Editor's Note: Below is a brief excerpt from today's Morning Newsletter written by Hedgeye CEO Keith McCullough. Click here to become a subscriber today.

Then I got lucky as the lead supply story on Oil for the last 3-6 months (rising Oil production) hit the tape:

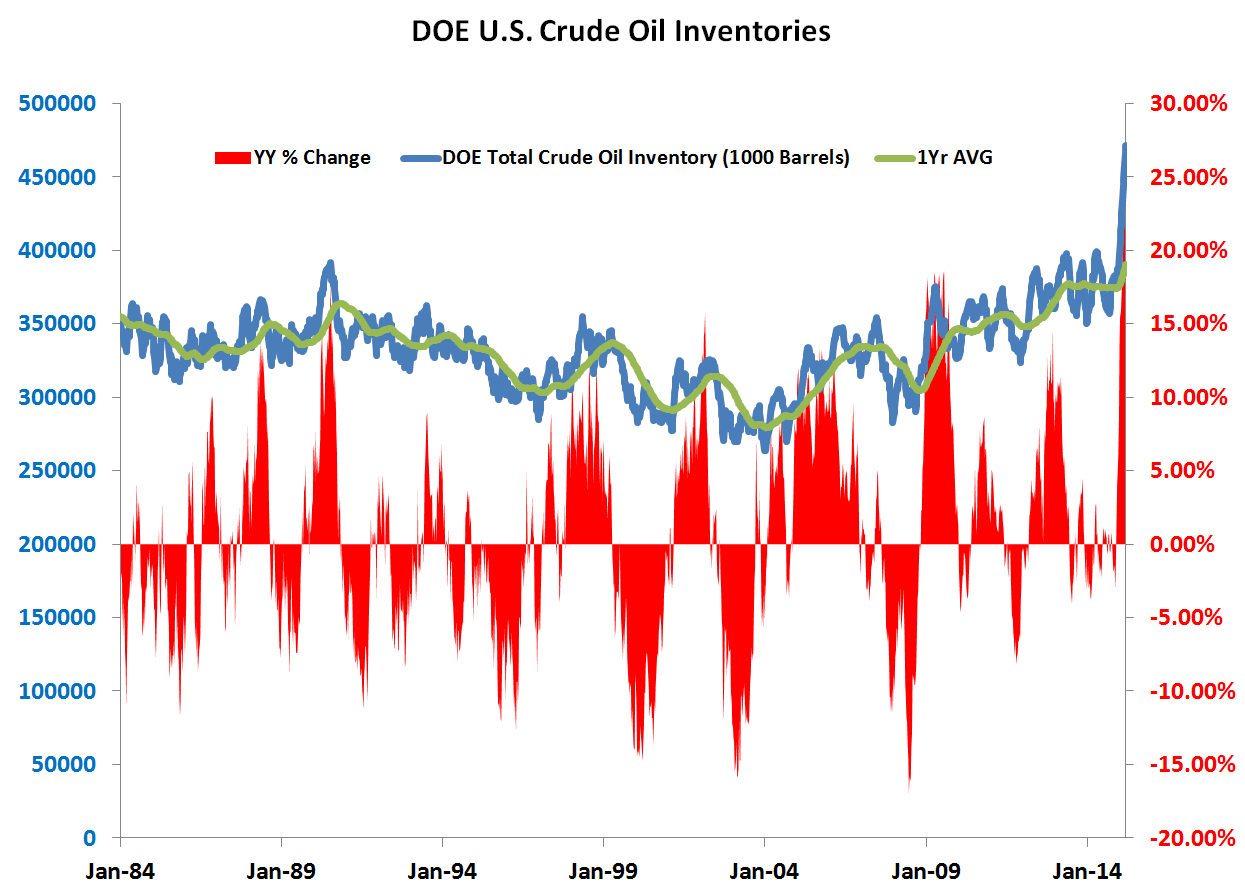

- The API reported domestic crude inventories increase another 12.2MM barrels week-over-week

- That was basically the biggest sequential increase we’ve seen through this whole downturn

- A DOE number in that area code (10:30AM EST today) would be the biggest sequential ramp since DEC 5th, 2014