Editor's Note: This note was originally published on February 18, 2015 at 12:22. Shares of NDLS are down 36% since.

Last week we elevated a number of troubled growth stocks to our Investment Ideas list as shorts. Among these was NDLS, a name we see approximately 35-45% downside in with a fair value of $14-16 per share.

NDLS is a small cap stock that has been the recipient of an unwarranted premium growth multiple. With only ~440 Noodles & Company restaurants system-wide, management maintains that they have a tremendous runway of growth ahead of them that calls for “at least” 2,500 restaurants nationwide. This is a lofty goal, by any measure, particularly when considering the recent surge of competitors claiming similar domestic growth profiles. We’ve already seen signs of how difficult this will be to achieve in NDLS’ infancy as a public company. As the company has accelerated unit growth and ventured into new markets, system-wide sales and margins have suffered.

While this is to be expected, the company believes it is facing a brand awareness issue and thinks it will solve this issue through increased marketing spend and its catering initiative. In our view, NDLS' brand awareness problem shouldn’t be management’s top priority. In fact, elevating brand awareness will not be the panacea most hope. Execution and site selection are the real deterrents to the business, and these can’t simply be fixed by plowing more cash into advertising.

Despite bullish consensus estimates, we believe NDLS is facing a difficult 2015 for the following reasons:

- Cost of sales inflation: management is only estimating 2% food inflation, but durum wheat prices are under pressure and food cost estimates could head higher as we move into the back half of the year

- Geographic concentration: the company has a notable number of stores in the DC metro area, which is an extremely competitive market

- Rising labor costs: 52% of company operated restaurants are in markets that are facing minimum wage increases in 2015 or 2016 (or both), the majority of which are coming this year

- The Affordable Care Act: will add about 30-50 bps of pressure on margins in 2H15

- Estimates are high: the street is looking for 27% EPS growth in 2015, after an essentially flat year in 2014

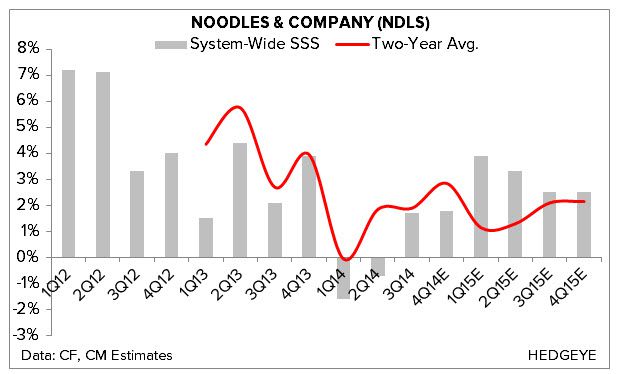

Management is currently guiding to between 20-25% EPS growth in 2015. With very little flow through from same-store sales, NDLS needs to drive 3-4% comp growth in order to keep margins flat versus last year – a task we feel will be difficult to achieve.

The biggest factor working against us on the short side is the amount of short interest in the name (~25%). The analyst community is rather divided, with a 60%/40% split on buys vs holds, respectively.

Consensus Estimates for 4Q14 Look Aggressive As Well

As a part of our process we continually monitor consensus estimates for each of the major line items on the P&L for the vast majority of companies in our space.

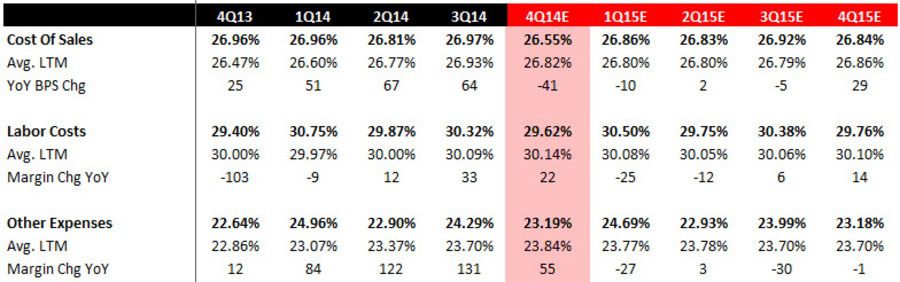

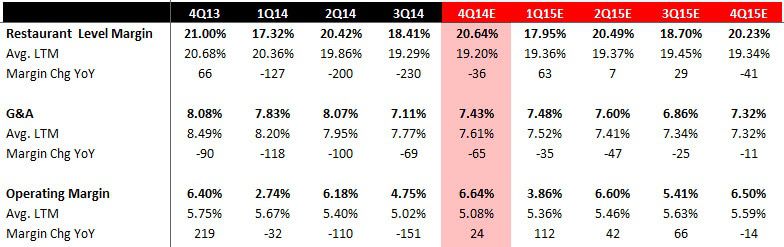

In regards to NDLS, we have a difficult time understanding the rationale behind the street's estimates for COGS and, subsequently, restaurant level margins in 4Q14.

Consensus expects cost of sales to decrease 41 bps on a YoY basis in the quarter, after increasing 51, 67, and 64 bps in 1Q14, 2Q14, and 3Q14, respectively. We've tried, numerous ways, to reconcile the extent of this sudden reversal - but to no avail. Predictably, this leverage is expected to flow through to restaurant level margins which consensus expects to be down 36 bps YoY, after decreasing 127, 200, and 230 bps in 1Q14, 2Q14, and 3Q14, respectively.

We think there is a material disconnect here which will become readily apparent if NDLS does not put up a well-above consensus comp.

Data: Company Filings, Consensus Metrix Estimates