Below we outline the quantitative signals and less importantly the fundamental story that supports the counter-TREND move in oil since the Fed’s March 18th meeting.

Without a near-term central-planning catalyst we view Friday’s non-Farm payrolls report as a key indicator for the direction of the USD which is near testing its intermediate-term TREND level of support at $93.12. Inverse correlations to commodities have also reverted to more normalized levels over the near-term, making the direction of the currency in the aftermath of Friday’s report telling for developing a more finite view on oil prices.

If you didn’t have a chance to view this morning’s macro call live or catch up with the Early Look commentary from KM, it’s worth a read as we verbally debated the meaning of the extended counter-TREND moves in commodities, the dollar, and interest rates:

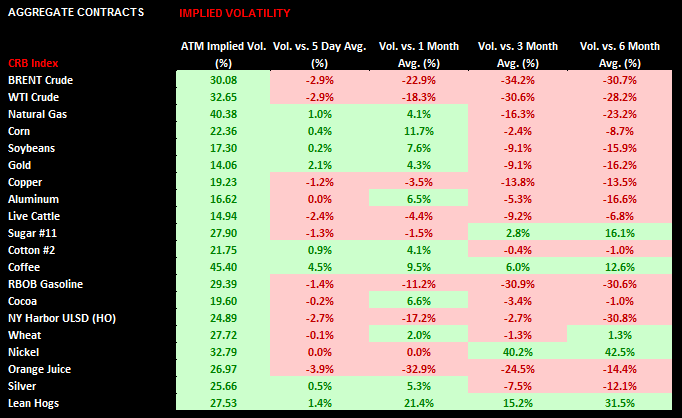

"From SEP 2014 to FEB 2015, Oil Volatility (OVX) went from 17 to 63 = +270%.

From FEB 2015 to now, OVX dropped from 63 to 36 = -42%."

With WTI moving above its own TREND resistance level, our risk ranges remain very wide over the intermediate-term with the shorter-term market signals more confirming of a move higher. The market signals that have accompanied the move higher are similar to the November-January signals that accompanied the move lower.

Specifically, oil is making a series of higher lows and higher highs in the last several weeks on healthy volumes and tighter ranges, or compressing volatility (both realized and implied). Since March 17th (pre-Fed meeting), here’s how the signals shake-out:

- Price: Positive daily returns skewed to the upside

- Volume: Ratio of Green Day Volume/Red Day Volume= 1.2

- 22 days of positive returns: 832,903 ADTV (Contracts)

- 11 Days of Negative Returns: 699,022 ADTV (Contracts)

- Volatility: historical volatility has compressed along with OVX despite healthy volumes (See the link to our Slide Deck and Commentary from April 24th below).

On April 24th we blasted a video and slide deck outlining these conflicting signals in more detail:

1) Conflicting quantitative signals in oil markets (Against our bearish call)

2) The importance of yielding to top-down macro over the push-and-pull of global supply/demand narratives. The replay link and slide deck are included below.

------

On the fundamental side of global energy markets we re-iterate that supply/demand adjustments will continue to smooth on a lag. Although much lower on the compendium of important factors to our process, the fundamental supply/demand picture DOES suggest more support for oil prices than it did in January:

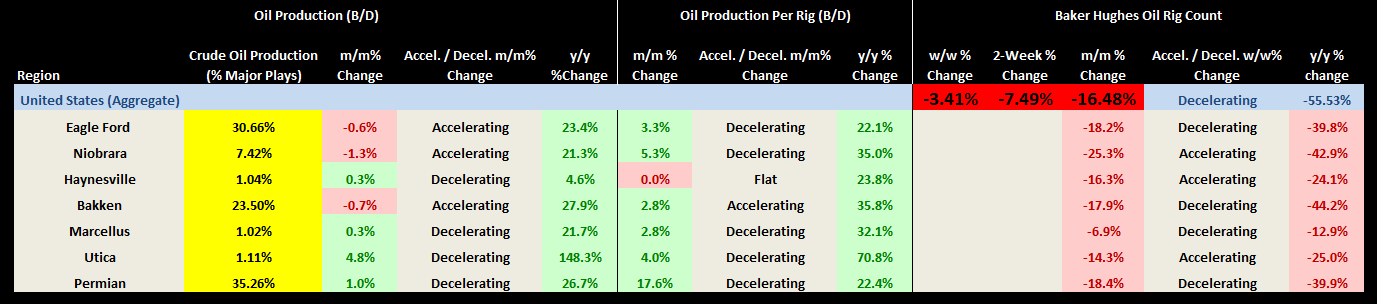

- Domestic crude production has gone from a linear increase, to decelerating, to now topping IN REACTION to a financial market fueled sell-off (Note below that the supply/demand picture is not that much different than it was last summer). The extra YY incremental barrels are without a doubt fueled by the U.S. shale boom, making the U.S. production slowdown a meaningful psychological catalyst supporting prices.

- Crude oil rigs in service, albeit not a proxy for production, are 42% of the October highs (679 vs. 1609).

- Last week was the first inventory flush in Cushing since the end of November and this week marked the first aggregate inventory flush since January 2nd

------

Oil prices will continue to move up and down and back again but all-in-all our historical cycle suggests anchoring on the direction of major currency moves is the most-sound tools for developing the right bias to risk manage the longer duration moves in commodities. Friday’s jobs report will be an important jobs report and one the Federal Reserve will be watching closely.

Ben Ryan

Analyst