Pain Trade is the one that the largest % of market participants are not positioned for.

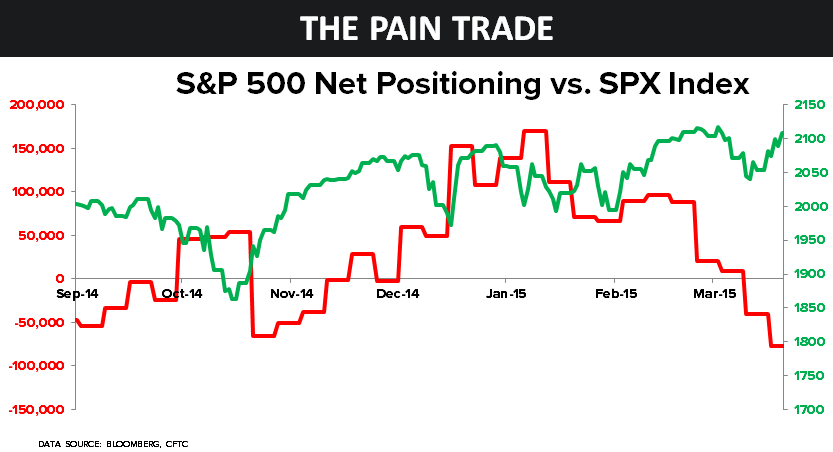

One very important way to listen to where the crowd is positioned is in futures and options contract terms. Before yesterday’s (and this morning’s pre-market futures) ramp, here’s where non-Commercial CFTC futures/options NET positioning stood:

- SP500 (Index + Emini) net SHORT position of -40,978

- The 3 month avg net position = +13,092 (net LONG)

- The 6 month avg net position = +31,930 (net LONG)

Click to enlarge.