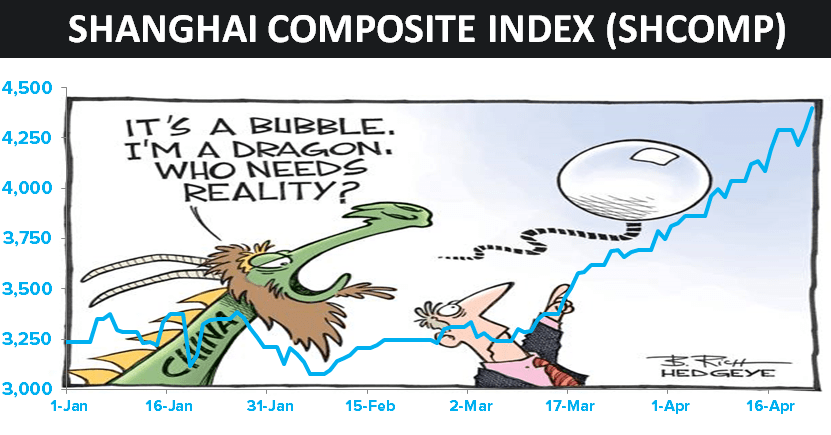

The Shanghai Composite? It is up another +2.4% this morning to +36% year-to-date (a new high). My, oh my… And, get this, China is up +92% since growth and inflation really started to slow in October of 2014!

Meanwhile, observe the *Record* weekly gain in Chinese stock brokerage accounts opened this week. 3,250,000 accounts were opened (per Sina.com.)

No issues here. This will all end really well. Move along.

Editor's Note: This is an excerpt from Hedgeye morning research today. Click here for more information and how you can become a subscriber.