KEY POINTS

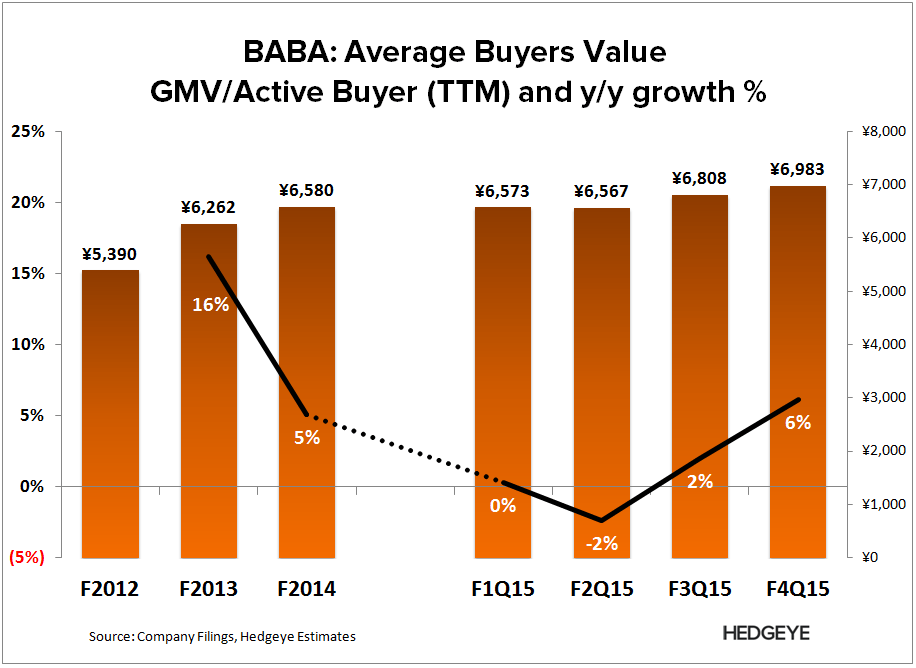

- 1Q15 = MARKED IMPROVEMENT: China Retail revenue growth accelerated off F3Q15, despite a slide in total GMV growth to 40% y/y (vs. 49% in the prior quarter). Commission revenue growth held steady from the prior quarter off a rebound in Tmall Mix (y/y change); suggesting the company may be making improvement in Tmall uptake on the mobile platform. Marketing improved off a moderating y/y decline in desktop take-rates. The biggest surprise from the quarter (for us) was the surge in average spending, which was up 6% y/y on a TTM basis. We can’t explicitly calculate the quarterly trend off the reported data, so we’re not sure if this is the beginning a of positive inflection, or a mirage from the GMV strength earlier in F2015.

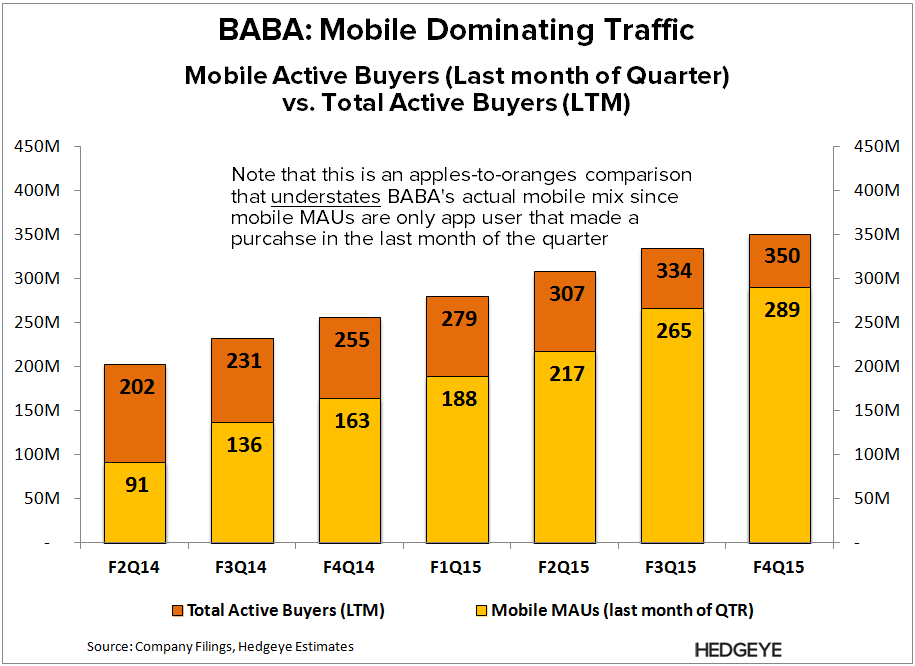

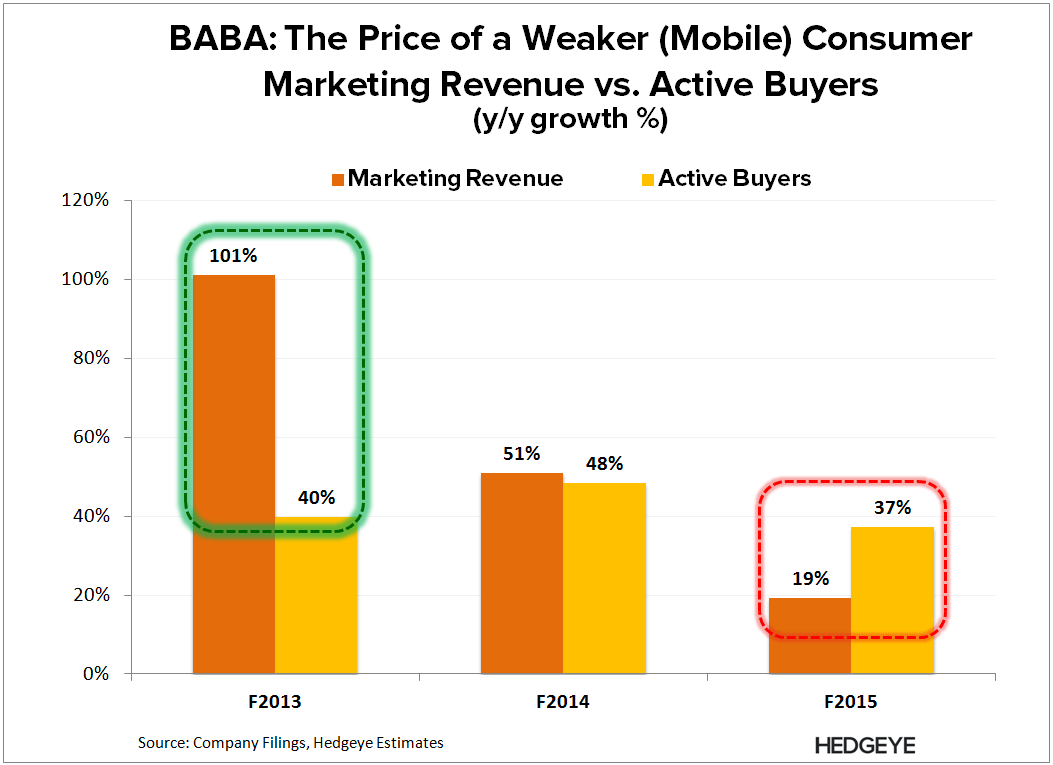

- THE MOBILE DEBATE: Can mobile monetization rates catch up to desktop, particularly on the advertising side since? We believe much of the improvement on mobile take-rates has to do with the migration of consumer traffic (ad click volume) to mobile. Management suggested as much on the call, but also spoke to improving demand from merchants for mobile advertising. The latter is encouraging, but we have a hard time believing that mobile will approach desktop rates that are more than double that of mobile. Traffic has been the predominant driver of growth, and mix is already over 83% of active shoppers (vs. 64% in the prior year). See note below for detail.

- IPO YO-YO: BABA beat top-line estimates by 5% in F2Q15; consensus estimates rose in response. On the F3Q15 print, BABA missed by -5%, then estimates came down significantly. BABA just beat F4Q15 revenues by 4% on reduced consensus estimates, and we’re expecting consensus revenue to shoot back up in response. Note that the prior estimate cut following the F3Q15 release was concentrated into F4Q15 and F1Q16, so if estimates do rise as we expect, the setup will get progressively worse starting in F2Q16.

BABA: The Mobile Debate

03/04/15 10:34 AM EST

Let us know If you have any questions or would like to discuss in more detail.

Hesham Shaaban, CFA

@HedgeyeInternet