“The hero of a tragedy, in order to interest us, should neither be wholly guilty nor wholly innocent.”

-Napoleon

That’s the opening volley from a brick of a recently published #history book (926 pages) that has been staring me in the face for months – Napoleon – A Life, by Andrew Roberts.

Research truths tend to be revealed with time. And since there’s never been a definitive history of the Corsican formerly known as “Napoleone de Buonaparte”, this one is getting what I love in a good read – polarizing reviews.

In many ways, this makes me think about the short history of QE (Quantitative Easing). Ben Bernanke has been quick to try to shape his own version of the story. And while I think he’s suspect in doing so, only time will tell who the real heroes are.

Back to the Global Macro Grind…

As long as stock markets around the world continue to hit all-time highs, the central planners will look wholly innocent to many who think equity gains reflect economic growth. All the while, they’ll look wholly guilty to those analyzing the economic data.

While the Japanese and Chinese stock markets are more obvious examples of the divergence between economic reality and stock “charts”, it will be interesting to observe how the American and European narratives change alongside market prices.

Last night Japan reported a bomb of a Retail Sales report at -9.7% year-over-year for the month of March. That compared to a paltry -1.7% in the month prior. And the Japanese stock market went up on that…

In other news:

- US Stocks stopped going up at their all-time highs yesterday post a weaker US Services PMI report

- Services PMI (Markit report) for APR slowed to 57.8 vs. 59.2 in MAR

- This begged me the question – are US consumption gains from “lower gas prices” slowing?

Contrary to however people who don’t understand our process, models, or investment conclusions think, we’ve actually been The Bulls on the US domestic consumption and #Housing economy for the last 4-6 months.

Some of our conclusions were born out of the following macro stimulus:

- #StrongDollar as a net benefit to the purchasing power of Americans

- #Deflation in commodities, gas prices, cost of living, etc.

- #Lower-For-Longer on interest rates = #HousingAccelerating

We’ve argued this is why:

- Housing, Consumer Discretionary, Healthcare, and Consumer Tech stocks have outperformed YTD

- Financials and Industrials (companies negatively affected by lower rates and #deflation) haven’t performed YTD

So why on earth would an easier Fed that:

A) Weakens the Dollar and …

B) Re-flates commodities prices and cost of living

… be good for real US consumption growth?

You’re right. It wouldn’t be. But it might be really good for Oil & Gas and Mining stocks!

This puts both the internal message of macro markets (stocks, bonds, commodities, FX, etc.) and US economic reality at odds with one another again. We’ve seen this movie before.

We’re seeing it in Europe and Asia every trading day. Mainstream economists and strategists are constantly being pulled towards a narrative of stock market gains being congruent with economic growth and inflation expectations.

Just to hold them to account - what if the 2H 2015 growth bulls are right, and a #DevaluedDollar + #RisingOilPrices is bullish for US economic growth? Shouldn’t interest rates be raised earlier then too? Then what happens to Housing and Biotech stocks?

Alongside some 2015 US equity bears capitulating to the upside yesterday (after getting bearish in January, covering your shorts at the all-time high isn’t a good #timestamp), Mr. Macro Market delivered that very message for us all to consider:

- Biotech (IBB) -4.2%, on the day!

- Housing (ITB) -1.3%

- Silver and Gold +4.5% and +2.4%, respectively

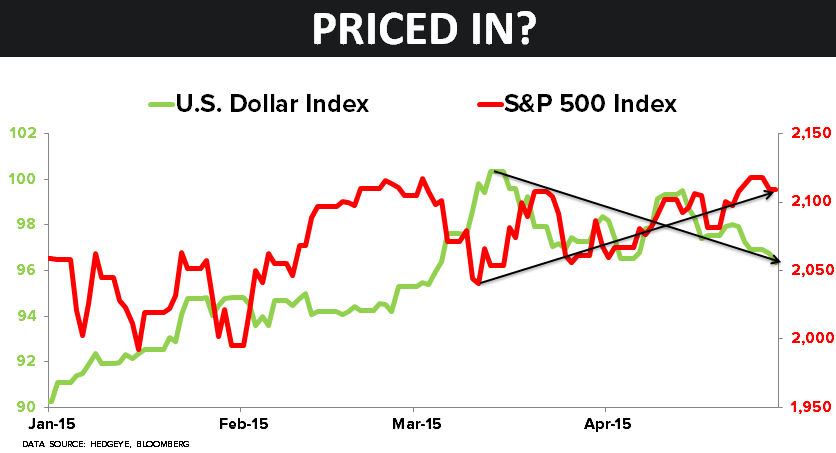

This had me asking myself if what’s been a solid run being long stocks into the Fed meeting has all been priced in? I hope it hasn’t been. But that’s not a risk management process inasmuch as the QE fans aren’t my economic #history heroes.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.86-1.99%

SPX 2093-2124

RUT 1

Nikkei 198

VIX 12.02-14.91

USD 96.45-97.85

EUR/USD 1.06-1.09

WTI Oil 52.35-58.16

Gold 1175-1208

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer