KEY POINTS

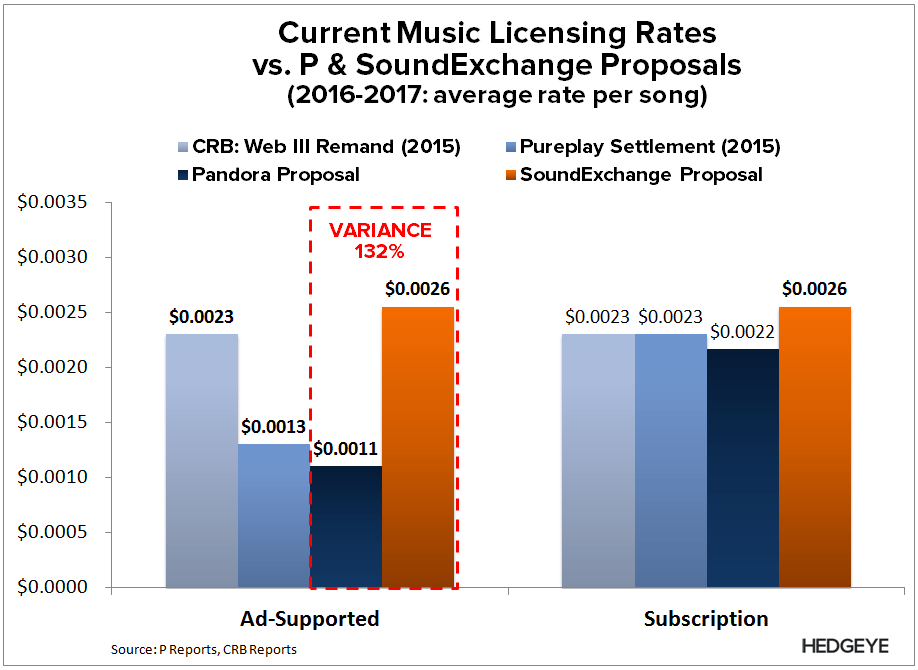

- THE CRITICAL DEBATE: the royalty structure. The key difference between the P and SoundExchange (SX) rate proposals is that SX is not distinguishing between ad-supported and subscription royalty rates. It’s that potential step-up in ad-supported rates that could cripple P’s model. So the question is whether the CRB believes there should be a distinction between the two.

- P MAY BE LOSING THIS DEBATE: We believe there are three main considerations regarding the varying royalty rate structure. In short, we suspect P doesn’t have much of a leg to stand on in this specific debate because the premise/support behind its arguments have limited legal bearing on the Web IV proceeding.

- WEB IV=POWDER KEG: What we mean is that the viability of P's model is highly sensitive to very small variations in final Web IV rates. To expound further: If P cannot convince the CRB to distinguish royalty rates by revenue source, then P would likely have to blow up its own business model. See the below scenario analysis and links to prior notes for supporting detail.

THE CRITICAL DEBATE

Both P and SX have provided a series of dense divergent arguments to the CRB; each discussing seemingly entirely different topics, which makes hard to tell who is really “winning the argument”. With all the noise in the CRB filings, we believe the street is losing sight of the key debate, which is the royalty structure.

The key difference between P’s and SX’s rate proposals comes down to the distinction between royalty rates for ad-supported vs. subscription tracks; SX is not distinguishing between the two in its proposal. It would be that step-up in ad-supported rates that could crush P’s business model. So the question is whether the CRB believes there should be a distinction between the two.

P MAY BE LOSING this debate

We believe there are three main considerations regarding the varying royalty rate structure. In short, we suspect P doesn’t have much of a leg to stand on in this specific debate because the premise/support behind its arguments have limited legal bearing on the Web IV proceeding.

- Pureplay Settlement is Irrelevant: It’s important to note that the distinction between royalty rates by revenue source (ad-supported vs. subscription) was not the result of any CRB decision through any Webcaster proceeding. It came from the Pureplay settlement agreement; the terms of which prohibited the associated rates from ever being included as a benchmark in any rate-setting procedure. P’s current proposal is structured under the same framework as the Pureplay agreement, and potentially existing agreements in the market (see below).

- Existing Benchmarks May Not be Relevant: The center of the debate on royalty rates is what willing buyers/sellers would agree to in a competitive market outside the shadow of statutory rates. Both parties are using different benchmarks as precedent to argue their cases: P is using existing webcasting agreements, while SX is using existing on-demand/interactive agreements. P’s benchmark appears more logical, but those agreement only cover a small subset of the market (28 of 29 agreements with independent labels). Further, it would be tough to argue that these rates were determined outside of the shadow of statutory rates (or worse the Pureplay agreement), especially since SX provided witness testimony from involved parties suggesting otherwise.

- P’s Financial Positioning is Irrelevant: P has taken the position that it can’t afford a rate increase, let alone current rates. Sx has taken the position that P’s wounds are self-inflicted because it has focused on gaining market share vs. profitability. But Sx concludes with a more important point. P’s financial positioning has no bearing on what the appropriate rate should be, quoting the CRB judges in the Web III Remand final ruling. “The Act instructs the Judges to use the willing buyer/willing seller construct, assuming no statutory license. The Judges are not to identify the buyers' reasonable other (non- royalty) costs and decide upon a level of return (normal profit) sufficient to attract capital to the buyers.” In short, P's monetization strategy (advertising vs. subscription) has no bearing the statutory royalty rate.

WEB IV=POWDER KEG

What we mean is that the viability of P's model is highly sensitive to very small variations in final Web IV rates. To expound further: If P cannot convince the CRB to distinguish royalty rates by revenue source, P would likely have to blow up its own business model.

We had previously run a series of scenario analyses projecting P's EBITDA under various potential Web IV outcomes (see first link below). Below is an additional scenario: P's proposed subscription rates applied to ALL of its listener hours. For context, P has only $355 million in cash.

We're highlighting this scenario because this might be P's best case scenario for Web IV if the CRB judges do not distinguish between ad-supported and subscription rates. That is unless the webcasters can convince the CRB that statutory royalty rates should be reset below those rates established in Web III, which seems like a stretch.

For more detail on the impact of Web IV on P's business model, see the two notes below. Let us know if you have any questions, or would like to discuss in more detail.

P: Worst-Case Scenario? (Web IV)

03/23/15 09:30 AM EDT

P: Webcaster IV = Powder Keg

01/13/15 02:49 PM EST

Hesham Shaaban, CFA

@HedgeyeInternet