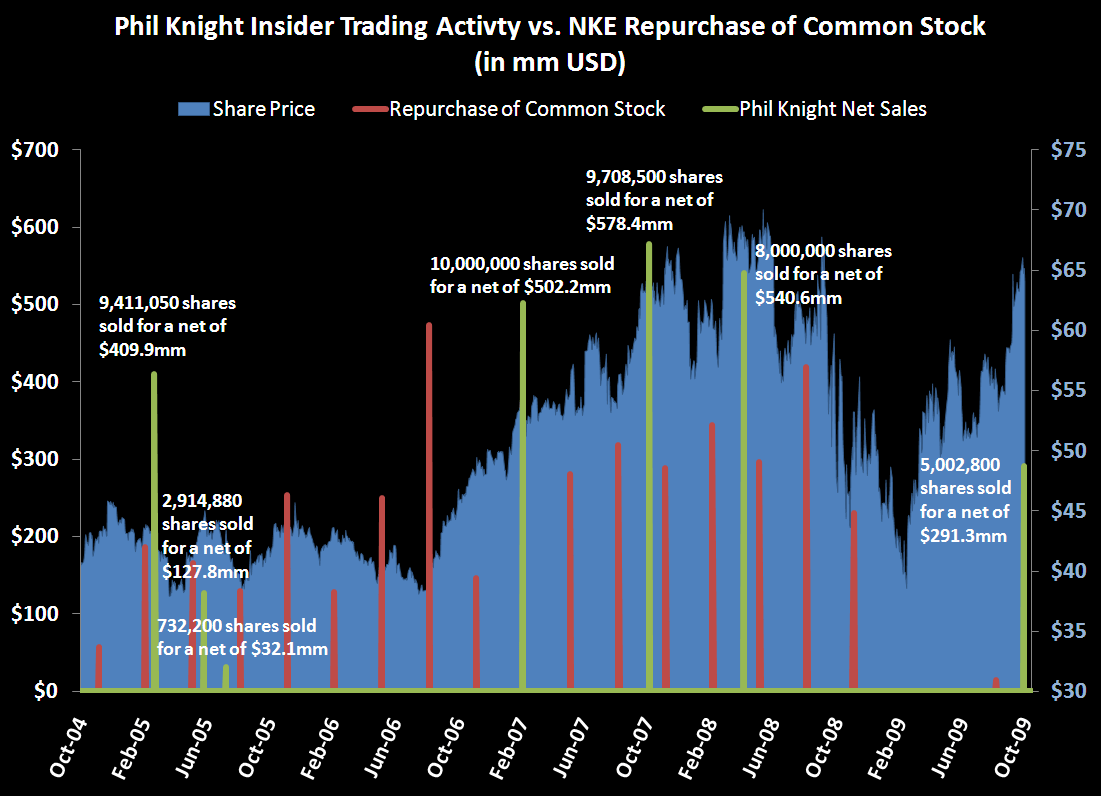

Phil Knight is such an icon in the footwear industry – not to mention the holder with majority voting interest. Mr. Knight has not been a ‘serial seller’ of his stock, and in fact hardly sold any in the open market in the first 30-years of his company’s existence. But since he began, he’s sold stock equating proceeds of about $2.5bn (yes – BILLION). Kind of mind-numbing, really, for a guy that started to sell shoes out of a van. Here’s the part where I bring up that these sales are under a 10b5-1 plan, meaning that it is not Mr. Knight that pulls the trigger, but rather a financial advisor that handles Mr. Knight’s estate planning. Like it or not, the guy is good. His timing has been far better than plans we’ve seen for other executives in retail as well as other industries. But what does that mean? Regardless of who is pulling the trigger, these sales have been timed well in the past.

What’s interesting is that it’s been 17 months since he’s sold a single share. It has been a rarity to see a plan like this executed over time just before a meaningful near-term run up in the stock.

It’s interesting to stack this up against Nike’s own repurchase activity. The facts and numbers don’t lie on this one. In all but one traunch of Mr. Knight’s arms-length selling, Nike was in the market buying shares. Perhaps this is as simple as the company offensively using its bullet-proof balance sheet to mitigate volatility among investor concern about its Chairman selling stock. What we also know is that NKE has not repo’d any shares of substance since Oct 2008. We don’t know the current quarter’s numbers yet. But I’ll be concerned if we see the company not buying any stock, while insiders are selling, AND cash is sitting on its books collecting less than 1% interest.

Definitely something to consider.

Darius Dale