Sales trends look better that most in 3Q09, but 4Q09 guidance is troubling.

There is no reason for me to patronize Doug Benn, but since landing at CAKE the company seems to be in much better shape. It’s clear he brings a financial discipline to this company that it has lacked in the past. Understanding that the significantly slower unit growth helps too!

Knowing that historical valuations are meaningless, it’s really hard to determine what the right multiple for any given name is. As a group, the Full Service restaurants are trading at 6.1x NTM EV/EBITDA, with CAKE trading at 7.6x. So it looks expensive on a relative basis. The FCF yield is 10%, but it looks like capital spending is going higher in 2010.

Sales trends are under control and the proper financial disciplines are in place to assure some stability to the earnings trends. The Cheesecake Factory is a strong concept, but the Grand Lux is an orphan.

I don’t see a great short story, nor do I see a reason to be super long. If CAKE can do $1.05 next year, it’s trading at 19x EPS. Given some of the risks that are still facing the company and the industry, any multiple expansion from here is unlikely. The strong balance sheet and free cash flow is net positive.

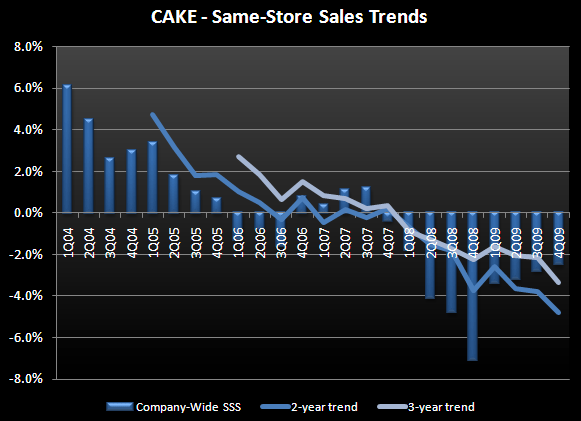

3Q Same-store sales trends – CAKE posted sequential improvement in same-store sales; sales decreased 2.4% and 6.0% at The Cheesecake Factory and Grand Lux Café, respectively. This represents no improvement on the 2-year trends at The Cheesecake Factory and a deceleration of 0.6% at Grand Lux.

At The Cheesecake Factory, the trends were slightly more negative in the west, particularly in California and the northwest. In the southwest, including Arizona and Nevada, CAKE is seeing stabilization on a sequential basis. Surprisingly, Florida and the southeast were actually both slightly positive for the quarter.

The sequential decline in sales trends at Grand Lux is troubling. Management is working to address the issues. I’m not confident there is much momentum behind that brand and would expect management to close some stores in the coming quarters.

Operating Expenses – In 3Q09 Cost of Sales decreased to 23.9% vs. 25.7% last year. The 180bps improvement was driven primarily by lower restaurant costs of sale. About 50% of the decline was due to the cost of sales initiative and 50% from lower commodity prices. Labor costs were 32.9% vs. 33.2% last year. Other operating costs and expenses were 25.5% vs. 25.6% last year. Utilities costs decline by 50bps offsetting higher marketing expenses. G&A expenses for 3Q09 were 6%, up 70bps from last year. The majority of this increase came from performance bonus accruals.

Development - CAKE is looking at 2010 and may open as many as three new Cheesecake Factory restaurants.

Strong Financial Position – At the end of the 3Q09, CAKE had a cash balance of $82 million and used $50 million to pay down debt during the quarter. CAKE’s credit balance now stands at $125 million, as they have repaid $150 million so far this year. The stated goal was to reduce debt by $125 million this year. CFFO for the nine months was $146 million ($24 million capital expenditures); generating $122 million in free cash flow.

Outlook – EPS guidance is for 4Q09 EPS of between $0.18 and $0.20, based on same-store sales of between negative 2% to 3%. Impacting the sales trends in 4Q09 by 1% are (1) Halloween falling on a Saturday and Christmas will fall on a Friday, both of which will hurt year-over-year comparisons. (2) A new focus on gift card sales this holiday season. The impact is expected to slow 4Q09 sales, but will build future traffic trends.

As you can see from the chart below, management’s current guidance for 4Q09 SSS would signify a significant slowdown in sales trends from where we ended 3Q09.

If these numbers are right, CAKE will have issues, but right now I don’t want to bet against Doug Benn being conservative.