“Confusion now hath made his masterpiece!”

-William Shakespeare

Oh boy, are macro markets confused by the collision of central plans now!

Shakespeare fans will remember the aforementioned quote from Act II (Scene 3) of Macbeth. It’s a great metaphor to use in answering the question I get from most long-term risk managers: “How does this all end?”

While it would be reckless to predict precisely how it ends, I have a pretty good idea how the beginning of the end looks – confusing. Confusion in the timing of central planning breeds contempt. And that perpetuates volatility which, in due course, crushes confidence.

Back to the Global Macro Grind…

How confident are you in explaining how rates can ramp to the top-end of their respective ranges as the US Dollar goes straight down? In rate of change terms, German Bund Yields doubled in 48 hours! Irrespective of what the Fed said, did that have anything to do with the US move in rates? Big time.

Was the rates move linked to the currency and commodity move (Down Dollar = Up Oil, Energy Stocks)? I don’t think so. The FX (foreign currency) market move and Global Rates moves went in the opposite direction of what most correlation models would have predicted. #Fun? Not.

But isn’t this what we’ve all signed off on? Wasn’t central planning of markets supposed to be a “smoothing” exercise whereby all of us “smart” people could make linear-assumptions to drum up macro correlation models for all of our asset allocations and bonuses?

Let’s get real here. Macro markets just did.

Setting aside the non-linear-multi-standard-deviation-move in both German Bund Yields and the European Currency for a minute, let’s bring this discussion back to the USA and what the Federal Reserve said yesterday:

- On Growth – ‘our forecasts continue to be too high, but it’s all “transitory” because it snows in the winter time’

- On Inflation – ‘our forecasts on 2% inflation were wrong, but that’s transitory too – everything we get wrong is’

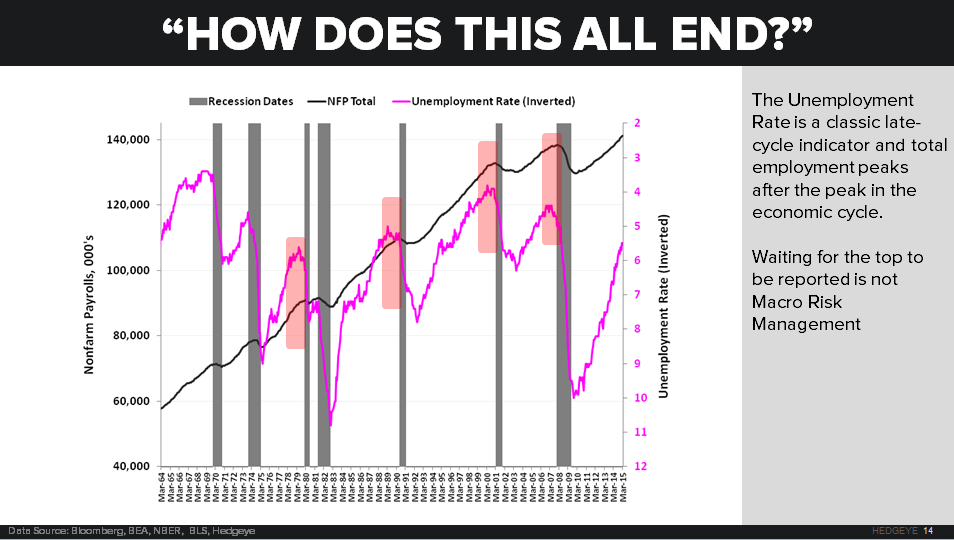

- On Timing – ‘rate liftoff is data dependent on the labor market – so run money on best #NFPGuesses’

That last point isn’t a joke (neither are paraphrasing points 1 and 2). The Fed has effectively reduced the timing of its first rate hike to the most lagging of #LateCycle economic indicators. And now you literally have to guess what the next jobs number is going to be.

Since my research team cannot predict an un-predictable number (we’ve tried to build models to front-run BLS Labor report data and, trust me, I’d have a prediction if there was a repeatable #process to be accurate with one), guessing is the only option.

Confused yet? You should be. Much like the March 18th Fed decision on “to, or not to, be lower on rates for longer” the May 8th jobs report is a binary event:

A) Jobs report “beats” useless forecasts of lagging indicator = Dollar Up, Rates Up, Oil Down (hard)

B) Jobs report “misses” useless forecasts of lagging indicator = Dollar Down, Rates Down, Oil To Infinity And Beyond

“So”, as my hedge fund friends in Chicago would say, place your bets!

Oh, did I mention that this is only a 6-7 day trading bet? Dammit this is getting good! Not only do we have to now day-trade US monetary policy based on best-guesses, but we have to completely ignore this longer-term thing called the cycle, at the same time.

What happens if the June and/or July jobs reports are bad? What happens if the May report is bad? I can tell you one thing – the entirety of Old Wall Consensus isn’t predicting anything bad – every question I get on rates has to do with ‘what if it’s good?’

There is nothing good about confusion in macro market correlations when volatility accelerates. There is no risk management #process in guessing either. So I’m selling in May and getting the heck out of the way. For now, going to cash beats confusion.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.84-2.06%

SPX 2085-2117

RUT 1

VIX 12.96-14.91

USD 95.12-97.66

EUR/USD 1.05-1.12

Oil (WTI) 52.96-59.69

Gold 1180-1215

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer