Source: RCL

CONF CALL

- Anthem of the Seas has been 'quite profitable and generating strong returns'

- Quantum of the Seas bookings in China has been 'heartwarming'

- Double-Double program still on track

- Hedgeye is skeptical

- China now represents 6% of capacity at a higher level % of the company's profitability

- Bookings curve moved forward since they marketed sailings earlier than usual; thus, less need to offer late-minute discounts

- In March, adopted new policy that they will not offer late-minute discounting in North America (excluding 2-4 night itineraries). This may negatively impact short-term bookings but believe this is the right method over the long-term.

- Strength in close-in pricing in Caribbean boosted Q1. Caribbean capacity had 69%.

- Quantum had significantly higher premiums vs rest of fleet

- At this point, Booking and APDs are higher vs same time last year

- Previous guidance already incorporated better Caribbean pricing in Q2-Q4

- Continue to expect low single digit yield increase in Caribbiean sailing

- Europe: volumes slightly down vs 2014. Capacity up 5% YoY. Strength coming down Baltic/Med doing well. Eastern Med are soft, particularly Turkey. Still see mid-single digit yield increase in 2015.

- Asia: in 2015, capacity accounts for 15%. Asia itineraries, as a whole, has been trending well but individual itinerary's performance vary. Quantum is booked 80% for the summer 2015. 2016 is looking good as well.

- We agree. As we wrote in "RCL: HOT ASIA BOOKINGS", Quantum bookings have been stellar. But pricing performance is mixed particularly with the older fleet underperforming in non-China itineraries.

- Expect low to mid single digit yield increase.

- Lower Fuel consumption due to better fuel initiatives.

- 2Q 2015: capacity mix: 37% Caribbean, 25% Europe, 10% Alaska, 10% China

Q & A

- China: 66% more capacity in China this year. Good yield growth but not double digit growth this time around.

- Southeast Asia: yields are flattish.

- Australia: yields are up slightly

- Consumer pay bundled packages in non-US$

- Onboard rev will still have a record year

- 150bps change from Q2 -Q4 ; half of it on anticipation of weaker non-US onboard spend. Another half of it is on Eastern Med and new NA pricing pricing policy mentioned above

- Is new NA pricing policy shared by their competitors? They don't think so.

- Repositioning is great for Quantum but lower yields for everyone else who has repositioned.

- We've been concerned about the underperformance of the pre-2006 fleet.

- Why NCC ex fuel much higher in 2Q? mostly due to Quantum repositioning to China

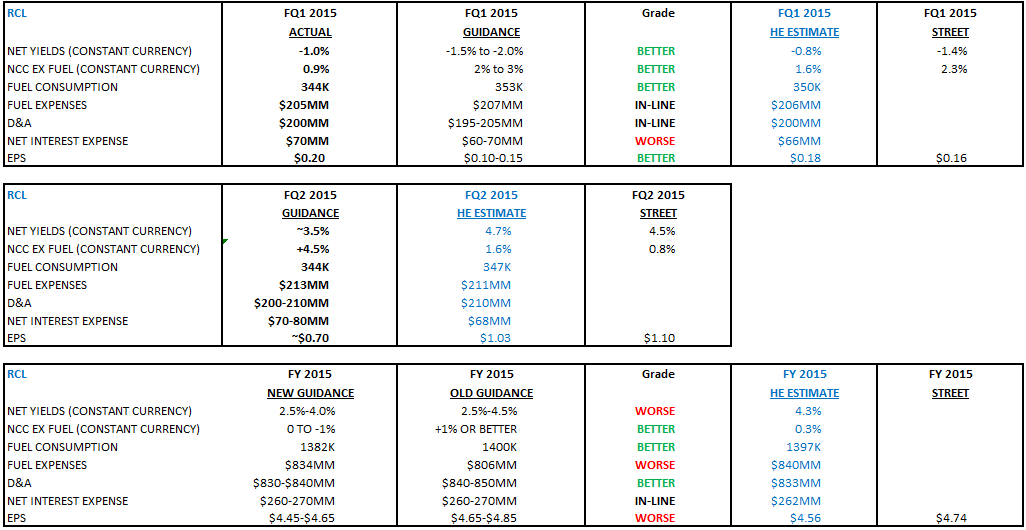

- Relative to guidance in October 2014, currency impact -$0.59, +$0.54 fuel impact. Relative to guidance in Jan 2015, -$0.36 (-$0.15 (fuel), -$0.20 (FX).

- Committed to keeping costs down this year and next year

- 2-4 itineraries is only a small portion of their NA itineraries

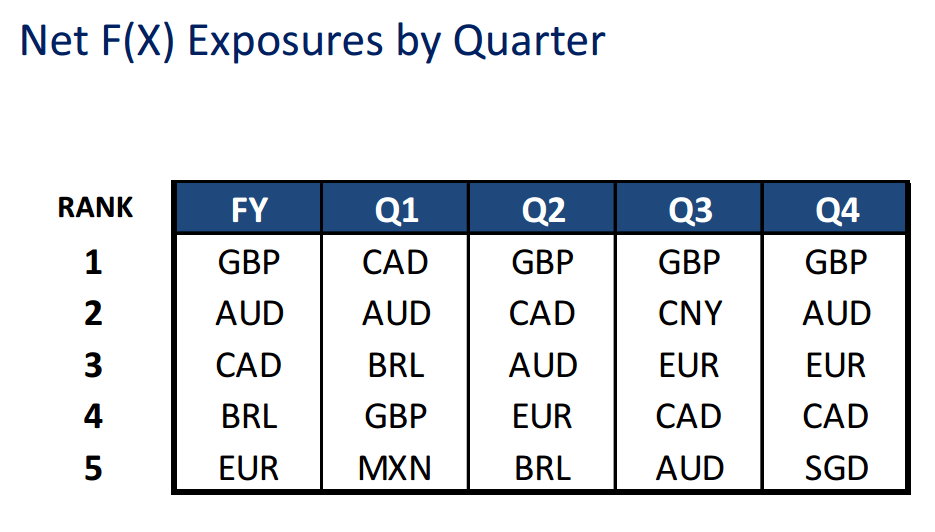

- FX impact onboard spend depends on exposure (see chart above)