“I have not failed. I’ve just found 10,000 ways that don’t work.”

-Thomas Edison

If you analyze every line item of what I like and don’t like right now, there are plenty of things that aren’t working. Unless you’re raging Long Chinese stocks and Commodities vs. Short US/European Stocks (and Bonds), you probably have some issues too.

In the last week the US Dollar has completely dislocated from what was a consistent and correlated moved with US interest rates. What was the #StrongDollar Deflation (one of the biggest macro moves in a decade) has morphed into Down Dollar, Up Rates.

But is the US Dollar down ahead of another weak US jobs report? Or are Rates Up ahead of a good one? I can’t give you 10,000 different ways to ask me those two very basic questions – but in the last week, I’ve fielded hundreds of them!

Back to the Global Macro Grind…

Some people say that part of the value I provide is my unique perspective. Unlike many macro economists, strategists, and chartists, I am a former hedge fund guy who has made almost every mistake you can make, using live ammo.

Setting aside all of my human flaws, I think most of you (buy-siders) can empathize with getting things wrong. It’s only on the sell-side where the pace of improvement in Macro Strategy has been stalled by not accepting mistakes and learning from them.

As one of the bigger buy-siders (Ray Dalio) wrote in Principles: “At Bridgewater, we created a culture in which it is ok to make mistakes, but unacceptable not to identify, analyze, and learn from them.”

Roger that, Ray.

One of the mistakes I made recently was underestimating how our fundamental research call (#LateCycle Growth Slowing) would impact the USD/Oil trade.

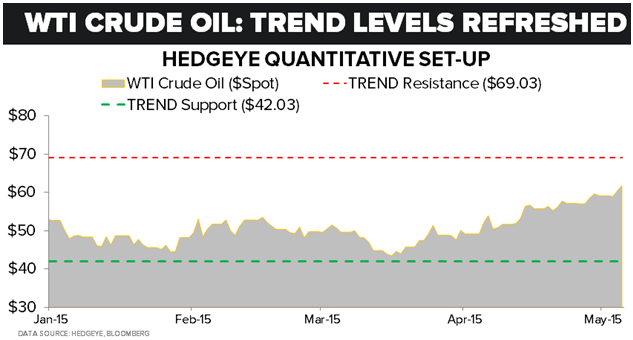

From an intermediate-term TREND perspective, I thought Oil (WTI) would settle into a range of $36-57/barrel. This morning, on another Down Dollar move, Oil is up another +2.5% to $61.91.

You can apply creative writing skills from your no-buy-side-P&L-experience all you want, but from where I was born/raised in this business, this is commonly called being wrong (until you have the mental humility to change your mind).

So here’s my mind-changing this morning:

- Intermediate-term TREND price deck for Oil now = $42.06-$69.03

- Intermediate-term TREND risk range for the US Dollar Index = $90.29-100.03

- Intermediate-term TREND risk range for 10yr US Bond Yield = 1.73-2.39%

My mind changes every day actually. As price, volatility, and economic data changes, what do you do, Sir or Madame?

The first thing you’ll probably notice about my intermediate-term view is that:

A) It’s more in line with the Global Macro reality of the last 6-12 months than the last 6-12 weeks

B) And that the intermediate-term risk ranges are wacky wide

#WackyWide risk ranges are leading indicators for rising volatility. And rising volatility perpetuates mistakes.

To be clear, my mistake wasn’t being short Oil for this entire move up (we covered commodity shorts ahead of an easier Fed and #LateCycle Labor reports, for a trade). It wasn’t being long it at $100 either. It was in not being long it from $45 to $62.

My main mistake there was that I didn’t think Oil’s Volatility was going to compress almost as fast as it exploded to the upside. To put the volatility of volatility (in Oil) in context:

- From SEP 2014 to FEB 2015, Oil Volatility (OVX) went from 17 to 63 = +270%

- From FEB 2015 to now, OVX dropped from 63 to 36 = -42%

Every buy-sider who survived the 2007-2009 gets that unless you were on the right side of the decline, it was hard to run out and buy something with historical volatility of 20-30, never mind 63. This #behavorial reality leads me to more of a question (from here) than an answer as to whether or not I should buy Oil with upside to $69.03, when the downside is still $42.06.

Did the guys/gals who bought Oil and its cyclically related inflation expectations exposures (E&P MLP stocks, Energy Junk Bonds, Levered Long Oil Futures, etc.) down at $45 own it from $90 to $45? Or are we talking about a whole new investor class who nailed it both ways? While I’m not certain about anything in this profession, I’m pretty sure long-term Oil bulls averaged in.

Of all the mistakes I’ve made, averaging into losers is by far the most punishing. Especially when I’d have our funds in smaller cap exposures, doubling and tripling down on mistakes could make them all the more severe. Sure, I could tell my partners that I wasn’t wrong. I could say I hadn’t really failed (yet). But the #truth happens on the next decline, when you can’t get out.

When my Global Macro model says lower-for-longer on both US and Global Growth Rates… and every central planner on the planet is trying to “ease” the confusion implied in the volatility of the aforementioned risk ranges, what works for me isn’t adding to my mistakes; raising Cash does. And I’ll do that again this morning in the Hedgeye Asset Allocation Model.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.85-2.21%

SPX 2084-2106

RUT 1

VIX 13.03-14.79

USD 94.08-96.01

EUR/USD 1.06-1.13

Oil (WTI) 53.99-62.30

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer