“Our greatest power is that we know that we don’t know.”

-Ray Dalio

Do you really know what the Federal Reserve is going to say today? I don’t. If you do, with 100% certainty, please don’t call and/or email me with that information. I don’t want to go to jail.

Having witnessed some characters in this business take on orange-jump-suit-risk to get what some of them call “edge” (i.e. inside information), I’ve spent my entire career trying to build a #process that doesn’t need short-cuts (i.e. cheating).

That puts me in a position of really not knowing what I’m not supposed to know. Instead of selling you certainty, it forces me to embrace uncertainty… and probability weight each and every decision I make based on the most recent data and market pricing.

Back to the Global Macro Grind…

We had our company meeting yesterday. We do one every quarter. It’s usually lunch and 3-4 hours of thought leaders at Hedgeye thinking out loud about #process: what’s working; what’s not – what can we do next. #BestPractices

The best part about these meetings is the element of surprise. When you have 57 thoughtful people in a room who have decided to open their minds to learning, a lot can happen in an afternoon. Who can really make you challenge yourself and think?

Our veterans (Daryl Jones, Howard Penney, and Tom Tobin) stepped up and delivered the wood on that front yesterday. In fact, I don’t think I’ve ever seen objective and critical self-reflection like that – back to back to back.

You can call us a cult. But we call ourselves a team.

During yesterday’s meeting, circa 3:15PM, one of our analysts slammed his laptop and left the room in a frenzy. This had nothing to do with Penney telling Hesham Shaaban to “embrace meditation” – one of his Best Short Ideas, Twitter (TWTR) was blowing up!

Fat finger on the pre-market close release. Stock down 18% in a New York minute. Halted. #Boom!

And the Hedgeyes smiled.

There’s something about building an independent think tank that prides itself in SELL ideas that gets me up in the morning. As most of you know, building a repeatable #process on the short side is not an easy thing to do. That’s why we’re doing it.

At one point in the QA session of the meeting, I was asked what our “pipeline of prospective analyst hires” was looking like. And, for the first time, instead of rattling off names of people we’re interviewing, I said I just wanted to see more of our rookies play.

Not only do the “young” guys/gals at this firm get how to not be certain about anything, they know how to build a battle-tested #process that allows them to probability weight both the accuracy and timing of their research ideas.

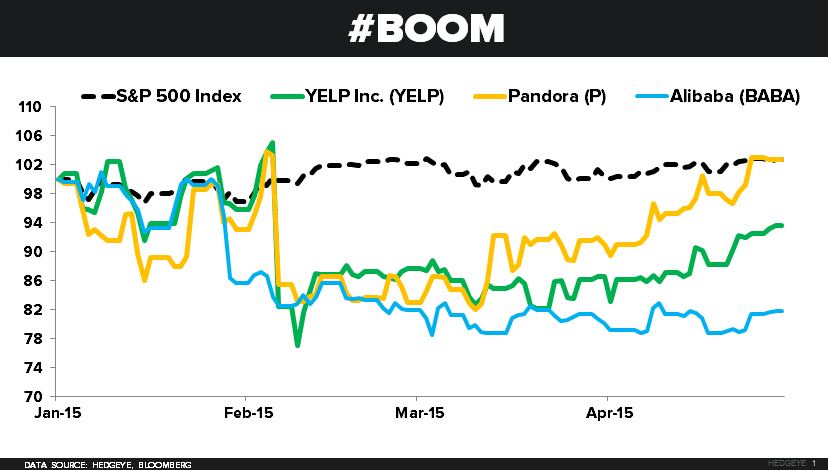

While you can criticize Shaaban for literally never having presented a Best Long Idea (yet), he’s nailed the following names to the proverbial NHL playoff boards in the last 18 months (i.e. since we let him start publishing on his own names):

- Weight Watchers (WTW)

- eHealth (EHTH)

- Pandora (P)

- Yelp! (YELP)

- Alibaba (BABA)

In other words, what he really needs next is to get run-over in one of these things. Because no analyst I have ever worked with stays this good (on the short side) for this long, in an up market!

I obviously don’t want the man to get crushed. But reality is that everyone gets tagged in this business, eventually – and that’s how we all learn. But if you listen to Shaaban talk through his ideas, he’s constantly talking about not only what he doesn’t know… but what the management teams he follows don’t know either.

And that, my friends, is how you get really good at this game.

That’s how you beat the guys who take the short-cuts, cheat, and have no other process than asking “management” what the numbers are. When management doesn’t know what they don’t know – the fundamentally driven research analyst who thinks for himself wins.

As for what macro “management” (The Fed) really knows… Cyclically, do they get that the US is #LateCycle? Secularly, do they get global demand is slowing due to #DemographicYields? We’ll see.

Our immediate-term Global Macro Risk Ranges (with intermediate-term TREND views in brackets) are now:

UST 10yr Yield 1.85-2.02% (bearish)

SPX 2095-2126 (bullish)

RUT 1 (bullish)

DAX 118 (bullish)

VIX 11.89-14.82 (neutral)

USD 95.63-97.83 (bullish)

EUR/USD 1.06-1.10 (bearish)

YEN 118.55-120.81 (bearish)

Oil (WTI) 52.61-58.30 (bearish)

Natural Gas 2.44-2.62 (bearish)

Gold 1181-1215 (neutral)

Copper 2.65-2.83 (bearish)

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer