If you can’t make money in stocks or bonds, what do you do?

This is one of the main reasons we have been steadily raising cash to the highest level in our Hedgeye Asset Allocation Model of the year.

62% to be precise.

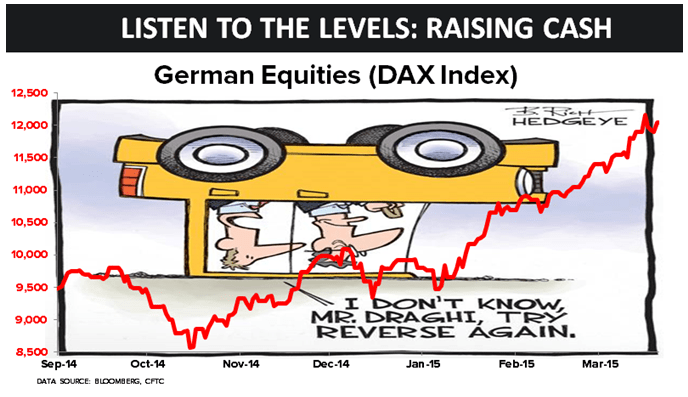

Over in Europe, stocks continue to break our immediate-term TRADE lines of support with the German DAX leading losers this morning down -2.3%. If ECB Mario Draghi lets Euro rates do this, he’ll let stocks drop faster.