(note: delayed because of an earnings season bout of stomach flu.)

Overview

The mining downturn showed CAT’s executives the importance of managing Street expectations. CAT stands a good shot of earning between $4.50 and $5.25 this year, and those odds increased with 1Q15 results. Estimates for 2016 EPS are now slightly below those for 2015, even with an aggressive buyback program. Despite an achievable bar, management commentary was decidedly downbeat. The delusional optimism is now gone. Bummer. Comments like this were more fun:

“That’s the reason back in 2010 we said that we were going to invest heavily in mining, and yes we did, in terms of our acquisitions and our R&D and our capital we invested over $15 billion and everybody will see over the long term that that was an outstanding investment.” – Steve Wunning 3/4/14

We have three takeaways from the quarter:

- Cat Financial Showing Cracks? Cat Financial had performance issues in its Latin American and Mining portfolios. Mining and Oil & Gas credit trouble is our next potential downside catalyst. Remarketing equipment would be no picnic in either industry. For background on our concerns, see here, and we expect to have more detail on Cat Financial in the next couple of weeks.

- Implied Orders Weak, But Biased by Cancellations: End-market demand was much weaker than either reported sales or full year revenue estimates. However, book-to-bill type metrics may be artificially depressed due to oil & gas order cancellations.

- CI, E&T Margins Quite Good: CAT performed well with what it had, and that, along with a low 2Q15 bar, may keep us sidelined for now. We had anticipated placing short CAT back on our Best Ideas List, after having removed following a weak 4Q14 earnings report in January.

Frustrating Set-up, Waiting Until Closer to 2Q 2015: CAT may be able to meet or beat 2Q15 estimates, and again inch guidance higher. We would guess that management didn’t raise guidance by the full beat because they wanted to keep expectations low heading into a far weaker 2H 2015 environment. We’d also bet that the company’s “actual” internal forecast has them crushing their “publically discussed” internal forecast. We have been expecting to re-enter a CAT short view, as discussed in our 1Q15 earnings preview note, but will now likely wait until either just before or just after 2Q15 results.

CAT Not Out of the Woods

Cat Financial Showing First Cracks: CAT noted that “At the end of the first quarter of 2015, past dues were 3.08 percent, compared with 2.17 percent at the end of 2014. The increase in past dues compared to year-end 2014 was primarily due to the performance of the Latin American and Mining portfolios and seasonality impacts.” We think this might be the next key downside catalyst for Caterpillar, and one that could represent ‘the bottom’ – that, or perhaps a management change. We will have more to say about Caterpillar Financial in coming weeks. .

Implied Orders Below Revenue, Estimates: The mining downturn is now better appreciated, including expectations for price competition and negative RI operating margins. CAT’s exposure to Oil & Gas is also well recognized now, even though it won’t really hit results until 2H 2015. Still, if we look at the end-market order rates implied by quarterly sales, adjusted for backlog and dealer inventory changes, CAT reported a book-to-bill like metric well below 1.00 (~0.86 in 1Q 2015 vs. ~0.98 in 1Q 2014). Does this suggest downside risk to revenue in the longer-term? Maybe, but we would bet that cancellations had a non-recurring and disproportionate impact.

Segments

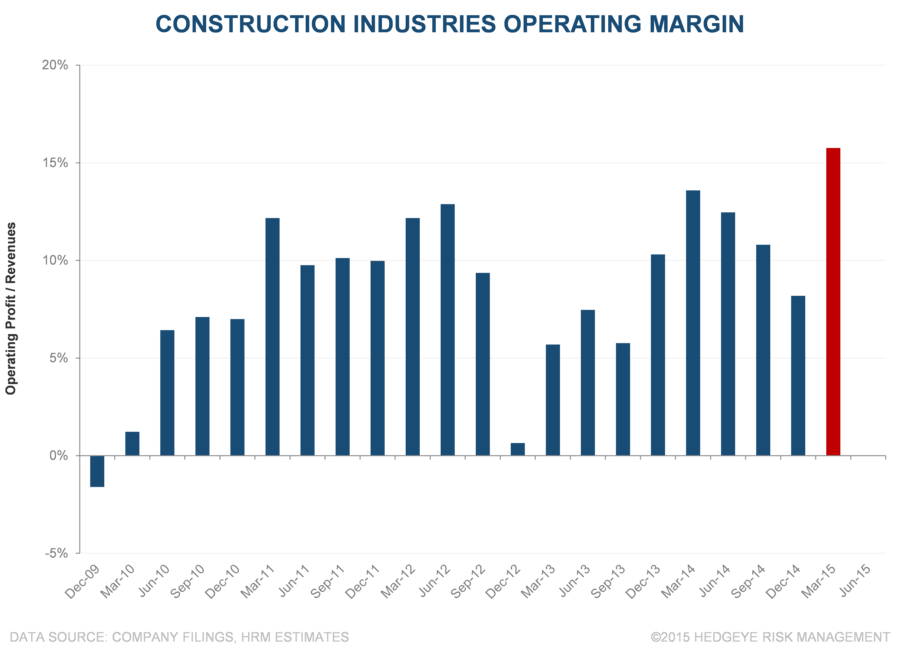

Construction Industries (CI): CI benefitted from a larger inventory build at the dealer level than the company has seen in recent years, but only about $100-$200 million more than last year by our rough estimates. Pricing and currency were also benefits. Regardless, it is hard to spin 220bps of margin improvement on a 7% revenue decline as some sort of negative. Of course, we expect margins to decline during next three quarters of 2015, much as they did last year following strong 1Q results and dealer inventory builds.

Energy & Transportation: E&T should run through its high margin, at risk oil and gas backlog by the end of 2Q15, and back half 2015 margins should suffer as a result. Still, an operating margin in the 15%-16% seems reasonable in 2H. We suspect, although the company has not indicated as much, that deposits for cancelled orders may have boosted results somewhat. Also, close in orders (inside 90 days, or so) are typically unable to be cancelled. Those two factors suggest margin slippage in 2Q 2015, ahead of the 2H 2016 profitability stepdown.

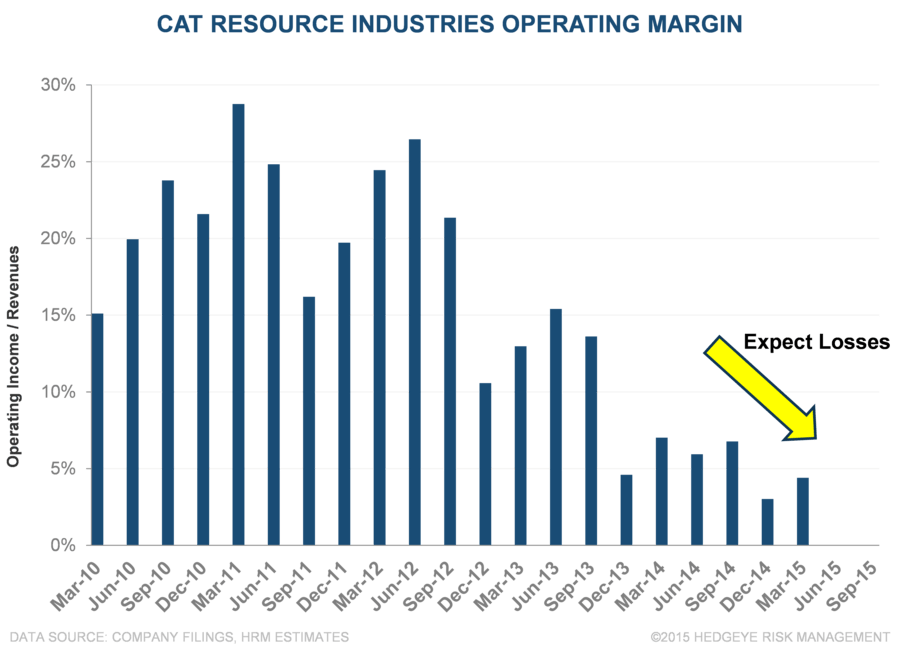

Resource Industries: Earnings call commentary indicated that segment operating losses would like;y come later this year. The industry is capital intensive industry and has excess capacity, and we have been expecting price competition to heat up.

Upshot

We learned last year, quite painfully, to be careful of CAT management’s plans to guide low and ratchet expectations higher. With 2015 and 2016 estimates already fairly low, we need to build our case for meaningful credit losses at Cat Financial. We will stay on the sidelines until we get closer to the 2Q 2015 results, which could again provide CAT with the scope to nudge guidance higher.