Fed Day Cometh… and the US Dollar Index is trading down around -1% intraday.

Position/Outlook Updates:

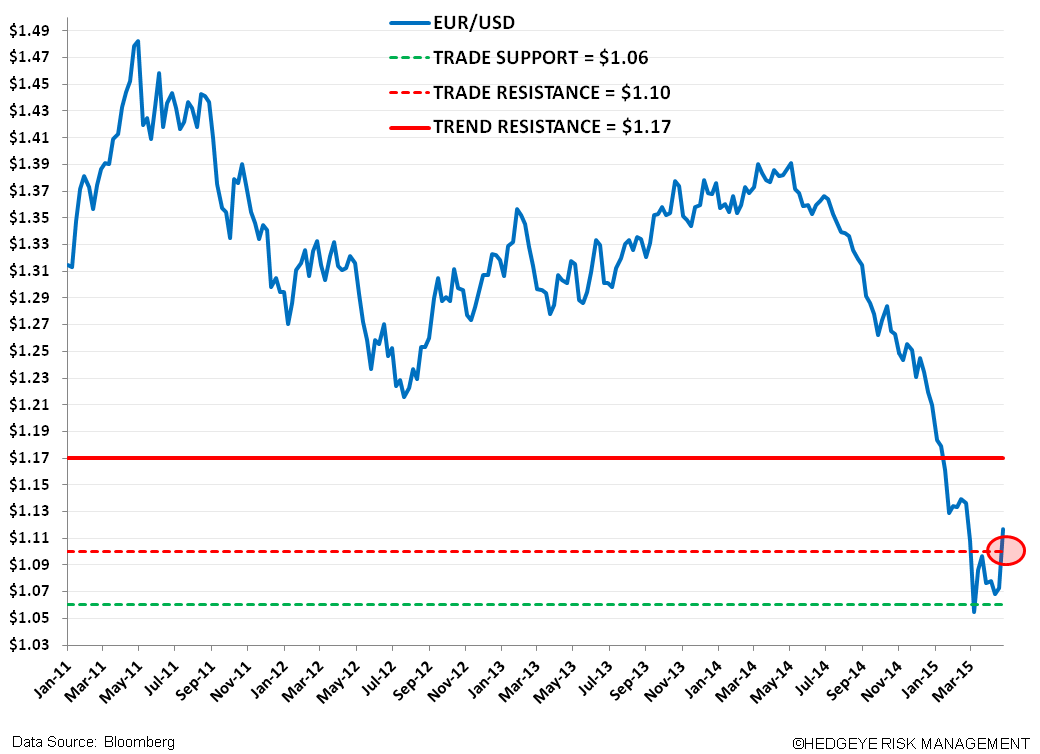

- EUR/USD – trading higher within our intermediate-term TREND bearish outlook. We shorted the cross (via FXE) today as the price collided with our immediate-term TRADE line of resistance ($1.10)

- EUR/USD – the Fed’s FOMC statement proves the Bank has a more moderate assessment of economic conditions/momentum, which could lead to further expectations of a delay in a rate hike, weakening the US Dollar from here.

- German Equities – weak in the face of a stronger EUR/USD (the DAX fell -3.2% today and is +20.3% YTD); we remain bullish on an intermediate-term TREND duration as Draghi’s foot remains on the QE pedal.

- German Equities – while not necessarily “trading” on fundamentals, recent data is mixed, with German CPI jumping 10bps to 0.3% in APR Y/Y while last week’s release of German PMI Manufacturing and Services figures fell for the first time this year (APR reading).

Shorting FXE

TRADE: Today Keith recommended shorting the EUR/USD (via the etf FXE) at $109.13. He wrote: “There are plenty of macro positions pushing to the top/bottom ends of their immediate-term ranges right now. My strategy during these counter-TREND moves is to wait/watch for the bullish/bearish TRADE to tap the top/bottom end of the range - sometimes it takes time.

I've been waiting for the Euro (vs. USD) to do that for a few weeks now, and this is my 1st SELL signal. There's no immediate-term TRADE support in the EUR/USD cross to $1.06.”

Additionally, we believe the US Dollar has been pushed to 2 month lows as investors expect the Federal Reserve’s more moderate assessment of economic conditions/momentum will push the dots (again) on a rate hike. A worse than expected US Q1 GDP and inflation report could drag the USD lower over the immediate term.

TREND/TAIL: Longer-term bearish: we continue to think a whole host of reasons will drag the common currency lower, including:

- ECB President Mario Draghi’s willingness to do “whatever it takes”, including a QE package that may win him the ‘Currency Wars’ over the USD

- There’s no end in sight for an exit of the Eurozone’s weaker countries, and in particular Greece’s debt hang will play out in multiples of years, not months

- A monetary policy across uneven economies will be highly conflicting

- Cultural differences that will limit cross-border labor movement

- Bearish demographics

Bullish German Equities

The German equity market (DAX) had a significant -3.2% pullback today. We continue with the stance that the Eurozone’s equity markets do not like a strong euro.

The DAX is up 20.3% YTD, and we continue to think that over the TREND/TAIL it will pay to obey the commands of the central planners, in particular by being long of German equities.

To reiterate our TREND thesis:

- QE is only just beginning; the euro will continue to weaken; Germany will disproportionately benefit due to exports; and asset classes like equities will inflate due to money creation

- The German economy sits in the sweet spot to benefit from a weaker euro as its exports account for a monster 47% of German GDP

- Since the ECB announced QE on 1/22/15 the correlation between the DAX and EUR/USD is -0.84, a strong inverse relationship that we expect to persist as the ECB keeps its foot on the QE pedal for longer than its intended target (late 2016)

- Recommending long the DAX (HEWG or EWG) and short EUR/USD (FXE)

If you missed our call titled “Germany: Still Bullish” on 4/14, CLICK HERE for a 30 minute video replay that walks through 40 slides of supporting material.

While German Equities are not necessarily “trading” on fundamentals, recent data is mixed. A couple notable call-outs include:

- German CPI jumping 10bps to 0.3% in APR Y/Y

- German PMI Manufacturing and Services figures fell for the first time this year (APR reading), in-line with the Eurozone average

From a quantitative perspective, the DAX recently broke its immediate-term TRADE line of support (to become resistance), but remains firmly above its intermediate-term TREND and long-term TAIL levels, a bullish signal.