Key Takeaway

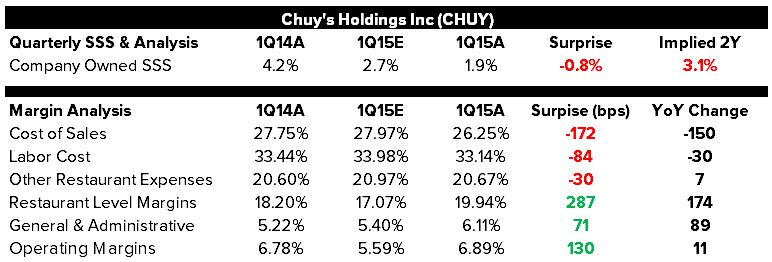

CHUY delivered a bottom line beat despite a slight top line miss in 1Q15. Comps of +1.9% fell well short of the consensus estimate of +2.7%, but management effectively managed the cost structure in order to produce earnings per share of $0.19. 2H15 guidance continues to look like a stretch. Nice opportunity to short here on the pop.

Composition of the comp. Although this was the 19th consecutive quarter of positive comps for Chuy’s, the bulk of the growth in same-store sales came from a +3.3% increase in average check (+2.8% price) and was partially offset by a -1.4% decline in traffic. As we’ve noted in the past, traffic is the true indicator of the health of a brand. It appears to us that Chuy’s is taking price in order to drive comps and margins, but at the detriment of traffic. This is a highly unsustainable trend. Management noted a -2% impact from adverse weather in Texas, Oklahoma, and parts of the Southeast. We note that TXRH, which just reported +8% same-store sales growth, said weather was not an issue in the quarter.

Credit where it’s due. We like to think we’ll always give credit where it is due and, in our view, management did a very nice job controlling costs in the quarter. While cost of sales primarily benefitted from lapping last year’s inflationary spike in dairy and produce, as well as the September 2014 and February 2015 price increases, it also benefitted from the implementation of zero based management. On the labor line, initiatives to improve labor productivity through the implementation of best practices across the system also paid dividends, with labor costs as a percentage of sales down -30 bps y/y. There were some questions on the call regarding the sustainability of this trend. As one of the analysts asked, are you “maybe pushing it a little bit too far?” We think they are and it will become abundantly clear as the year progresses.

Difficult setup in 2H15. Given the beat, management guided up full-year earnings per share from $0.74-0.77 to $0.76-0.79 while keeping same-store sales guidance flat at +2.5% (+2.8% price). Full-year food inflation is expected to come in at 0-1%, below the prior guidance of 1-2%, but is expected to accelerate sequentially. Getting to the core of short thesis here, new units continue to be a drag on same-store sales (as they enter the comp base) and margins. Non comp stores are operating at a high single digit margin in the first year and a low double digit margin in the second year. Importantly, development plans for 2015 are going to be more back-end loaded than originally anticipated, which should pressure margins despite the street’s expectations for notable margin expansion. We believe that margins in the first quarter were more an aberration than reality and think that 2H15 is setting up to be a very difficult period for the company.