KEY POINTS

- MUCH WORSE THAN WE EXPECTED: We expected YELP to bounce off a beat and high 2Q guidance with support from inorganic tailwinds. It did the opposite. What’s worse is that YELP maintained 2015 Revenue guidance; which is not only lofty to begin with, but also means the sell-side is going to up their estimates for 2H15; ultimately increasing the hurdle.

- THE NEW MAJOR RED FLAG: We estimate that YELP’s salesforce sequentially declined this quarter. Given that the company guided to growing its salesforce by 40% in 2015, but only achieved 25% y/y growth, we believe YELP experienced a heightened level of sales rep attrition in excess of what’s implied in by the net figures. But more importantly, It doesn’t matter why this is happening, what matters is that this is an issue at all (next section).

- PULLING THE THREAD: While we expected our primary read this quarter to be salesforce productivity, we weren't expecting a decline in its salesforce itself. Remember that YELP’s business model is predicated on hiring enough sales reps to drive new account growth in excess of its rampant attrition. That said, the only thing preventing declining revenue for YELP is its growing salesforce. The fact this is even remotely an issue suggest this story is going to turn much sooner, and get much uglier, than we initially expected.

MUCH WORSE THAN WE EXPECTED

We expected YELP to beat and guide high for 2Q with support from inorganic tailwinds. It did the opposite. YELP missed both Local and Brand Advertising revenue estimates, with Other revenues surging well ahead of estimates on what was likely understated implied guidance on the Eat24 acquisition.

Delving into its Local Advertising metrics is somewhat trickier now that YELP pulled its legacy ALBA metric for its new Local Advertising Accounts (LAA) metric. The issue is that we can’t construct a sufficient time series since mgmt only provided us limited history for its new customer repeat rate metric (5 quarters). At a very minimum, there’s no denying that the majority of its attrition is coming from its core Local Advertising segment.

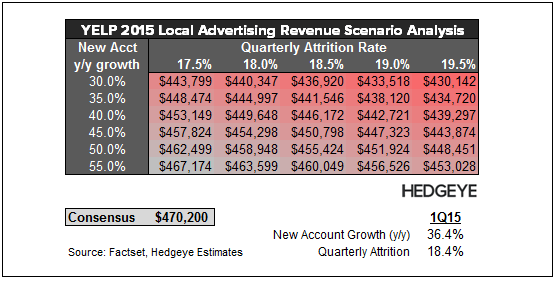

More importantly, YELP shot itself in the foot (again) by maintaining 2015 revenue guidance; which was lofty to begin with, but also means the sell-side is going to up their estimates for 2H15 since 1H15 fell short of their expectations;. See scenario analysis below for more detail.

THE NEW RED FLAG

We estimate that YELP’s salesforce sequentially declined this quarter. Given that the company guided to growing its salesforce by 40% in 2015, but only achieved 25% y/y growth, we believe YELP experienced a heightened level of sales rep attrition in excess of what’s implied by the net figures

We suspect there are two explanations behind its elevated attrition

- Too many mouths to feed: YELP's salesforce is already large enough to canvas the US in call volume. Hiring more reps just means more mouths to feed from the same trough (see note below).

- Not enough food: YELP may have switched its commission benchmark from gross to net revenue, which drastically lowers the commission pool given its rampant attrition.

But more importantly, It doesn’t matter why this is happening, what matters is that this is an issue at all (next section)

YELP: Salesforce Productivity?

03/16/15 08:10 AM EDT

Pulling the thread

While we expected our primary read this quarter to be salesforce productivity, we weren't expecting a decline in its salesforce itself. Remember that YELP’s business model is predicated on hiring enough sales reps to drive new account growth in excess of its rampant attrition.

That said, the only thing preventing declining revenue for YELP is its growing salesforce. The fact this is even remotely an issue is a major problem, especially since salesforce productivity was already on the decline to begin with. If YELP is already having difficulty sustaining its salesforce, then the story is going to turn much sooner, and get much uglier, than we initially expected.

Let us know if you have any questions, or would like to discuss in more detail.

Hesham Shaaban, CFA

@HedgeyeInternet