On Wednesday, the S&P 500 closed at 1,081, down 0.9%. The S&P declined for the second straight day on accelerating volume, although the market was in positive territory for most of the day. Yesterday’s move at the end of the day was on outside reversal, which is also a bearish sign.

On the MACRO front, the global RECOVERY theme provided the upside support ahead of the release of the Chinese economic data. Chinese GDP rose 8.9% in the 3Q; the median of 34 estimates in a Bloomberg News survey was for a 9% gain.

Yesterday, portfolio activity included buying GS and shorting MS. Keith also shorted TOL, AAPL and PENN. We also shorted more of the USO.

The dollar weakness continued yesterday as the UUP declined 0.6%. Yesterday the VIX surged 6.3%. With dollar weakness, Energy (XLE) outperformed the S&P 500. December crude finished up $2.25 at $81.37 a barrel, the highest settlement since October 9th 2008. The materials (XLB) did not benefit from the dollar weakness, as an earnings miss from Dow Chemical (DOW) weighed on the chemicals. Further weakness is expected in the XLB today as Potash (POT), which is one of the world’s largest fertilizer companies, missed numbers this morning.

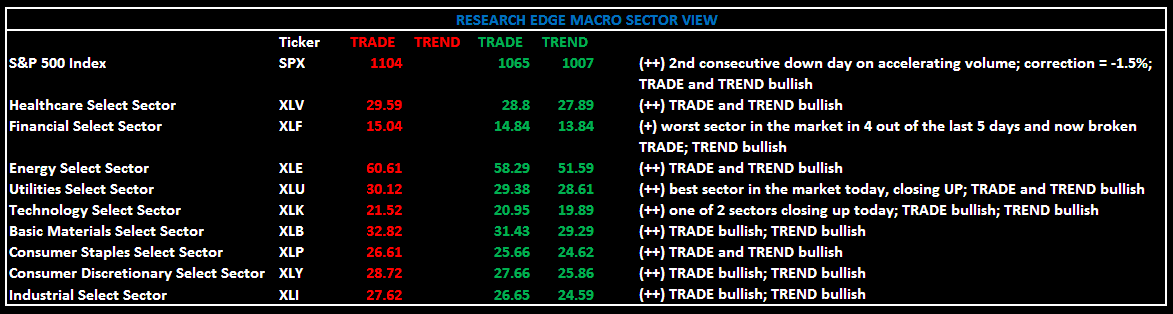

Yesterday, only two sectors were up on the day (XLU and XLK) and five sectors outperformed the S&P 500. The three best performing sectors were Utilities (XLU), Technology (XLK) and Energy (XLE), while Healthcare (XLV), Consumer Discretionary (XLY) and Financials (XLF) were the bottom three.

The Financials have been the worst performing sector in the market in 4 out of the last 5 days and is now broken on the TRADE duration. The regional banks have been dragging down performance of the XLF on real estate and credit concerns, which has been further emphasized by Fifth Third Bank this morning who reported weak earnings on the back higher than expected bad loans.

On the political front related to financials, Elizabeth Warren was on CBS’ Early Show this morning discussing compensation for “piggy” bankers. Warren, whom heads the Targeted Asset Relief Program's oversight committee, stated: "Guys, you have to understand that you can't party on like it's 2007. If you're going to take taxpayer dollars, then the game has to change. In that sense it's real." Indeed.

Today, the set up for the S&P 500 is: TRADE (1,065) and TREND is positive (1,007). The Research Edge quantitative models have 9 of 9 sectors in the S&P 500 positive on TREND and 8 of 9 sectors are positive from the TRADE duration. Yesterday, Financials broke trade.

The Research Edge Quant models have 0.5% upside and 1.5% downside in the S&P 500. At the time of writing the major market futures in the U.S. are lower.

The Research Edge MACRO team.