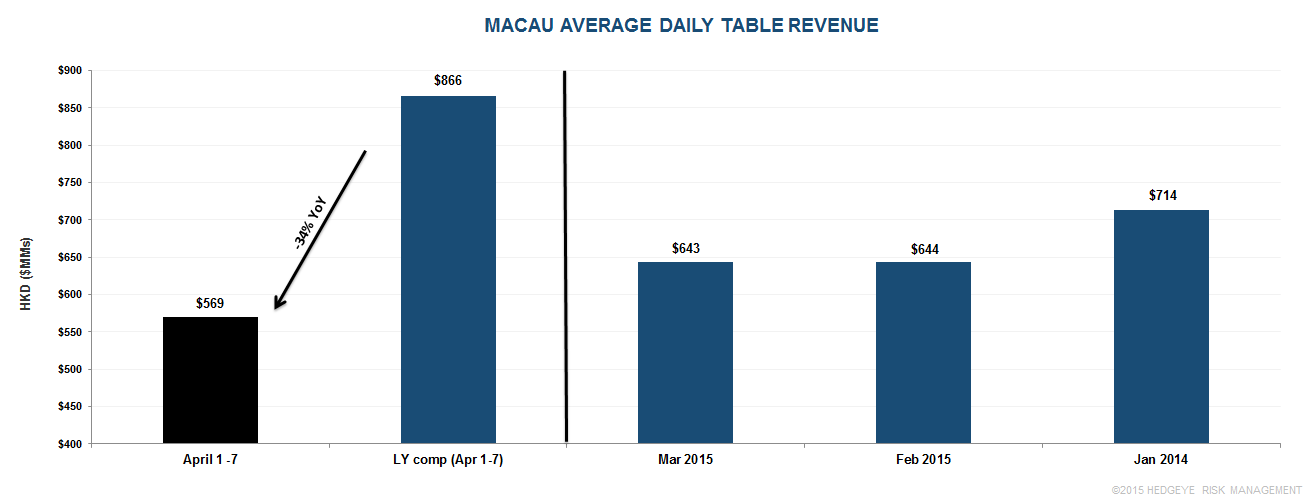

Daily table revenues for the 1st week of April came in only at HK$569m, down 34% YoY. This is worse than the low HK$600s we had been seeing in March. The Chingming festival (April 5) may have played a role in the lower numbers.

Last year, revenues fell 21% in the Chingming festival week versus the previous week. For 2013, the difference between the weeks was 2%. So there could be some impact but it varies.

However, if the current run rate persists, we could be seeing a monthly decline closer to -40% for April, which would be another disappointment.

We will have more details in our Macau monthly presentation/conference call this Friday at 11am.