"It’s like Speed 2 but with a bus instead of a boat.”

-Milhouse Van Houten, The Simpsons (season 12)

Progress is generally not a cosmological crapshoot; some mystical coming together of elements, which, through some random spontaneity, have come to form a specific, organized end.

Black swans and accidental billionaires are real but success, by and large, is not an accident.

Progress and change can, at times, be illusory however.

You know those “Before” and “After” photos that grace the pages of pretty much every fitness and nutritional supplement ad you’ve ever seen? I took part in one of those photo shoots one year following a natural bodybuilding show I did.

The best part...

I did both the “BEFORE” and “AFTER” photo in the same day. No twelve-week transformation, no sophisticated supplement cocktail, no sycophantic testimonial ...mostly make-up, lighting artistry and photo editing acrobatics. Yep, the venerable before & after shot – that paragon of fitness marketing – can be (not always) the simple product of illusion and marketing malfeasance.

Back to the Global Macro Grind…

It’s been a tough last couple days for housing bulls with price volatility rising and performance whipsawing alongside company earnings and data seasonality. However, similar to my illusional instantaneous physique transformation, the ‘Before’ and ‘After’ of Housing’s underlying fundamental reality is largely unchanged.

Let’s review and contextualize the crush of recent data, starting with the (perceived) negatives.

DHI: D.R. Horton beat top and bottom line estimates for fiscal 2Q on Wednesday, reporting 30% growth in orders, strong selling season demand and a rising backlog while raising full year sales and construction estimates. The stock, however, closed down -5.4% on the day as management pared back its gross margin forecast by -50bps on account of the rising contribution from and increased focus on the lower-margin, entry level market (i.e. 1st time homebuyers).

So, investors remain acutely focused on builder margins - a preoccupation and movie we’ve seen before with KBH reporting a similar quarter, with a similar investor response, at the start of the year. To tie in today’s amusing but otherwise irrelevant headline quote - it’s like January but with DHI instead of KBH.

The bullish rejoinder to the margin concerns is two-fold:

- It’s our view that the recent margin weakness is largely a product of the marked deceleration in HPI (Home Prices) that occurred over the course of 2014. In other words, it’s a product of rearview dynamics. With home price growth stabilized and now beginning to accelerate over 2015 the forward outlook for margins is improving.

- DHI is making a calculated bet that 1st time homebuyer demand is poised to accelerate meaningfully and the market disagree’s with the conclusion and/or the operating decision. DHI’s own results are testament to the improving trends in entry level demand. With employment growth for the 20-34 year old group now positive for 2-years and accelerating over the last couple quarters the labor market dynamics are supportive of that expectation as well. Further, the FHA loan cost reductions and low downpayment loan programs rolled out by Fannie/Freddie in January are all aimed at bolstering entry-level demand.

We understand the margin consternation but, from a top-down perspective, it’s difficult to characterize accelerating demand as a negative fundamental development, particularly with a view that HPI should support margin improvement going forward. This is why we've been recommending buying the dips on builders - such as KBH when it traded down to $11 (24% lower from yesterday’s closing price) back in January - that sell off on margin concerns.

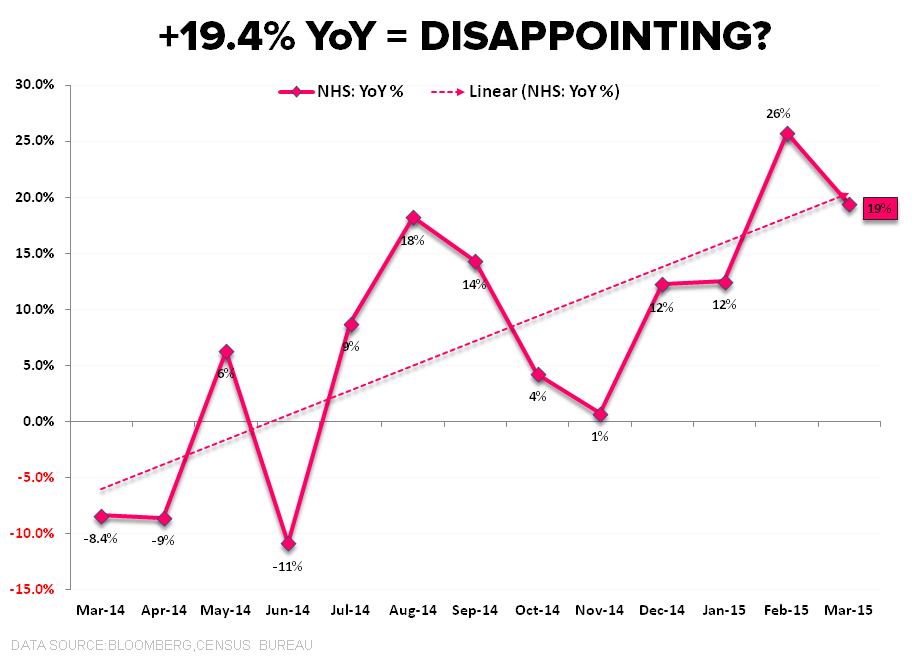

New Home Sales: New Home Sales for March, reported yesterday, declined -11.4% MoM to +481K. The sequential retreat was notable and captured most of the headlines but was, in fact, not overly surprising and deserves proper contextualization. New Home Sales in February were the highest since February 2008 and some 22% above the TTM average so a modest hangover on the heels of that comp should not be unexpected

Further, as we show in the Chart of the Day below, given the favorable comp dynamics, New Home Sales in March – despite the sequential softness – were still up a remarkable +19.4% YoY. Moreover, with comparison’s remaining favorable through July, year-over-year sales growth is likely to come in in the upper-teens to mid-twenties over the next four months - one would be hard pressed to find a better, rate-of-change chart in all of Global Macro.

So, DHI’s earnings were disappointing and New Homes Sales in March were soft…but not really. Moving onto this week’s discretely positive housing data….

Purchase Applications: Purchase demand, as measured by the MBA’s weekly survey, rose +5.0% week-over-week to 205.4 on the Index – the highest level since June of 2013. On a year-over-year basis, purchase demand accelerated to +15.4% - the fastest rate of growth YTD and the 15th consecutive week of positive growth. Purchase activity in 2Q15 is currently tracking +13% QoQ and +12% YoY.

Existing Home Sales: Existing Home Sales rose +6.1% MoM in March to 5.19M Units SAAR – marking the highest level in 18-months. On a year-over-year basis, EHS accelerated to +10.4% YoY as the confluence of easy comps, improving organic demand and weather related catch-up all supported the rebound in reported demand. That same constellation of factors should continue to support strong 2nd derivative improvement in demand over the next couple/few months.

FHFA HPI: the FHFA Home Price series for February released this morning showed home price growth accelerating to +5.5% YoY (vs. +5.1% prior), further corroborating the acceleration reported by the CoreLogic series earlier this month. Tight supply should continue to support home price growth and given the strong relationship between housing related equities and 2nd derivative HPI, the existent demand/supply/price dynamics should support performance across the complex.

We turned positive on Housing back in November but having been on both the long and short side of housing multiple times since 2008 as our model is both data sensitive and dynamic.

Looking forward, there are a trinity of known risks to housing activity whose likely magnitude of impact remains largely unknown. Specifically, the convergence of negative seasonal performance, new regulation (TRID) and the impacts of the California/West Coast drought pose a collective risk to housing activity into late 2Q/early 3Q.

However, while we remain mindful of those quasi-latent risks, we continue to think improving fundamentals and accelerating rates of change in both demand and price should dominate investor mindshare and related equity performance in the more immediate-term.

Enjoy your weekend.

Christian B. Drake

U.S. Macro Analyst