CALL TO ACTION

The Macau stocks appear to be in a trading range with March coming in essentially in line with expectations. While we definitely picked up on some potential bright spots while in Macau, 2015 EBITDA estimates look high to us, particularly LVS which maintains more exposure to the grind Mass segment. While exposure there should prove beneficial over the long-term, we fear the Street is overestimating growth in that segment this year. Disappointing results in the highest margin segment will impact profits disproportionately. We believe this is the major driver of the disparity between the Street and us, despite similar GGR forecasts (-25%).

We will be hosting a call on Friday morning at 11am to discuss our Macau outlook and to provide an in-depth look into the Direct VIP segment.

MACAU MARKET OBSERVATIONS

- GGR fell 39% and 41% on a hold adjusted basis – the casinos played a little lucky

- Unadjusted Mass and VIP revenue fell 29% and 45%, respectively

- Adjusted for the reclassification of certain tables from Mass to Direct VIP to circumvent the Mass smoking ban, VIP and Mass revenue fell 48-50% and 16-20%, respectively

- Junket volume dropped 54% - the 2nd worst decline behind February’s 60% drop

- We estimate Direct VIP accounted for 8.5% of VIP volume in March compared to 8.3% over the past 3 months and 7.0% in March 2014

- Slot revenue tumbled 25% YoY

COMPANY TAKEAWAYS

Sands China (LVS)

- GGR share at 21.4%, in line with its 3 month average but 100bps below the 12 month average. The discontinuance of phone proxy betting in October has caused the share decline. As of now, the Sands China properties are the only ones that will not accept phone proxy betting.

- Eliminating phone proxy betting likely contributed to the market leading 62% decline in junket volume.

- On a YoY basis, GGR fell 41%, the 3rd worst in the market

- We estimate adjusted Mass revenues declined 22-24%, the 2nd worse decline ever behind February’s -26-28%

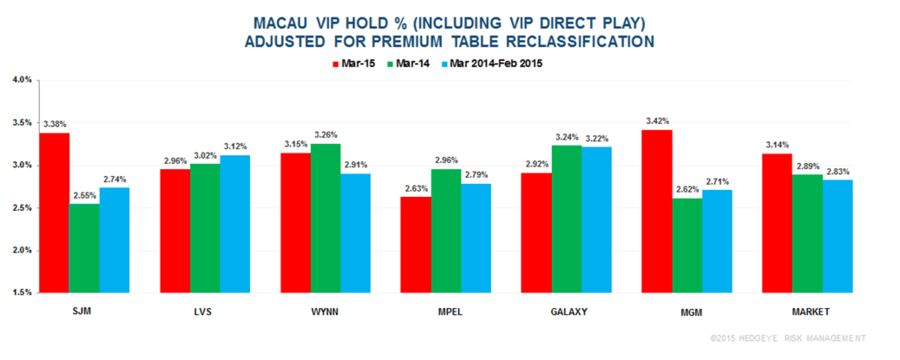

- Adjusted for mass reclass, hold was normal in March

- We remain concerned with Street estimates given the worse than expected performance in the grind Mass segment and slots (down 32% YoY in March)

Wynn Macau

- The new junkets at Wynn Macau appear to favorably impacting market share – Wynn’s GGR market share grew 150bps versus its 3 month average driven by a 220bp increase in Junket volume share

- Wynn also resumed its phone proxy betting operation which also contributed to the Junket and GGR share improvement

- However, on a YoY basis, Wynn is fighting an uphill battle. GGR fell 43% from March 2014, the worst in the market, despite higher hold compared to normal and last year.

- The precipitous drop in VIP has certainly freed up some hotel rooms for Mass customers. Wynn’s Mass business was the best performing in the market with only a 5% decline

- Wynn Macau should continue to be a market share gainer in the coming months

MGM China

- GGR fell “only” 34%, the 2nd best performance in the market driven by very high VIP hold (3.4%)

- During the month, MGM converted its reclassed Direct VIP tables back to Mass so going forward the comparisons will be apples to apples for Mass and VIP

- Market share was solid, 40bps and 60bps higher than its 3 and 12 month averages.

- Junket volume dropped 57%, slightly worse than the market

MPEL

- For the 2nd straight month, MPEL’s GGR fell the least in the market, despite the lowest hold in the market

- Adjusted VIP hold was only 2.6%, so volumes appear to be “relatively” healthy

- Junket volumes led the market on a YoY change basis

- While market share came in below recent trend, hold was the likely culprit. Junket volume share actually improved markedly in March

Galaxy

- GGR declined in line with the market but market share was well below trend

- Lower VIP hold percentage was the likely culprit for the lost share as Junket volume share actually increased sequentially

- Junket volume declined 44% YoY, better than the market. However, in previous months, Galaxy had been significantly outperforming in VIP.

Here are the relevant market shares:

HOLD PERCENTAGES:

Please note that these hold percentages are estimated for 2 reasons. First, total VIP revenues included direct VIP while Rolling Chip volume only includes junket volume. Thus, direct VIP volume needs to be estimated. Second, the revenues reclassified from premium mass to direct VIP need to be estimated and subtracted out of reported VIP revenues.

2015 PROJECTIONS

Our 2015 GGR forecast of -24% YoY change remains unchanged.

CONCLUSION

While a little less negative than we’ve been in a long time, this coming earnings season could shine a light on the deterioration of the high margin grind Mass segment. The Street still appears to be projecting decent growth in this segment in 2015, despite recent monthly declines. The weekly and monthly data do not break out grind Mass and premium Mass but table minimum bet levels and anecdotal evidence suggests a negative trend. Looking ahead, we’re encouraged by some recent trends in Direct VIP and some stability in the grind Mass segment, albeit at levels likely lower than Street expectations.