Earlier today Hedgeye’s European analyst Matthew Hedrick led a discussion on why we are still bullish on the German equity market.

Watch the for a video replay below.

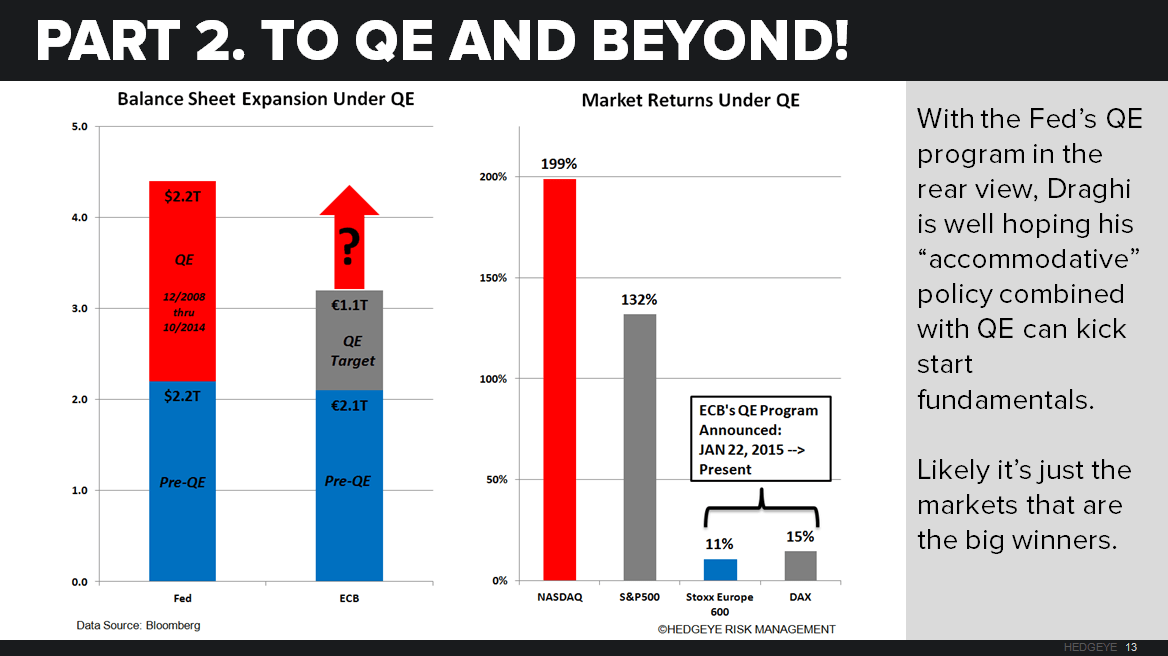

Key take-ways from the call include:

- QE is only just beginning; the euro will continue to weaken; Germany will disproportionately benefit due to exports; and asset classes like equities will inflate due to money creation

- The German economy sits in the sweet spot to benefit from a weaker euro as its exports account for a monster 47% of German GDP

- Since the ECB announced QE on 1/22/15 the correlation between the DAX and EUR/USD is -0.84, a strong negative correlation that we expect to persist as the ECB keeps its foot on the QE pedal for longer than its intended target (late 2016)

- Recommending long the DAX (HEWG or EWG) and short EUR/USD (FXE)