Conclusion: We remain extremely confident in the long term KATE story, which includes the company doubling its sales base in 3-years, taking margins from 11% to 19%, generating $3+ in EPS power, and ultimately, a stock between $70-$80. Too often we have to couch a solid long-term story with challenges over the near term. But in this instance, we're seeing everything we need to remain comfortable that the company is executing on the short term plan as well as the long term. We think that the margin equation looks very good for KATE this year (and this quarter), especially relative to expectations. But let's face it, at 20x EBITDA, we need unadulterated top line growth IN ADDITION to improved margins for the stock to work. The good news is that we think we'll get both. While we won't see the company comp 28% like we saw in 4Q (when it put up the best comp in all of retail), we'll be shocked if the company does not beat the consensus of 7% (the whisper last month -- when the stock was still in the low $30s -- was 4-5%). We're at a 10% comp for the quarter, and if we had to pick the over/under on our estimate, we'd say 'over'. While e-commerce is not the be-all-end-all for KATE, it is important at 20% of sales. The US traffic trends looked particularly good as the quarter came to a close. We outline more details below. For more details on the quarterly puts and takes, see our 3/5 note entitled "KATE - Buy The Guidance Gauntlet".

Details

The way the math works, e-commerce alone would support 5% comp growth assuming it is a) 25% of the business in 1Q, b) grows at 20%, and c) Brick and Mortar comps are flat. If we ratchet e-comm comps up to 25% holding all other assumptions the same, it would get us to a 6.25% comp for the quarter. Based on what we’ve seen from the traffic metrics throughout 1Q we feel extremely confident in the company’s ability to deliver on the top line. We’re at a 10% comp for the quarter.

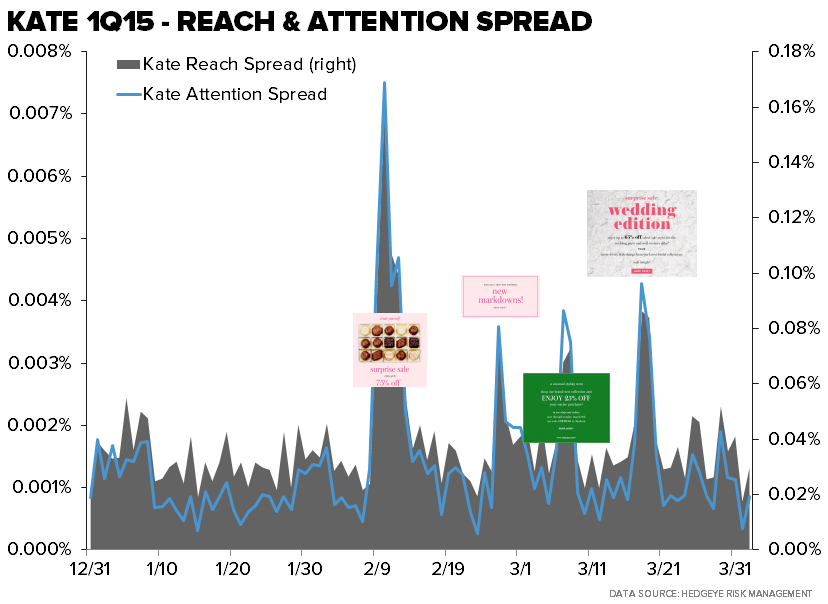

Here are a few charts we pulled looking specifically at KATE’s e-comm traffic trends in the US. These are daily metrics that gauge the visitation (measured by reach) and engagement (measured by attention) on a given day relative to the internet in aggregate. We then paired that with the ‘Flash Sale’/promotional events during the quarter to get a better sense of what drove outsized traffic during the quarter.

1Q15

Traffic trends (see chart 1) looked rock solid during the quarter. Measured by the YY spread in reach and attention.

We think that’s a favorable set up for KATE on the top line. Especially when you consider that the meaningful top line outperformance in 4Q14, where the company guided to 8%-14% comps and posted a 28%, was due in part to outperformance on the company’s reduced ‘Flash Sales’.

To sum up our thinking on the subject…fewer events does not equal less demand. In fact, it’s just the opposite, where reduced sales lead to increased demand at both a) Full Price and b) the reduced number of Flash Sales.

Chart 1 – 1Q15 Daily Reach and Attention spread for katespade.com

In total there were 4 events that accounted for big spikes in traffic in both 1Q15 and 1Q14. The makeup of those sales differed in each quarter. 1Q15: 2 ‘Flash Sales’, 25% off new collection (which occurred last year), and a more generic ‘New Markdowns’ sale. 1Q14: 3 ‘Flash Sales’ and 1 ‘Friends and Family’ event (chart 2 below).

Last year the company pulled one sale forward, the ‘Friends and Family’ event, from April to March as an attempt to capture sales that would have otherwise been pushed into 2Q because of a late-April Easter. The fact that the company didn’t see the need to repeat this sale in 1Q of this year, gives us a lot of confidence that the company is cranking on its internal plan.

It’s also important to point out that these ‘Flash Sales’ are not Gross Margin dilutive because much of the product is designed specifically for this channel. Meaning margins should be in good shape as the company works to improve quality of sale.

Chart 2 – 1Q14 Daily Reach and Attention for katespade.com

***chart note: these are absolute values and do not reflect the YY spread.

Market Share

Lastly, a point on market share. KATE still doesn’t have much of it, just 3%-4% in the US. And the company is continuing to grow its footprint and customer base as it fills out its category and distribution platform. That’s probably best demonstrated by Chart 3. This shows the reach (% of total internet users) visiting katespade.com on each day over the referenced time period. The growth in its user base on a relative basis reflects the strength we've seen from the e-comm channel over the past 18mnths +. And for KATE, with over 20% of its sales already captured through the online channel it can’t be explained away by a shift in the way consumers shop.

Chart 3 –Daily Reach for katespade.com (August 2013 – July 2014, August 2014 – April 2nd 2015)