Below is the detailed breakdown of this morning's initial claims data from Joshua Steiner and the Hedgeye Financials team. If you would like to setup a call with Josh or Jonathan or trial their research, please contact

APRIL: STRONG....& LONG:

April finished just as strong as it started. As we have pointed out in the last few weeks and show in the first chart below, in terms of cumulative initial claims April 2015 has been the best April since 1996 with the small exception of 2000 (with which it's almost tied). We now look to the jobs report on Friday to see if claims strength with show up in the overall employment situation.

One thing to note about tomorrow's NFP report is that it will have 5 weeks in it vs the normal 4. The BLS corrects for this, but in years when an April with 5 weeks follows years with a 4-week April data problems have tended to ensue. Remember that the establishment survey measures from the weeks of the 12th to the 12th. As such, it's possible that there will be an upward bias to tomorrow's number on the order of ~25% owing to the inclusion of the additional week. We continue to rely on claims as our primary indicator of the Labor market's health.

In the second chart below, oil prices have made steady progress upward of late. Given that movement, the spread between the indexed basket of claims in energy-heavy states and the U.S. as a whole tightened week over week from 28.1 to 26.6.

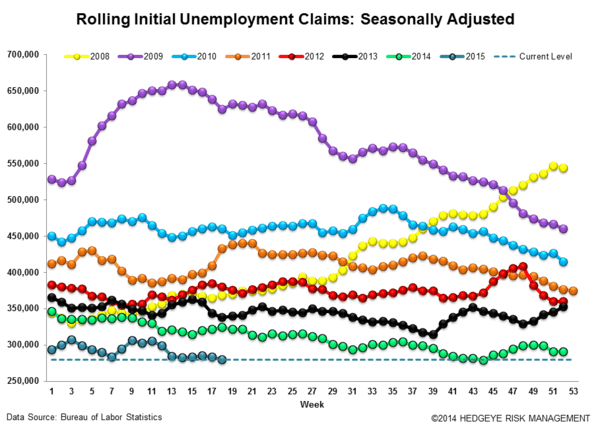

The Data

Initial jobless claims rose 3k to 265k from 262k WoW, as the prior week's number was unrevised. Meanwhile, the 4-week rolling average of seasonally-adjusted claims fell -4.25k WoW to 279.5k.

The 4-week rolling average of NSA claims, another way of evaluating the data, was -10.8% lower YoY, which is a sequential deterioration versus the previous week's YoY change of -11.6%

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT