It’s a good thing $80-90 Trillion in QE is working right? In case you missed it, Japan reported a stink bomb of a Retail Sales report last night. Japanese Retail Sales fell -9.7% year-over-year in March versus down -1.7% in February.

Splendid.

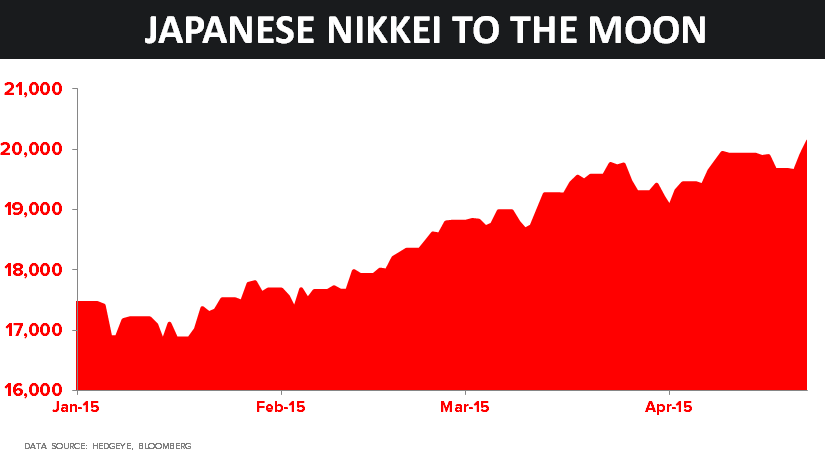

What did the Weimar Nikkei do on the news? It went up, of course! The Nikkei is up +0.4% to +15.6% year-to-date pre the BOJ meeting.

As I wrote in today’s Morning Newsletter:

As long as stock markets around the world continue to hit all-time highs, the central planners will look wholly innocent to many who think equity gains reflect economic growth. All the while, they’ll look wholly guilty to those analyzing the economic data.

Stay tuned—this Gong Show is going to get really interesting.