I spent all day yesterday in New York City with my team meeting and debating some of the smartest institutional investors in the world.

The debate (in most meetings) was as vibrant as it has been in a long time. You can read all about it in my Morning Newsletter. Lots of learning equals less mistakes.

Some quick thoughts:

Right now, there are a lot of people looking for the US Dollar to decline and Oil to rise. It’s just not happening as the USD is +2.6% week over week to 99.29 on the USD Index and WTI is re-testing a breakdown through $50.

Meanwhile, Euros continue to burn, $1.06 last – we’re staying with our #StrongDollarDeflation theme.

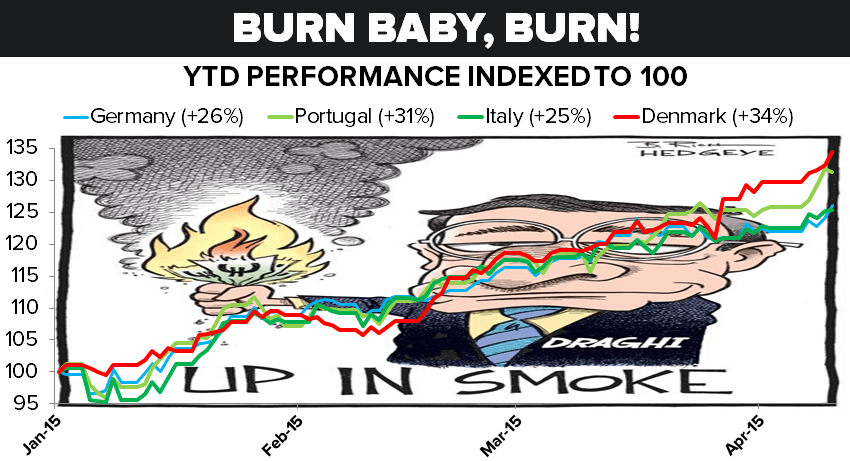

On a related note…my, oh my, are these stock markets in Europe incredible to watch!

In Germany, the DAX is +1.7% this morning to fresh year to date highs of over +26%. Places like Denmark are up over +35% year to date. They love the smell of Burning Euros. How could you blame them?

European profit margins are going up on this epic FX move like US ones did when the USD was devalued.

Click image to enlarge.