Below are Hedgeye analysts’ latest updates on our eight current high-conviction long investing ideas and CEO Keith McCullough’s updated levels for each.

We also feature two additional pieces of content at the bottom.

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

CARTOON OF THE WEEK

IDEAS UPDATES

GS

Goldman Sachs stock had a good week rising 1.8% against an S&P 500 that was flat in the holiday shortened week. This extends outperformance for the leading investment banking stock against the broader market with GS investors outflanking the S&P 500 by 5.9% over the past 12 months.

With the firm reporting first quarter earnings in two weeks on April 16th, the market will be speculating no more on the solid capital position of the firm and also an improved trading environment for an equity and fixed income franchise that has gained market share as European competitors retrench. Revenue estimates for Fixed Income, Currency and Commodity trading sit at $2.8 billion for the quarter but the result should be in the $3.0 billion+ range, which will get investors thinking about growth again for the company with the first year-over-year gain in bond trading since 2009.

ITB

March Mojo

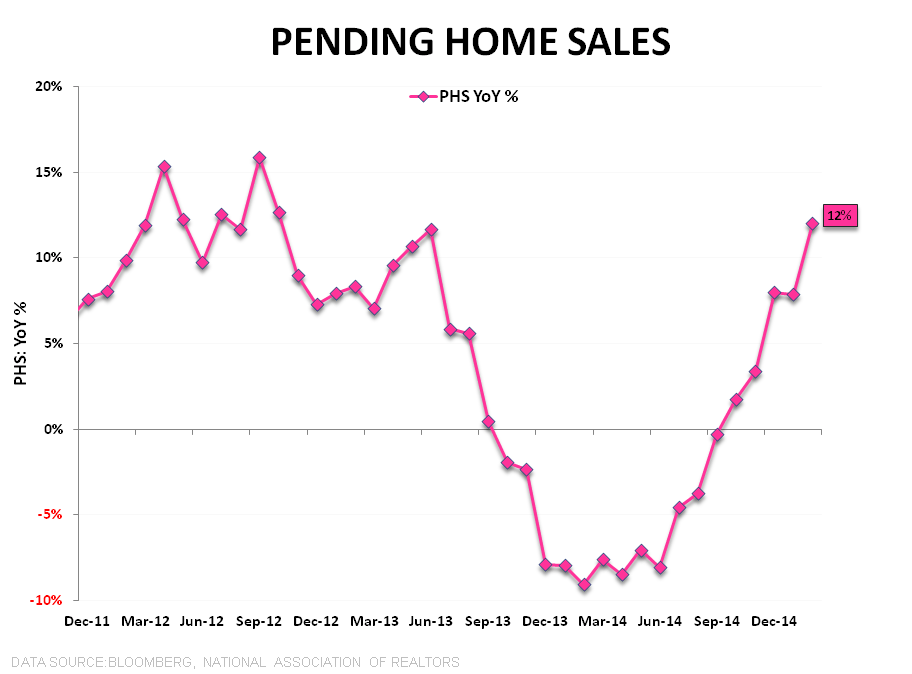

The housing data was again strong in the latest week with Pending Home Sales, HPI and Purchase Demand all accelerating to close out March.

- Pending Home Sales rose +3.1% sequentially in February with signed contract activity up a remarkable +12% YoY, taking the index to a new 19-month high. Pending Home Sales is a lead indicator for Existing Home Sales and the recent strength in Pending argues for upside risk in reported Existing sales (where the trend has been comparably softer) over the next couple months.

- Mortgage Purchase Applications – the most real-time, high frequency housing demand indicator - rose +5.7% WoW on the back of last week’s +4.9% advance and accelerated to +7.6% on a year-over-year basis. Given the notable acceleration in activity in the last two weeks of March, the data does indeed appear to be catching up to the thaw – a trend we expect to continue over the next 6-8 weeks

- HPI: The Case-Shiller 20-city series showed home prices grew +4.6% year-over-year in January, accelerating moderately relative to the 4.4% growth reported in December. A stabilization/inflection in home price growth is important as housing related equity performance tracks the slope of home price growth strongly.

- March Employment: The March Employment report released on Friday was broadly disappointing but belied ongoing, modest strength in housing demand fundamentals. First, 25-34 year old employment growth – the key demographic for 1st time buyer demand - held near the cycle high (& at a premium to the broader average) at 2.6% YoY. Second, residential construction employment rose +4K in March despite both adverse weather and softness in the balance of construction industry (total construction employment was down -1K for the month). On a year-over-year basis, employment growth continues to hold in the high single digits as conditions in the resi construction labor market continue to tighten.

We detailed our outlook for housing in 2Q with a deep dive conference call on Thursday entitled “If It Ain’t Broke…”. In short, we continue to like the setup for the sector over the current quarter.

TLT | MUB | UUP | EDV

It was another week of declining long-term yields getting you paid on the long-side of Long-term Treasury bonds (TLT, EDV) and anything that acts like it (MUB) as the benchmark 10-Year U.S. Treasury yield declined another -12 basis points. The USD experienced some volatility ending the week down (~-50bps) with the most pressure coming after Friday’s big Non-Farm Payrolls Report (#LaborMarket).

To reiterate our view over the longer-term, we pin a good chance the U.S. Dollar will reach new highs ($120 anyone?) with the probably of long-term Treasury yields reaching all-time lows very much in play.

#GlobalDeflation was one of our top 3 themes for Q1 and we’re continuing to ride that call:

With Q1 coming to a close on Tuesday, here’s how things shake out YTD:

- UUP +7.2%

- TLT: +3.8%

- EDV: +5.1%

- S&P 500: +0.40%

- MUB -0.1%

- XLE (Energy): -1.8%

- XLI (Industrials): -2.0%

- CRB Commodities Index: -6.0%

Deflation crushes the debtor who makes pays interest in U.S. dollars (over-leveraged energy companies) and the earnings power of industries leveraged to commodity Inflation. Unfortunately the pain may not be over (Steer clear)!

Both the Hedgeye macro team and your central planners in D.C. will continue to eye the labor market intently for direction on the U.S. dollar but remember that rates can go lower with the dollar going both ways (In 2014 rates reverted a whole 75bps even though the U.S. dollar declined -2% from January 1st to May 6th before going on a tear through the back half of 2015 into this year).

- Wednesday’s ADP report printed a number that slowed again sequentially in March which doesn’t bode well for the current rate hike expectation

- Friday’s Non-Farm Payrolls report for March was a certified disaster for those long of rates rising:

- Non-Farm Payroll additions added +126K vs. and expectation of +245K (+264K revised in February)

RH

Retail Sector Head Brian McGough and his partner Alec Richards remain big believers in Restoration Hardware (even with its recent run higher) and reiterate that RH is their best idea in retail. This recent deep dive note fleshes their thesis out in more granular detail.

MTW

While the crane business receives the most attention in part due to its cyclicality and because they are well, more noticeable, Manitowoc’s other business, Foodservice equipment, is the larger of the two in terms of operating income (60% vs. 40% for Cranes).

Several indicators are pointing towards upward momentum for MTW’s Foodservice business. Restaurant same store sales have benefitted since the drop in oil prices. Furthermore, an indicator by the National Restaurant Association, RPI Capital Expenditures Index, has surged recently in part due to lower fuel prices driving restaurant traffic and restaurant owners’ outlook.

* * * * * * * * * *

ADDITIONAL RESEARCH CONTENT BELOW

DALE: NO GROWTH?

Senior macro analyst Darius Dale says domestic economic growth remains fairly anemic with mounting risks to the downside as we progress through the balance of the year.

ual: will losing win, long-term?

"While a drop in jet fuel prices has led to a surge in airline shares," Industrials sector head Jay Van Sciver writes, "evidence continues to mount that UAL is not like the others."