No Edge On The Quarter

This was likely a tough winter for Panera, considering its exposure to the Northeast, but same-store sales estimates of +2.2% seem to reflect this as they lag Black Box industry same-store sales of +3.0%. While we believe initiatives are driving a sales and traffic lift, incremental costs associated with these initiatives are increasing and we, along with the rest of the street, don’t have the greatest clarity around the potential impact of this.

Buy It On Down Days

While limited visibility kept us away from the long side for most of 2015, the announcement of several initiatives a week and a half ago tell us that Mr. Shaich is serious about righting the ship. While visibility is still somewhat limited, we see an asymmetric setup to the upside here. Estimates have come down 6% and 12% over the past three and six months, respectively, and the stock has underperformed the XLY to a large extent over the past three years. Importantly, management has a feasible opportunity to reverse this trend. This is a stock you need to buy on down days.

Management Commentary Is Paramount

While the recently announced initiatives are certainly a good starting point, they’re far from the endgame here. Levering up, refranchising, and buying back shares should support the stock over the intermediate-term as management works to operationally fix the business, but we see opportunity to go significantly above and beyond this. This is the first time management will address the investment community in a public forum since this announcement and additional commentary will be paramount. We laid out the activist playbook on a Flash Call immediately following this news, but don’t know to what degree management will be receptive of our suggestions. We believe there’s a significant opportunity to enhance Panera 2.0 (or create Panera 3.0), slow unit growth, aggressively refranchise stores, reduce capital spending, cut excess G&A, and sell off non-core assets such as the distribution business. We hope to hear about recent developments on any of these fronts on the call tomorrow.

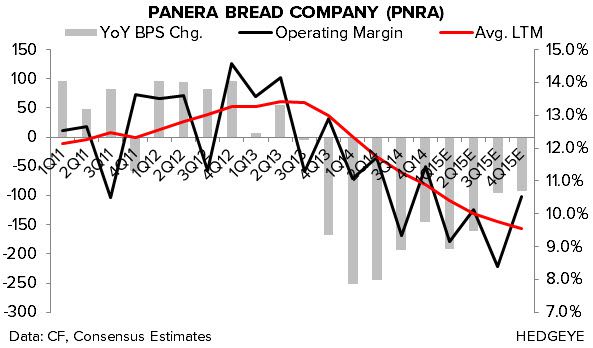

Breaking Down 1Q15 Estimates

Same-Store Sales: The street is looking for 1Q15 EPS of $1.43 (-7.5% YoY) on sales of $659.1 million (+8.9% YoY). The system-wide comp outlook (+2.2%) represents a 90 bps sequential slowdown in the two-year average.

Cost of Sales, Labor Costs, Other Restaurant Expenses, and Restaurant Level Margins: The street expects cost of sales as a percentage of revenues to increase 26 bps YoY. We suspect PNRA could deliver a slight “beat” on this line considering the rather benign food inflation the industry is seeing to-date. At this time last year, Panera had 80% of commodity needs locked. Labor costs and other restaurant expenses as a percentage of revenues are expected to increase 132 bps and 5 bps YoY, respectively. We are in-line with these estimates. This would imply restaurant level margins of 16.87%, down 164 bps YoY. We could see a little bit of upside to this line depending on how cost of sales shake out. We note that this line has been a source of upside for multiple companies (CAKE, CMG) that have already announced 1Q15 results.

G&A Expenses and Operating Margins:

G&A as a percentage of revenues is expected to increase 13 bps YoY to 5.91%. We have little clarity on this line given the timing of certain initiatives, but wouldn’t be surprised if it proved to be conservative. Operating margins are expected to decrease 192 bps to 9.15%.

Sentiment and Valuation

With a $177 average target price and only 37% buy ratings, the sell-side community remains rather cautious on the name. Short interest comprises 10.9% of the float. At only 12.1x EV/EBITDA (NTM), Panera trades at a significant discount to the majority of its quick-service peers. An accelerated transition to an asset light model should result in immediate multiple expansion.