KEY POINTS

- F4Q15 = CAPPED UPSIDE: There could be some top-line upside to the print since F4Q15 estimates are down 6% following the F3Q15 miss. However, we’re expecting much of that upside would come from its ancillary segments, with China Retail limited by sputtering Tmall Mix shift (commission revenue) and growing mobile user mix (advertising take-rates).

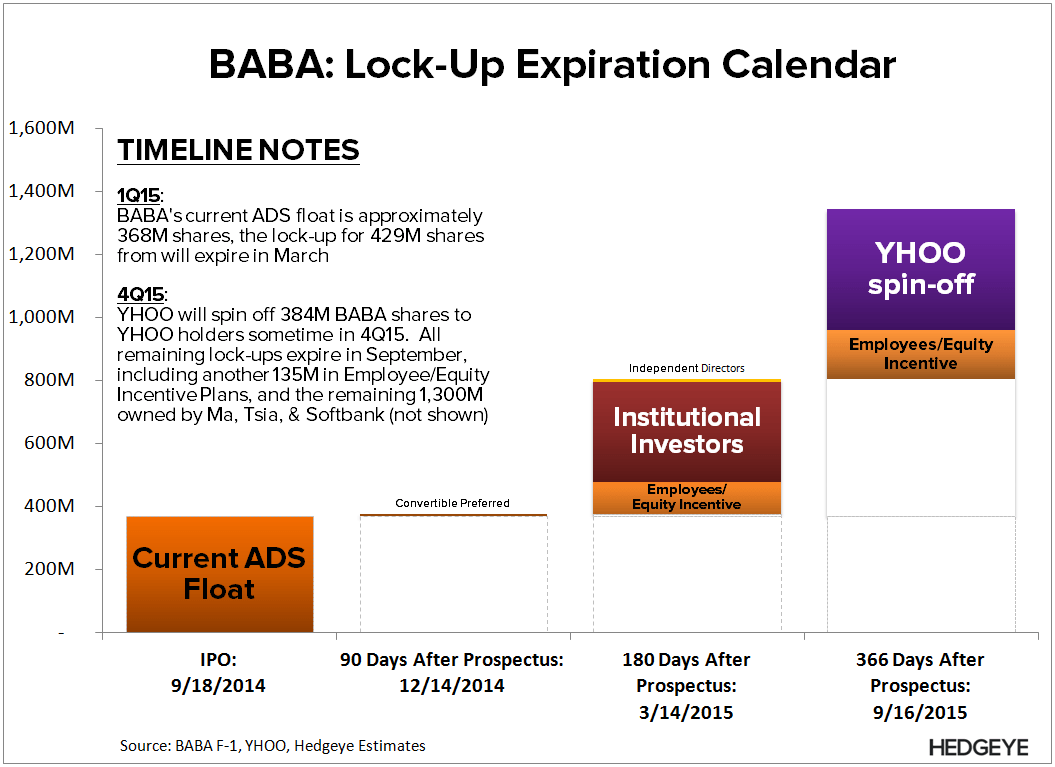

- NOT MUCH BREATHING ROOM: The setup will get progressively worse through F2016 since consensus concentrated their estimate reductions into F4Q15 and F1Q16 following the F3Q15 top-line miss. The sell-side is now expecting accelerating China Retail revenue growth from F1Q16 through F4Q16; a challenge given the secular headwinds facing the model. Further, the YHOO SpinCo will come more into focus as we move closer to year end.

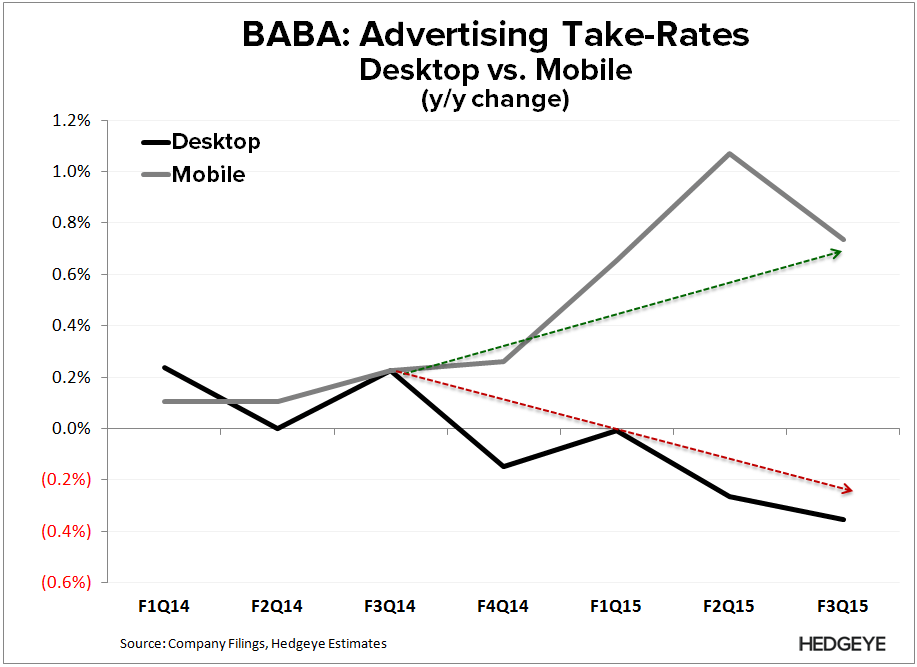

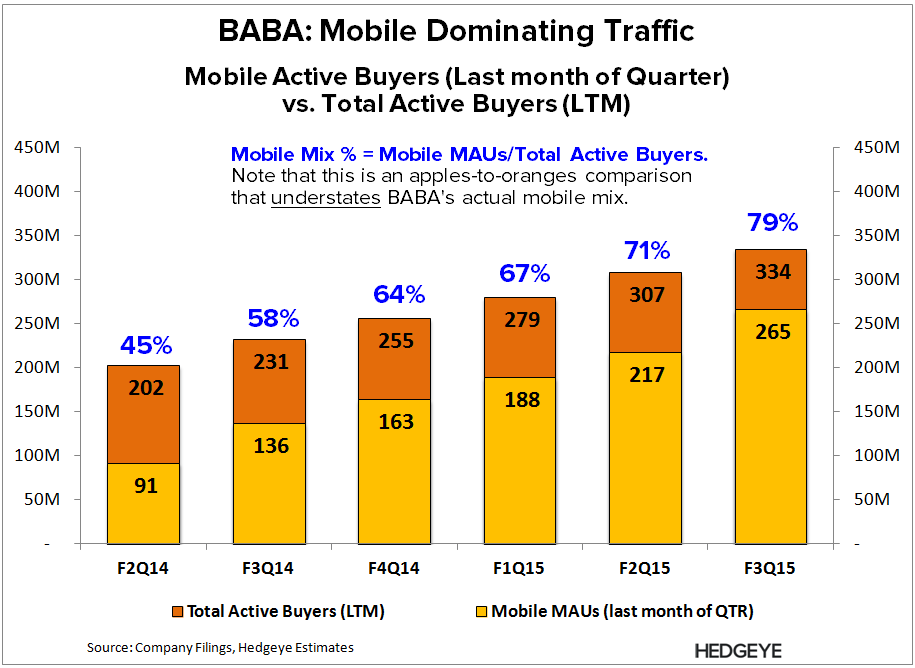

- WHAT WE’RE KEYING IN ON: Mobile take-rates, particularly on the advertising side. The bull-case suggests that mobile will approach desktop rates over time, but we suspect the opposite. We believe much of the rise in mobile monetization rates has to do with user mix shift to mobile. If that is the case, BABA may hit a ceiling on mobile advertising take-rates since mobile user mix may already be over 80%.

F4Q15 = CAPPED UPSIDE

We’re expecting a top-line beat off reduced consensus estimates following the F3Q15 miss. However, we’re expecting much of that upside would come from its ancillary segments. We’re expecting any upside to China Retail would ultimately be limited by sputtering Tmall Mix shift (commission revenue) and growing mobile user mix (take-rates). Mobile is the connecting theme.

- Vendors pay less for mobile ads: BABA runs a self-serve ad platform, so the lower price is likely the result of lower demand from what we believe to a lower-conversion/ROI product (weaker consumer).

- Tmall still nascent on mobile: BABA’s initial focus for its mobile build-out was on Tabao, where BABA doesn’t collect any commission. In turn, mobile GMV favors Tabao.

We built our Tmall tracker to gauge GMV mix percentage between the two platforms since the y/y change in Tmall GMV Mix has been the driving factor behind BABA’s surging commission revenue. The deceleration flagged by our tracker suggests commission revenue growth will decelerate sharply this quarter. Note that our tracker only focuses on desktop traffic, so this dynamic will be exacerbated by the secular rise in mobile user traffic. In turn, we’re expecting a greater percentage of ad-click volume to favor the lower-priced mobile product.

That said, any upside to China Retail will be driven by the combination of Total GMV and/or take-rates. Very small variances in either could swing the print either way, and we don’t have any real edge calling the quarter for either. But given the headwinds mentioned above, we're not expecting a strong top-line beat on the quarter.

![]()

NOT MUCH BREATHING ROOM

The setup will get progressively worse through F2016 since consensus concentrated their estimate reductions into F4Q15 and F1Q16 following the F3Q15 top-line miss. The sell-side is expecting accelerating China Retail revenue growth from F1Q16 through F4Q16 (from 30% to 42%); a challenge given the secular headwinds facing the model. Further, the YHOO SpinCo will come more into focus as we move closer to year end.

As a reminder on our thesis, we believe China’s Elite is driving the bulk of BABA’s GMV. Average spending on the platform is well in excess of what the average Chinese consumer could afford. In turn, we expect GMV/Active Buyer to decline as a progressively weaker consumer joins the platform, leading to precipitous slowdown in GMV growth, which will pressure its entire model. For more detail, see the note below

BABA: New Best Idea (Short)

02/11/15 11:12 AM EST

WHAT WE’RE KEYING IN ON

Mobile take-rates, particularly on the advertising side. The bull-case suggests that mobile will approach desktop rates over time, but we suspect the opposite.

We believe much of the rise in mobile monetization rates has to do with a growing mix of mobile users. The corresponding decline in desktop take-rates would suggest as much, especially since ~75% of BABA's marketing revenues are CPC, which require user clicks to drive revenues. If growing traffic is driving mobile take-rates, then BABA may eventually hit a a ceiling on mobile advertising take-rates (we estimate mobile is already over 80%).

BABA: The Mobile Debate

03/04/15 10:34 AM EST

Let us know If you have any questions or would like to discuss in more detail.

Hesham Shaaban, CFA

@HedgeyeInternet