Below are key European banking risk monitors, which are included as part of Josh Steiner and the Financial team's "Monday Morning Risk Monitor". If you'd like to receive the work of the Financials team or request a trial please email

------

Key Takeaway:

While it fulfilled a promise to meet a payment deadline on its IMF loan, Greek spreads widened. This may be an indication that, in the debate of whether Greece is unwilling or unable to repay, investors are leaning towards the latter.

European Financial CDS - Swaps mostly tightened among European banks last week. However, Greek bank swaps widened between 24 and 77 bps, even as Greece met a deadline for repayment of part of its IMF loan and Greek finance minister Yanis Varoufakis promised that the country would meet "all obligations to all creditors". There has been debate recently about the possibility that Greece can make repayments but is unwilling. Now that Greece has shown its willingness to make payments, continued spread widening could be an indication that investors are leaning towards the belief that the country is unable.

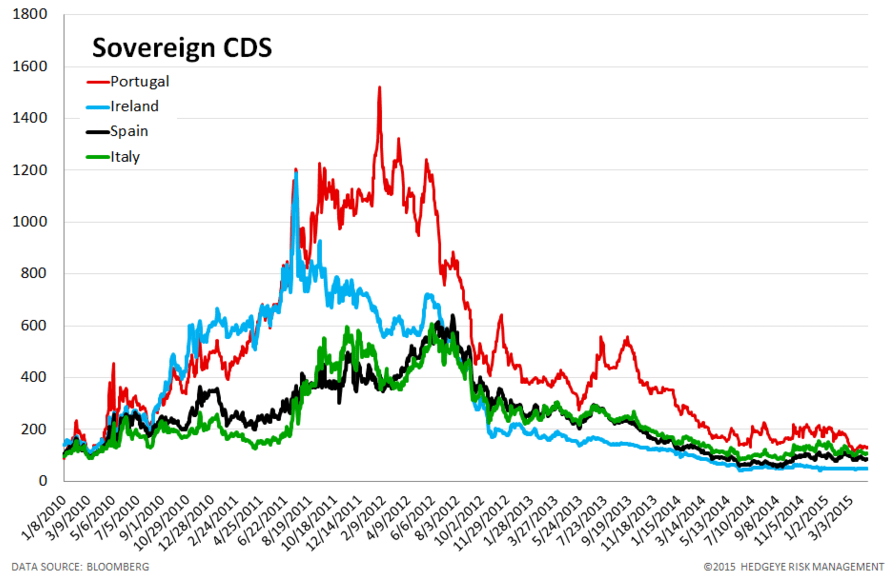

Sovereign CDS – Sovereign swaps modestly tightened over last week. Portugal tightened the most, by -3 bps to 132. Of those that widened, German sovereign swaps widened by 1 bp to 17.

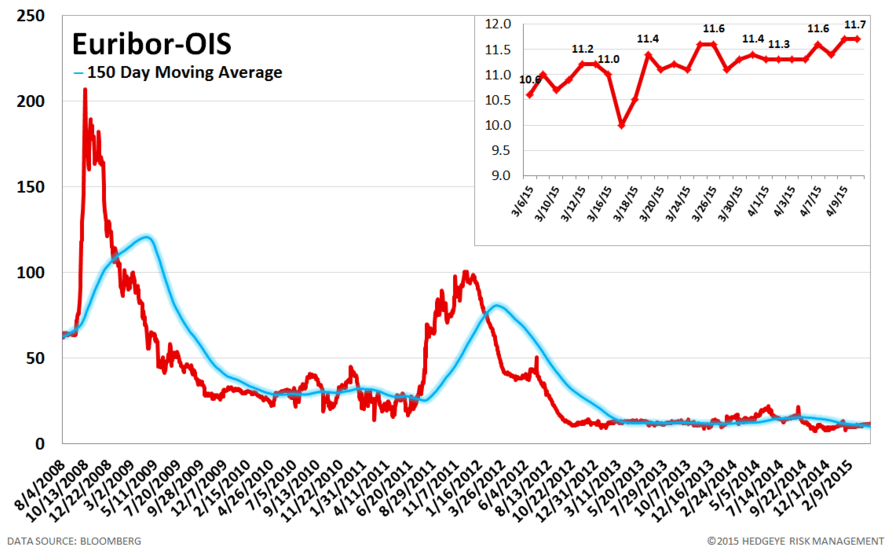

Euribor-OIS Spread – The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk. The Euribor-OIS spread was unchanged at 12 bps.

Matthew Hedrick

Associate

Ben Ryan

Analyst