Editor's Note: This is a brief excerpt and chart from today's Morning Newsletter. Click here for more information on how you can subscribe.

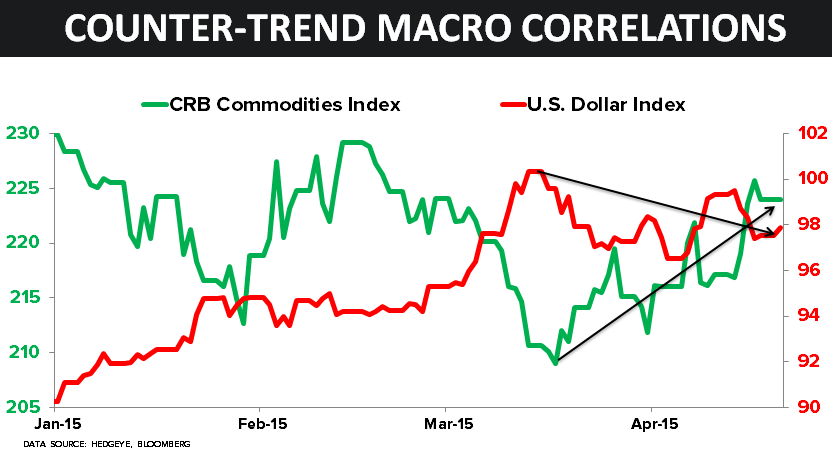

If you look at the Correlation Risk (USD vs. everything Commodities) on a 1-month basis, it’s been significant, even though the USD hasn’t corrected much on a percentage basis. Here are the 1-month moves: