This note was originally published at 8am on April 17, 2015 for Hedgeye subscribers.

“Market values are fixed only in part by balance sheets and income statements; much more by the hopes and fears of humanity; by greed, ambition, acts of God, invention, financial stress and strain, weather, discovery, fashion and numberless other causes impossible to be listed without omission.” – Gerald Loeb, The Battle for Investment Survival

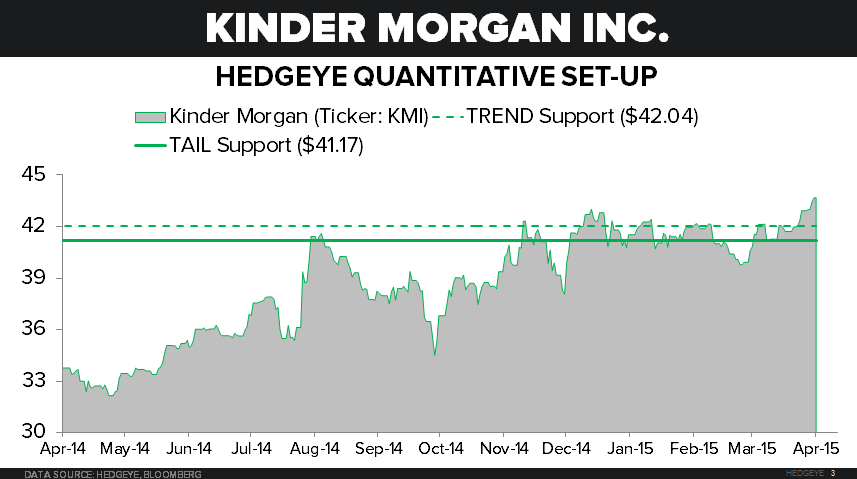

After rolling up its MLPs in December 2014, Kinder Morgan Inc. (KMI) is now the third-largest energy company in the S&P 500 by enterprise value ($137 billion) and fourth-largest by market cap ($95 billion). It’s also one of the more polarizing names out there – you either love it or you hate it.

KMI kicked off the earnings season for the energy sector on Wednesday, and with KMI being a relatively new and large name in many portfolio managers’ benchmarks, we figured that the generalists that subscribe to the Early Look would be interested in, and benefit from, our latest thoughts on KMI – the company and the stock. Regarding the former, the commentary below was sent to our Energy sector subscribers yesterday:

“In its 1Q15 report … Kinder Morgan Inc. (KMI) declared a quarterly dividend of $0.48/share, reiterated its 2015 dividend target of $2.00/share, and emphatically reiterated its long-term dividend growth guidance of 10% p.a. through 2020. KMI bulls need not read any further.

The quarter was soft overall as the more-commodity-sensitive segments of CO2 and Natural Gas Pipelines posted a combined 5% YoY decline in segment cash flow. Adjusted EBITDA came in at $1,743MM, down 1% YoY and missed the consensus estimate of $1,861MM by 6%. EBIT was $1,193MM, down 5% YoY. Pre-tax earnings were $679MM ($0.31/share), down 16% YoY. (All metrics are "before Certain Items.")

KMI incurred ~$935MM of CapEx in the quarter, $104MM (11%) of which was classified as sustaining / maintenance. It spent ~$3.2B on acquisitions, ~$3,060MM on Hiland and ~$160MM on the Vopak terminals. The Hiland acquisition closed on February 13th, so it was a significant contributor to the 1Q15 numbers.

Free Cash Flow (defined here as EBITDA – net interest expense – CapEx) was ~$295MM or $0.14/share.

Rich Kinder remarked on the call, “…our enormous footprint and our diversified set of mostly fee-based assets can produce very good results, even in times of tumultuous market conditions.”

Very good results?

EBITDA and EBIT were down YoY in 1Q15 despite $9.4B of capital invested since the start of 2014 ($5.0B of CapEx – ~$1.0B per quarter – and $4.4B of acquisitions). That’s mediocre, at best.

What is exceptional about KMI is 1) its valuation at 20x EV/EBITDA, 29x EV/EBIT, 35x P/E (pre-tax!), and a 1.3% FCF yield (all metrics are 1Q15 annualized); 2) its leverage at 6x debt/EBITDA and 9x debt/EBIT; and, of course, 3) its dividend payout ratios at +230% of net income and +150% of pre-tax income.”

---

Here’s our opinion of KMI – the company – in as succinct of a form as possible, a 140 character #tweet:

MegaCap energy conglom. Capital intensive, cyclical, competitive. Avg ROIC. Super-levered. Low organic growth. Roll up. Ponzi divi.

And all of that really isn’t that hard to see. Which of those points could you convincingly argue the other side of?

The debate and difficulty lies in what to do with KMI the stock here.

Our current view, one that is, of course, subject to change, is that it’s just one to watch from the sidelines. We apologize to the bulls for not joining the rest of the sell-side in the Rich Kinder booster club, and to the bears for not betting on the imminent collapse of the evil empire, but the risk / reward set-up does not warrant action at this time and price.

The challenge on the short side is that the higher KMI’s valuation, particularly relative to its peer group, the more “accretive” each acquisition will be. Say what you want about this growth strategy (and we suggest you re-read Buffett’s thoughts on it on pages 29 and 30 of the latest BRK letter!), but the market has bought into it and it’s going to work until it doesn’t.

Reflexivity is clearly at work; we’d consider a short position in KMI on the way down. But for now, we’re interested in playing KMI’s well-advertised acquisition ambitions via second derivatives. More on that to come…

We’ll leave it there on this battleground stock. If you own KMI, we hope that you at least know what you own!

Enjoy the weekend,

Kevin Kaiser

Managing Director